A fleet of autonomous trucks linked into a single coordinated group safely complete a week-long transportation challenge held by the Dutch last month.

Self-driving cars are getting all the headlines. But judging by a convoy's recent test drive across Europe, self-driving trucks may transform our roads first.

A dozen or so trucks completed a week-long challenge in which they drove, for the most part autonomously, across Western Europe.

The Dutch government organized the challenge as part of its 2016 presidency of the European Union, which rotates among countries annually. The trucks, made by brands including Volvo, Daimler and Volkswagen subsidiary Scania, journeyed from their production bases in Sweden, Denmark, Belgium and Germany to their final destination in the port of Rotterdam in the Netherlands.

Self-driving trucks could lower shipping expenses by cutting labor costs and, with no weary drivers, letting trucks drive nonstop. It could also put a lot of people out of a job: in the US, one of the most common jobs is truck driving, according to census data.

The trucks might not be cute like the autonomous pod cars Google is testing, but they are very much a precursor to the self-driving personal vehicles that individuals will own. The findings from the truck experimentation will trickle down to affect how everyone uses roads in the future.

Using a technique called platooning, the trucks followed one another extremely closely as they drove at a constant speed. Linked by Wi-Fi, they could brake instantly, preventing road accidents caused by humans who don't react as fast even if they aren't distracted or sleepy. Platooning promises to improve traffic safety, reduce fuel consumption, and squeeze vehicles onto the road more densely for higher traffic flow.

"As the test shows, the technology has come a long way already," said Dutch Infrastructure and Environment Minister Schultz van Hagen. "What it also makes clear is that we Europeans need to better harmonise rules of the road and rules for drivers. This will open the door for upscaled, cross-border truck platooning."

Those behind the challenge hope EU member states will now grant permission for truck platooning to be used on national road networks. They hope countries will implement new technologies that improve safety and efficiency while driving, as well as enable the introduction of self-driving trucks into the existing market.

Income-tax officials have found new ammunition with which to extract correct information from taxpayers. The ammunition in question are social media posts, such as photographs of an overseas vacation or a new car, which the taxpayer has shared among his friends, little knowing that the same could be used by taxmen. Surprisingly , it is I-T officials in non-metros who are increasingly vetting social media posts of taxpayers.Prominent chartered accountants in Mumbai, Chennai and Delhi whom TOI spoke with haven't come across such instances.

The Central Board of Direct Taxes (CBDT), the apex body of the income tax department, has not issued any directive to its tax officers to scour social media. However, an I-T official admitted he finds it useful, in certain instances, to look up social media posts of a taxpayer to gather information.

"This isn't harassment as the posts are publicly available. We don't jump to conclusions, but ask questions, which results in correct tax assessment," said the official. Glimpses of how this was done in their client's cases were shared by several CAs. "The main purpose is to `spook' the taxpayer.So if the I-T officer says he will make an addition to the taxable income declared by the taxpayer in the I-T return, either by denying certain expenditure that was claimed, or by enhancing the income declared, the taxpayer (who is a businessman) may start cribbing on how his `dhanda' is not going well. Just as he is getting into the flow on how things could not have been worse, the I-T officer shows him pictures of his foreign trip a month back, which was shared by the taxpayer on Facebook," explains a chartered accountant (CA) based in Asansol, West Bengal.

"Tax officers want to see additions to income made during an assessment get converted into final collections and not get stuck in appeals.Producing photographs of an expensive vacation could prompt the taxpayer to blink and this helps close the assessment," adds the CA. Many entities, such as banks, companies with whom investments have been made, mutual funds, have to file annual information returns (AIRs). A taxpayer's significant expenses are revealed, to a large extent, via AIRs. To illustrate, a bank has to file details of credit card payments, of its customers, aggregating to over Rs 2 lakh in a year. Yet, social media data, which is collated by I-T officers, gives them the added edge.

"The main purpose of vetting social media posts is to ascertain the lifestyle and thus real income of the taxpayer. If his personal expenditure, including by way of foreign trips, is disproportionate to the income declared in the I-T return, an indepth probe can follow to unearth unaccounted income," explains a Hyderabad-based tax practitioner.

A smart readerasks how investing isn’t gambling. He/she says:

“While I agree with your premise that true investing is current spending for future cash flow, the only time this happens in the public markets is at an IPO. And even then, my money is still exposed to several risks of loss in ways that are similar to gambling. How do I know this company isn’t the next Enron? How do I know equities aren’t about to enter a 25+ year bear market (Japan)? How do I know whether or not Deutsche Bank isn’t about to sink the entire European banking system?”

Great question.¹ The answer, in my opinion, is largely a temporal problem and relates to what I call the Intermporal Conundrum in a portfolio – the problem of time relating to someone’s risk profile. A gambler wants to get rich quick so they do things that are irrational inside of a short time period. The investor lets time work for them by applying a strategy that has a high probability of success over time. The image below might better conceptualize my thinking here:

Most of us are behaviourally biased and short-term oriented. As a result we pay high fees for “market beating” return promises, we watch financial TV too much, we log-in to see our portfolios too much, we churn up short-term capital gains, etc. This leaves many asset allocators in the bottom left hand portion of our probability of success line and unable to move towards the upper right hand portion of the line. This results in worse performance because it leads to too much market timing, higher fees and higher taxes. And we know, definitively, that these frictions erode performance and must,by definition, underperform a pure passive portfolio.²

So, how does one overcome this temporal problem? Quantifying it is a good starting point. I highlighted a nice temporal measurement tool inmy new paper on portfolio construction.³ I also wrote about it a few weeks back in “How to Avoid the Problem of Short-termism“:

the allocation of savings is ultimately about asset and liability mismatch.¹ Cash lets us protect perfectly against permanent loss risk and maintain certainty over being able to meet our short-term spending liabilities, however, because it loses purchasing power it leaves us exposed to this risk in the long-term. Cash feels safe in the short-term, but in the long-term it is the riskiest asset because it is guaranteed to decline in value relative to inflation. We can extend the duration of our financial assets to better protect against the risk of purchasing power loss, however, this increases the odds of permanent loss risk (the risk of being forced to take a loss at an inopportune time) and not having the funds when you need them.

Thinking of your savings in terms of a specific duration can be extremely helpful for overcoming the problem of short-termism. For instance, we know that cash is essentially a zero duration asset that will lose purchasing power over the long-term so if you have no temporal flexibility allocating your savings then your duration is zero and you should remain in cash. On the other hand, if you wanted to reduce your risk of purchasing power loss you could buy a bond aggregate fund which pays about 2% every year and has a duration of about 5.5 years. You might not beat the rate of inflation, but you’ll do better than cash thanks to your temporal flexibility. Of course, you need to be able to put the funds away for 5.5 years to ensure high odds that you’ll get your principal back at that time.

The stock market is what makes all of this tricky since the stock market doesn’t have a specific duration like a bond does. In the paper I used a rough heuristic technique calculating the break-even point on a range of stock market declines in an attempt to calculate the stock market’s sensitivity to price changes. I arrived at a duration of 25 years which I think is both quantitatively satisfactory and intuitively correct since the global stock market tends to have a very low probability of multi-decade bear markets.

This puts things in a nice perspective for us because it allows us to allocate our assets in a way that properly contextualizes our asset and liability mismatch problem. For instance, we can now run a simple calculation using an aggregate bond index with duration of 5.5 years and the total stock market with duration of 25 years:

PD=(S*25) + (B*5.5)

Where PD = Portfolio Duration, S = % stock allocation & B = % bond allocation.

Here’s a basic cheat sheet for thinking about this across different time periods:

By quantifying the concept of time within our portfolios we’re able to become more comfortable with the way we allocate the assets. We’re able to increase the certainty in the way we balance that asset and liability mismatch. And importantly, what this exposes is a crucial reality – when we’re dealing with stocks and bonds we’re dealing with inherently medium-term and long-term instruments which means that this rat race of short-termism is completely inconsistent with the actual structure of these instruments. After all, you’d never judge the performance of a 2 year CD inside of a 1 month period, but that’s the equivalent of what someone is doing when they judge stock market performance based on a 1 year period.

By putting the concept of duration in the proper context you can improve the odds that you won’t fall victim to the problem of short-termism. And most importantly, by being armed with this knowledge going into the asset allocation process you’ll reduce the odds of falling victim to the many behavioural biases that plague modern asset allocators. As a result, you’ll reduce your fees, reduce your tax bill and increase your average performance. But most importantly, you’ll sleep better at night.

Good portfolio management is really about conquering the problem of time. It is the struggle to match an uncertain time horizon with financial assets that have uncertain life times. But by putting things in the proper context you can improve the odds of success. In doing so, you reflect the mentality of the investor and not the mentality of the gambler.

The unthinkable has happened with the United Kingdom voting to leave the European Union.

Arguably, this is potentially the most serious development in world politics since the collapse of the Soviet Union. (Curiously, both catastrophes happened ‘voluntarily’.)

What lies ahead? Let me outline three concentric circles – Britain’s future comes, of course, in the First Circle; followed by the fate of Europe in these uncertain times; and, enveloping the above two circles, the shift in the ‘co-relation of forces’ in the international system and world politics.

Unsurprisingly, David Cameron has done the honorable thing to do – draw a line on his public life as a statesman. He made a disastrous miscalculation by assuming that the conservative British people will never want to take a peep into the abyss. Well, they have, and he needs to quit. Three cheers for British democracy.

More important, however, the verdict itself is such a fractious and contentious one that it opens ancient wounds in Great Britain’s gory history. Scottish and Irish nationalism will inevitably rear their heads and militate against Britain’s departure from the European Union. So, how long can Britain survive in the present form? That is the troubling question.

Second, the British vote also strikes chords within other EU member countries – especially in Germany, Italy, Netherlands, Poland and so on. There is a pervasive weariness over the EU, accentuated by more or less the very same grievances that Brits have harbored – over migration, loss of sovereignty, security concerns, decline in welfare system and austerity, economic inequality, and so on.

So, what happens if the EU unravels? This is the second question.

If we go back in time and recall the impetus behind the European project as such, we are bound to come across ancient ghosts that the continent had desperately needed to bury but are still around – the great mutual revanchism between the peoples of France and Germany dating back to the 16th century, in particular. It is vital that the European project survives to ensure that those ghosts of history remain forever in the attic.

Even if EU doesn’t unravel, Britain’s role as a ‘balancer’ will be keenly missed. A new equilibrium will need to evolve. Which is not easy since Germany is already much more equal than the others in the tent.

So, will the German question, the most daunting spectre of modern European history, resurface? This is the third question.

In the international system, there is certainly going to be much volatility. Britain’s exit from EU deals a body blow to the US’ trans-Atlantic leadership. Indeed, there is no alternative but to mothball the Trans-Atlantic Partnership Agreement. It was meant to be a ‘platinum grade’ FTA, as John Kerry one put it. Washington may now have to settle for whatever is available, which may be no FTA. The advantage goes to China and Russia.

Beyond that comes the US’ geostrategy. Certainly, if Moscow is wringing its hands with pleasure today, there is good reason for it. A disheveled, disoriented Europe makes a weak negotiating partner for Russia. Combined with the strong ‘Russian lobby’ within Germany (and France, Italy and Greece, etc.), it becomes highly problematic for the US to keep the sanctions against Russia going.

So, will the US’ containment strategy against Russia be sustainable for long? This is the fourth question.

Then, there are the unavoidable fallout's – euro’s uncertain future, for instance, and the concomitant turmoil in exchange rates; or the decline of London (‘The City’) as the world’s financial capital; or the capacity of the US dollar to retain its status as the world currency; or the surge of yuan; or the investment flows in general, etc.

The post-cold war multi-polar order rests on four key pillars – US, China, EU and Russia. If one pillar becomes shaky, the architecture weakens. Serious repair and renovation work will need to be undertaken. But the big-power rivalry doesn’t easily allow that.

The good thing is that this momentous development has happened before Hillary Clinton and her neoconservative retinue moves into the White House in January. It comes as a badly-needed reality check for them on the serious limits to US power in world politics.

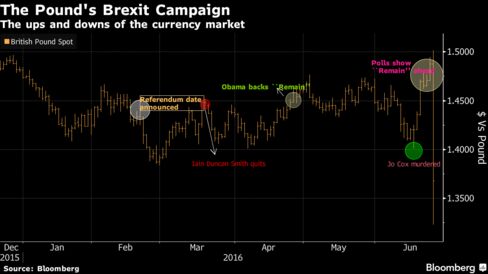

The experts were wrong again. Even on the day of the referendum, traders and oddsmakers, pollsters and professors were forecasting a vote to remain in the European Union.

In the wake of a stunning decision to leave the 28-nation bloc, the nation is left divided in a way not seen since the 1980s. What was a very British question over a lukewarm relationship with Europe turned into accusations of lying, evocations of Hitler and rather un-British slurs. The government -- whatever its complexion -- will now have to nurse those wounds.

The recriminations were stilled for a moment last week after the killing of lawmaker Jo Cox but the passions unleashed by months of bickering and assertions on the economy and immigration have yet to play out.

“Jo understood that rhetoric has consequences,” Stephen Kinnock, who shared an office with Cox in the U.K. Parliament at Westminster, told lawmakers on Monday after they were recalled for tributes. “When insecurity, fear and anger are used to light a fuse, then an explosion is inevitable.”

Who to Believe?

The battle at first didn’t quite grip the nation as much as it did financial markets, the pound gyrating with every twist and turn. Then it became a case of who to believe. Would Britain be better off forging its own trade agreements? What is sovereignty anyway? Is Turkey really about to join the EU? Do immigrants cost more to public services than they provide in labor?

“I hope we remember it as the high-water mark and the end of post-truth politics,” said Drew Scott, a professor of European Union studies at Edinburgh University. “The campaign has been riven with half-truths and falsehoods on both sides. We don’t seem to worry about the truth anymore -- it’s just about winning or losing.”

Cameron delivers a statement on Feb. 20.

It was a referendum that Cameron promised to call to keep his Conservatives together and see off the threat of Nigel Farage’s U.K. Independence Party at last year’s election. First, he had to hammer out a new agreement with the EU, including restricting welfare payments for migrants from the bloc.

Cameron summoned his cabinet for its first meeting on a Saturday since the 1982 Falklands war. On Feb. 20, they voted to back his deal and hold the referendum on June 23. It was never going to be enough for the Euroskeptics; cabinet ministers immediately started taking sides.

Enter Boris

Justice Secretary Michael Gove, one of Cameron’s closest friends and allies, appeared in a photo in front of a “Vote Leave” banner along with Iain Duncan Smith, the minister in charge of work and pensions.

Johnson speaks to reporters at his home, Feb. 21.

But the first real piece of choreography was in front of a crowd of reporters at the home of Boris Johnson, Cameron’s former Oxford University pal and biggest political threat. He declared “after a huge amount of heartache” he would go against the prime minister. The prize asset for the “Leave” campaign, bookmakers also put the now-former London Mayor as the front-runner to succeed Cameron. The pound had its worst day since 2010.

In response, Cameron launched a verbal assault on Johnson in the House of Commons, suggesting that he had based the decision on his ambition to replace him. Cameron, who had called for a civilized campaign, surprised lawmakers with the vehemence of his attack. Less than two weeks later Duncan Smith said Cameron’s “scaremongering” was damaging his integrity.

His campaign has “become characterized by spin, smears and threats,” Smith, a former Conservative leader, wrote in the anti-EU Daily Mail. He resigned from the cabinet on March 18 over the budget as Cameron returned from a regular EU summit in Brussels. The tone of the campaign was set.

Carney’s Eyes

From then on, every intervention was dismissed by one side or another as trying to spook the public, whether Chancellor of the Exchequer George Osborne’s warning of decades of economic pain, or the concerns of International Monetary Fund Managing Director Christine Lagarde and Bank of England Governor Mark Carney.

Mark Carney and Christine Lagarde

In the first of testy exchanges with politicians, pro-Brexit lawmaker Jacob Rees-Mogg told Carney in March “it is beneath the dignity of the BOE to be making speculative pro-EU statements.” Carney, often more statesman than banker in recent weeks, replied: “I’m not going to let that stand.”

U.S. President Barack Obama, on a trip to London to mark the Queen’s birthday, backed membership of the EU and said the country would be “at the back of the queue” for negotiating a trade deal with the U.S. In an article in the pro-Brexit Sun newspaper, Farage repeated a claim previously made by Johnson that Obama’s Kenyan background meant he was predisposed to dislike the British.

There were also alliances, some more unlikely than others. Old Labour Party leaders and chancellors shared platforms with Conservatives, pro-EU former Prime Minister John Major campaigning with his successor, Tony Blair.

Hitler Jibes

While the number of undecided voters could have always swung it one way or the other, opinion polls showed little sign of a revolution. In May, Sadiq Khan, an advocate of staying in the EU, defeated pro-Brexit candidate Zac Goldsmith to succeed Johnson as mayor.

Johnson left to tour Britain on Vote Leave’s battle bus, and Cameron looked more and more confident that things would go his way. Struggling on the economy, Vote Leaveput the focus back onto immigration, claiming that Turkey was close to joining the EU.

Johnson said the EU shared Adolf Hitler’s goal of unifying Europe, admittedly by different means. Other “Leave” campaigners mocked up German Chancellor Angela Merkel as Hitler. EU Commission President Jean-Claude Juncker said Johnson needed to be re-educated about Brussels.

“The only redeeming feature of Cameron is the other side are even worse,” former Scottish leader Alex Salmond, who fought and lost the 2014 independence referendum on whether to leave the U.K., said this week. “It’s been a poisonous, appalling campaign.”

‘Court Jester’

Major called it “squalid.” He likened Johnson to a “court jester,” albeit what turned out to be milder than Energy Secretary Amber Rudd’s comment days later that he “was not the man you want driving you home at the end of the evening.”

But the strategy was working. A YouGov Plc poll on June 1 showed the sides were now neck and neck, while the bookmakers increased the probability of Brexit to above 20 percent. The pound started weakening again.

In Brussels, the mood swung from frustration that the interests of one country were dominating the EU agenda, to confidence that the U.K. would never vote to leave. Then, in the two or three weeks before the vote, there was the sudden fear that the unthinkable might actually happen.

Top officials in the European Commission held daily meetings. Privately, some began to express the opinion that Cameron was not handling the campaign as well as they had hoped and that Farage and Johnson were being allowed to dictate the debate.

Merkel’s Moment

In a highly unusual intervention, Merkel took a pre-arranged question from a BBC reporter in English to warn the U.K. of isolation.

Angela Merkel

“For those coming from the outside, and we’ve had lots of negotiations with third-party countries, we would never make the same compromises, or achieve the same good results, for states that don’t take on the responsibility and costs of the single market,” she told reporters in Berlin.

The currency market reflected the anxiety increasingly being felt in the pro-EU camp. In the first week of June, the pound sank after a YouGov survey showed “Leave” at 45 percent and “Remain” at 41 percent.

Rattled, Cameron held an unscheduled press conference on a rooftop overlooking the river Thames. His alarm was clear the moment he started speaking, denouncing Johnson and Gove and accusing them of lying to the public.

“The Leave campaign are resorting to total untruths to con people into taking a leap in the dark,” Cameron said on June 7. “It’s not for me to say why they’ve made these factual errors and mistakes, but it is for me to call it out.” Later in the day, Cameron and Farage faced questions from a live television audience. Farage claimed the “Leave” campaign was being bullied: “We’re British, we’re better than that,” he said.

Tory on Tory

A week later, Conservative lawmaker Sarah Wollaston quit the "Leave" campaign over the claim it would free up 350 million pounds ($524 million) a week for the National Health Service. “They have knowingly placed a financial lie at the heart of their campaign,” she said.

Cameron realized he needed the Labour Party to detract from the Conservative in-fighting. Extracts of a speech by Osborne were held back so as not to clash with a one by former Labour Prime Minister Gordon Brown, whose intervention was key in the final run-up to the Scottish independence referendum.

Rather than throw the campaign into reverse, five opinion polls in 24 hours gave “Leave” the lead and Rupert Murdoch’s Sun newspaper backed the drive to leave the EU. “I’m sensing real momentum for “Leave” around the country,” Farage said on Twitter. “We can win this and get our country back!”

Final Days

Then everything changed.

A flotilla of fishing boats led by Farage sailed up the Thames to be met by rock musician Bob Geldof haranguing them through a sound system and playing themed music as small boats carrying “in” banners buzzed around. Fishermen started hosing the “Remain” boats.

’In’ and ’Leave’ boats on the Thames on June 15.

One contained Brendan Cox and his children the day before his wife and their mother was fatally shot and stabbed on a street near Leeds. The man charged with her murder later gave his name in court as “death to traitors, freedom for Britain.”

All sides suspended campaigning for the weekend. Farage talked of how the Leave campaign was running away with it: “We did have momentum until this terrible tragedy,” he said.

When the news of Cox’s murder broke during an EU finance ministers’ meeting in Luxembourg, shock was accompanied, for some, by the belief that it may help the “Remain” camp. In the run-up to the debate, several EU officials pondered whether a major event -- a terrorist atrocity or a huge influx of migrants -- would swing the outcome. Was this the defining moment?

The pound gained, ultimately touching $1.50 for the first time this year. Betting shops shorted the odds of a Brexit win. Endorsements came from household names for remaining in the bloc, from former soccer star David Beckham to TV presenter Jeremy Clarkson.

Little could still the furies.

On June 21, the day before his wife would have turned 42, Brendan Cox said in a BBC interview that Jo had become concerned about the “tone of the debate.” The worry was that it was “whipping up fear and whipping up hatred potentially,” he said. “The EU referendum has created a more heightened environment for it.

In the immediate term, an intense burst of volatility in financial markets on Thursday night and Friday morning is more or less assured, regardless of the outcome of the referendum vote. The outcome of the plebiscite is the dominant issue in the minds of traders and asset managers in the City of London and, increasingly, in other financial centres across the world. Various indexes of expected market volatility have been rising in recent weeks.

Who will be trading?

Some financial players, such as hedge funds, will be speculating on the outcome (or, more precisely, market movements in response to the outcome) with their own money. Other players, traders working for banks, will be anticipating a rush of orders from corporate customers for various assets in response to the outcome and they will be looking to position themselves to make a profit by making a market for these clients. There is expected to a be a frenzy of action in the spread-betting markets too on the value of currencies, as there usually is for high-profile political events with economic implications (such as general elections).

Is this just a UK phenomenon?

No. Movements in financial markets in recent weeks suggest that many now see the economic fallout from Brexit as of material importance not only for the UK economy, but for other states around the world too. Janet Yellen, the chair of the US Federal Reserve, today said Brexit could even have a negative impact on the mighty American economy. Stocks moved up throughout the world on Monday, a shift that was attributed by traders to perceptions of the risk of Brexit receding.

Which markets will be affected?

There is expected to be sharp movements in currency markets – particularly the pound versus the US dollar and the pound versus the euro. There is some expectation of major currency moves even before the polls close at 10pm because hedge funds and banks are rumoured to have commissioned private exit polls upon which they may trade. There will certainly be action throughout the night after polls close because traders will be responding as the results are announced by various districts throughout the country and the overall result comes into focus. There will be movement in “futures” markets for stocks and shares of UK-based companies overnight too. This will give some indication of the market reaction for equities. But heavy action for shares and bonds is expected from 8am on Friday when trading in the London Stock Exchange kicks off.

Which way will markets move?

Sterling strengthened considerably on Monday as traders discerned a strengthening of the Remain position in the poll. And many traders expect a Remain vote to push up the value of sterling further. Many expect a Leave to suppress the value of pound against other currencies, reflecting a bleaker output for the UK economy outside the single market. Some have estimated a fall in the value of sterling against the dollar of as much as 20 per cent. George Soros, the hedge fund boss who made a £1bn personal profit from betting against the pound on Black Wednesday 1992, when it fell 15 per cent, said this week that he expects an even bigger fall this time if Britain votes for Brexit. As far as stocks and shares are concerned, large international banks with exposure to Europe such as Barclays, Royal Bank of Scotland and HSBC could well be marked down in the event of a Brexit vote. Exporters to Europe could suffer too in anticipation of the return of tariffs. Tourism firms with big revenues from Europe such as the airline Easyjet and the cruise operator Carnvial could come under pressure. UK property and house building firms would also likely suffer if the domestic housing market comes under pressure. A converse boost to such shares is likely in the event of Remain. The outlook for UK Government bonds (Gilts) if Leave wins is more ambiguous. In a general market flight to safety Gilt prices have tended to rise in recent years since they are seen as safe assets, like Gold or US Treasury bonds. This would probably happen again. But Brexit could theoretically make them less attractive to investors if the view was that the UK had suddenly become a less desirable place to park money, sending their price down.

What will happen to interest rates?

The long-run interest rate is set by the yield on government debt, so that would depend on the attractiveness of Gilts after a Brexit vote. But the short-term rate is set by the Bank of England. Some economists say the Bank would be likely to cut rates further from their historic lows of 0.5 per cent in the event of a Brexit vote to support the economy and reassure investors, possibly also restarting the bond-buying QE programme. Others argue that if there is a major run on the pound, stoking expectations of a dangerous spike in domestic inflation, Threadneedle Street would need to raise rates to restore investor confidence, even though this would harm the economy and, in all likelihood, help tip Britain back into recession.

All the conservative traders should stay away for 2 days from trading Nifty being an event day. Partial risk takers can work out option strategies. Full risk takers can buy Nifty with a stop-loss of 8000.

Moving further into a challenging 2016, investors remain apprehensive about the global financial outlook and they are in the process of accepting the new state of markets, which is the low-returns in equities and fixed income. Extensive QE and negative interest rates inflate the markets and constitute the main reasons for the low-yielding scenery and for the rise of alternative investment allocations. Institutions like insurance companies and banks find themselves amid a difficult situation making alternative income-producing strategies appealing. Political issues add uncertainty to the ever-changing status of markets, such as the ongoing Greek debt and the upcoming Brexit referendum and concurrent U.S. elections. Even earnings in big corporations are lowering, signalling the need for rebalancing portfolios and shifting to alternative investments.

Alternative investments constitute a broad category, but this perspective focuses on three asset classes: hedge funds, private equity and private debt. Hedge funds constitute the most debated and controversial asset class gathering the lights of publicity for numerous reasons. With over $3.23tn of assets under management according to BarclayHedge and over 5 thousand institutional investors, hedge funds are considered to be the elite of money managers charging the infamous 2/20 structure to their investors. There is a lot of discussion since the beginning of 2016 regarding high fees and bad performance indicating the upcoming reshaping of the industry following the divesting of major pension funds. Despite, the exodus of big names in the institutional spectrum, more and more pensions are attracted to hedge funds according to Preqin research, which contrasts the recent assaults on the asset class.

Figure 1. U.S. Pension Fund investments in Hedge Funds, Source: Preqin Investor Profile

However, this pressure is likely to be sustained and resulted already in lowering of fees from some managers. But is it fair for some managers to take lower fees while they are delivering robust outperforming returns and while the costs for running a hedge fund are enormous? Recent regulatory changes and the need for alluring talent into the space gives rise to costs, which smaller managers have to charge their investors. The 'war on hedge funds' is based on the bad performance the asset class is exhibiting the last two years and this is merely explained by the overcrowding of managers. Hedge Fund Research database contains over 7,300 investment products, which manifests the over-competition in the space and attenuates the returns from α-focused strategies, making the pursuit of niche and unique strategies trivial. Hedge fund managers need to become creative and offer novel opportunities to the investors via exotic products and robust investment processes. Technology is the breakthrough the space is waiting for and new algorithmc and blockchain related strategies eye opportunities in a new unexplored investment arena.

Private equity, on the other side, is probably the biggest player in thε "allocation battlefield" with assets under management exceeding $4.2tn and with investor appetite for the well established asset class. Private equity constitutes the biggest enemy of hedges funds in attracting capital and identifying investment opportunities. Private equity seems to be more appealing to long-term investors due to the illiquidity offered, which allows to realise higher returns than their peers in the hedge fund space.

Investors appreciate the clawback provisions that PE managers offer them and prohibit managers from receiving fees when losses are experienced. The turbulent and volatile global markets add more uncertainty to the investments alongside the valuation challenges, which make the identification of the right investment opportunities hard and this will impact the long-term return of the funds. European PE is having another predicament to overcome, which is the AIFMD, a compliance burden that PE managers are not familiar with and makes them struggle. AIFMD will introduce depository and risk management processes to private equity funds. The next years are going to be challenging and constitute a period of adjustment to the new regulatory area.

The last case is private debt, which is a nearly $500bn asset class and one of the most intriguing in the investment arena. Private debt is looking to capitalise new opportunites created by the global economic outlook and offers investors an amazing tool for diversification and downside protection as it is collateralised by real assets. Due to the nature of business, investors know what to expect in terms of returns and the asset class is growing steadily alongside the investor appetite as seen below.

Figure 3. Long-term Investors' Intentions For Their Private Debt Allocations, Source: Preqin Private Debt 2016

What comes as big surprise is the appetite in Europe for private debt products and the regulation which is changing in favour of private debt managers in some countries, facilitating the loan origination from funds. The growing demand for private debt and especially direct lending funds has a solid rationale behind it and this is Basel III for banks and Solvency II for insurance companies. Despite the incentives from EU politicians to boost banking lending, corporations appear to seek alternative financing highlighting the decreased need for bank loans. Under regulatory capital considerations, like RWA for banks and solvency capital for insurers, lending to SME and lower middle market is prohibitive due to increased capital requirements.

Figure 4. Need For Bank Loans In The Euro Area From 2009 To 2015H1, Source: ECB Data Warehouse

The above figure indicates the change of landscape in corporate financing in the Euro area and welcomes the rise of direct lending funds, which appear to be extremely successful in fundraising as seen below.

Figure 5. Direct Lending Fundraising: North America vs. Europe Funds, 2006 - 2016 April, Source: Preqin Private Debt Report 2016

Potential comeback from banks regarding lending especially in the SMEs area could only prove beneficial for the direct lending arena, because it will help the asset class become bigger, more competitive and sustainable. Apart from banks and insurers, pension funds could find a great fit for their asset liability matching portfolios due to the illiquidity of several private debt funds, which is a crucial consideration due to the risky nature of this business. The Dodd-Frank Act and AIFMD provide investors with confidence when it comes to investing in such funds due to the stringent compliance and risk management rules.

Private debt is positioned strategically somewhere in the middle field between the battling alternative asset classes of hedge funds on one side, with mostly up to monthly liquidity for single managers and up to quarterly for fund of hedge funds, and illiquid private equity on the other side, with typical 5, 7 and 10 year terms plus potential yearly extensions e.g. in real estate. The fee model is lower than the 2/20 in hedge funds and private equity and more tight to the long only fixed income fund space with performance fees. In general, we recognise a melting pot of alternatives and particularly private debt and direct lending strategies demonstrate how hedge funds and private equity are growing together. Mostly long only, un-levered and with low volatility, those strategies seem to assist family offices, fund of funds and slowly as well institutionals like pensions, insurers and sovereign wealth in the search for yield. Most of the largest GPs in PE have long opened private debt strategies and various credit and high yield related hedge funds started direct lending into corporates, speciality finance, trade finance, consumer credit and real estate. Extensive due diligence is required in analysing direct lending strategies, as not only the underlying lending activity to individual, firm or transaction, but as well the level of debt as LTV and the seat in the capital structure from senior secured, mezzanine, convertible, unittranche or preferred equity requires dedicated credit experience and structuring capabilities combined with extensive risk management, credit scoring, restructuring and workout experience. Plenty of direct lenders do not posses a credit scoring mechanism, are unregulated as no formal registration is yet required and particularly in the online peer-to-peer (P2P) and marketplace lending space follow 'no cherry picking' policies from senior management down to the credit analysts. Those policies combined very low decline rates of loan applications - meaning almost every applicant gets a loan - lead to volume based lending practices, in part comparable with with pre-crisis 'originate-to-distribute' subprime mortgage lending, but now from non-bank lenders in the shadow banking system. Certain direct lending strategies provide liquidity like hedge funds and face an underlying asset and liability mismatch in their portfolios. In stressed markets, investors will want to redeem their investments according to liquidity provision in the fund prospectus, but will likely have to queue with their peers until GP's have liquidity available. The direct lending market has risen 100-150% p.a. since 2009 on both sides of the Atlantic and a recent resurrection of bank senior loan provision to lending funds combined with the securitisation of marketplace and P2P loans in the US and Europe for funding purposes, with the engagement of tier 1 rating agencies, seems like a recipe for upcoming stress in this industry. From an investor perspective, private debt and direct lending are welcome sectors with high yielding and low volatility strategies. Extensive investment and operational due diligence is required in order to survive periods with stressed solvency levels during the next credit cycle turn, as the direct lending space has not yet been tested in a downward credit market.

This perspective aims at analysing three of the major asset classes inside the alternative investment space, which provide investors with options for diversification and return enhancement amid a changing and low-yielding economic environment. This analysis will be different if the upcoming political scenery changes with specific mentioning of a potential Brexit.