Recep Tayyip Erdogan believes high interest rates are the cause of inflation, not the remedy for it.

MANY of the most famous hedge-fund trades have been bets that things were about to go wrong. Think of Enron’s bankruptcy or the souring of subprime mortgage bonds in America. The best trade made by “the Professor” was very different. It was a bet that something was starting to go right.

A visit almost 20 years ago convinced him that Turkey was serious about fixing its economy. The yield on its one-year Treasury bills was then above 100%. “It was a serious mispricing,” he tells Steven Drobny in “The Invisible Hands”, a book of interviews with pseudonymous hedge-fund managers. The IMF gave its approval to Turkey’s reforms soon afterwards. The price of T-bills surged. The one-year interest rate fell to 40%.

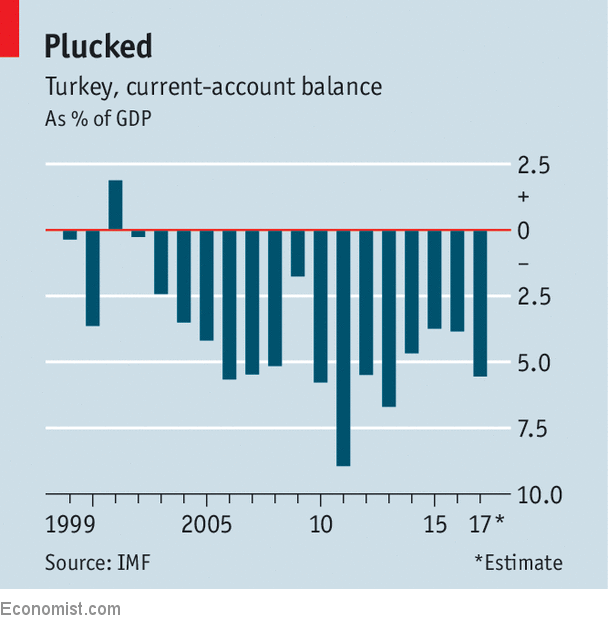

The wheel has since turned almost full circle for Turkey, which now seems to attract more sellers than buyers. The lira is sinking. S&P has cut the country’s credit rating from junk to junkier, partly because of concerns about its reliance on foreign capital. The deficit on its current account, a broad measure of trade, is one of the largest in the world. To bridge that gap, Turkey’s banks and big firms have borrowed heavily, often in foreign currency. Its tarnished credit rating is a hint that those debts may not be paid back in full.

It is tempting to see Turkey as a morality tale for emerging markets. Just as the sound policies of the early 2000s were rewarded by rising incomes, the reckless borrowing of recent years must soon be punished by a deep recession, the reasoning goes. Yet the wonder is not that Turkey is skirting the edge of a crisis, but that it has managed to avoid one for so long.

To understand how, start by going back to when the smart money was betting on Turkey. The IMF blessing that made the Professor money was a staging-post on the way to more profound changes. In 2001 Kemal Dervis, a former World Bank official, became the country’s economy minister. He negotiated a big loan from the IMF to create breathing-space. The central bank was made more independent, putting an end to the monetary financing of public spending. The lira was allowed to float. When Recep Tayyip Erdogan became prime minister, in 2003, his government stuck with the programme.

The economy flourished, but a big weakness remained. As in many countries with a history of high inflation, savings in Turkey are low. When the economy picks up, foreign capital is needed to sustain the momentum. The country’s foreign debts have steadily mounted. To make matters worse, the policy orthodoxy of the early 2000s has been called into question. Almost everyone thinks rising inflation in Turkey is a sign that interest rates are too low. Mr Erdogan, however, believes high interest rates are the cause of inflation, not the remedy for it. His efforts to bully the central bank into seeing things his way have been unsubtle—and successful.

There is a trace of hubris in all this. When Mr Erdogan holds forth on his theory of interest rates, he sounds as if he believes it. In this regard, and others, he fits the paradigm of “economic populism” sketched out in 1990 by Sebastian Edwards and the late Rudiger Dornbusch. This approach downplays or denies the notion that budget deficits or inflation are constraints on economic growth. The Latin American populists of the 1970s and 1980s printed money to pay for public-spending sprees, only to find (after a brutal crisis) that the constraints were binding, after all. As Dani Rodrik of Harvard University has noted, Turkey is a variant on this theme. It has relied instead on capital inflows to fund private-sector excess.

A decade of low inflation, easy money and surplus saving worldwide has kept the credit line open. That is how the Turkish economy has avoided a reckoning for so long. The forbearance of foreign investors will not last for ever. Indeed, many think that a resurgent dollar and rising bond yields in America will end it. Yet Turkey has emerged unscathed from similar tight spots in the past. Perhaps its frailties are now so well-documented that they no longer seem worrying.

If Turkey is a parable of easy money, its lessons cannot readily—or can no longer— be generally applied to emerging markets. Current accounts have, by and large, moved towards balance, meaning most of them are less reliant on foreign borrowing. Turkey’s double-digit inflation stands out because low single-digit inflation has become the norm. Indeed, the approach to monetary policy in emerging markets is, bar a few renegades, rigidly orthodox. That is why bets of the kind the Professor made almost two decades ago have become so rare.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.