Harnessing the motherlode of the sun’s power is almost within our reach.

The sun, our primary source of energy, bathes our Blue Planet in more solar energy than we can ever hope to reasonably use. Each hour, the sun sends 430 quintillion Joules of energy our way, more than the 410 quintillion Joules that humans consume in a whole year. With the sun likely to be around for another five billion years or so, we have a virtually unlimited source of energy--if only we could tap it efficiently.

Unfortunately, we are currently only able to harness a minuscule amount of this energy due to technical limitations.

But that could be about change, thanks to advances in one wonder-crystal--perovskite.

The U.S. Department of Energy’s (DOE’s) National Renewable Energy Laboratory (NREL) has forged a public-private consortium dubbed the US-MAP for US Manufacturing of Advanced Perovskites Consortium, that aims to fast track the development of low-cost perovskite solar cells for the global marketplace.

Silicon Panels

According to the IEA, solar power supplied just 592GW, or a mere 2.2%, of the world’s 26,571GW in electricity consumption in 2018. That was after an impressive 20% growth in global PV installations to the tune of nearly 100GW.

More than 90% of those photovoltaic (PV) panels installed were constructed from crystallized silicon.

Silicon panels have their advantages: They’re quite robust and relatively easy to install. Thanks to advances in manufacturing methods, they’ve become quite cheap over the past decade, particularly the polycrystalline panels constructed in Chinese factories.

However, they have one major drawback: Silicon PV panels are quite inefficient, with the most affordable models managing only 7%-16% energy efficiency depending on factors like placement, orientation, and weather conditions. Si panels are wafer-based rather than thin-film, which makes them sturdier and durable, but the trade-off is a sacrifice of efficiency.

To meet the world’s rapidly growing energy appetite--and achieve the kind of de-carbonization goals that would help slow the impact of climate change--it would take hundreds of years to build and install enough silicon PV panels.

This is way too slow, given that we have a mere 10-year window to act to avert irreversible and catastrophic climate change.

More critically, the best (and most expensive) silicon panels to-date boast an efficiency rating maximum efficiency rating of 26.7%, pretty close to the theoretical maximum of 29.1%.

For years, scientists have experimented with alternative crystal formations that would allow panels of similar size to capture more energy. Until now, few designs emerged that were commercially viable, particularly thin-film cells that could theoretically achieve much higher levels of efficiency.

Thin-film PV panels can absorb more light, and thus produce more energy. These panels can be manufactured cheaply and quickly, meeting more energy demand in less time. There are a few different types of thin-film out there, all of them a little different from standard crystalline silicon (c-si) PV panels.

Amorphous silicon (a-Si) panels are the oldest form of thin-film: a chemical vapor deposits a thin layer of silicon onto glass or plastic, producing a low weight panel that isn’t very energy efficient, managing 13.6%. Then there are cadmium telluride (CdTe) panels, which uses the cadmium particle on glass to produce a high-efficiency panel.

The drawback there is the metal cadmium, which is toxic and difficult to produce in large quantities.

These panels are usually produced using evaporation technology: the particles are superheated and the vapor is sprayed onto a hard surface, such as glass. They are thin, but not as dependable or durable as c-si panels, which currently dominate the market.

NREL Perovskite Breakthrough

Perovskite has now managed to break the efficiency glass ceiling.

Perovskites are a family of crystals named after Russian geologist Leo Perovski, “perovskites.” They share a set of characteristics that make them potential building blocks for solar cells: high superconductivity, magnetoresistance, and ferroelectricity. Perovskite thin-film PV panels can absorb light from a wider variety of wave-lengths, producing more electricity from the same solar intensity.

In 2012, scientists finally succeeded in manufacturing thin-film perovskite solar cells, which achieved efficiencies over 10%. But since then, efficiencies in new perovskite cell designs have skyrocketed: recent models can achieve 20%, all from a thin-film cell that is (in theory) much easier and cheaper to manufacture than a thick-film silicon panel.

At Oxford University, researchers reached 25% efficiency; a German research team has achieved 21.6%, while a new record was set in December 2018, when an Oxford lab reached 28% efficiency.

The National Renewable Energy Laboratory NREL has been able to build composite Silicon-Perovskite cell by putting perovskites atop a silicon solar cell to create a multijunction solar cell, with the new cell boasting an efficiency of 27% compared to just 21% when only silicon is used.

But perhaps more significant is that the organization has been able to boost the longevity of Perovskite solar cells by altering their chemical composition to overcome light-induced phase-segregation-- a process through which the alloys that make up the solar cells break down when exposed to continuous light.

Low-Cost Perovskite Panels

Solar power has become more affordable, accessible, and prevalent than ever before thanks to technology improvements, competitive procurement, and a large base of experienced, internationally active project developers.

According to the International Renewable Energy Agency (IRENA), solar power generation is now fully competitive with fossil fuel power plants, with the global weighted average levelized cost of electricity (LCOE) for utility-scale solar PV cells having declined 75% to below USD 0.10/kWh since 2010.

Source: IRENA

However, there’s still work to be done.

At an LCOE of $0.085/kWh for photovoltaic cells and $0.185/kWh for concentrating solar projects, solar power(utility-scale + residential rooftop) remains more expensive than other renewable sources including hydro, onshore wind, geothermal and bioenergy.

US-MAP plans to solve issues mainly regarding manufacturing and durability and also tackle sustainability issues mainly relating the use of lead and other metals. The consortium will focus on funding from federal sources and also explore private-sector financing.

Hopefully, it will be able to make this IEA prediction a reality by making solar power one of the cheapest, if not the cheapest, ways to generate electricity by 2025.

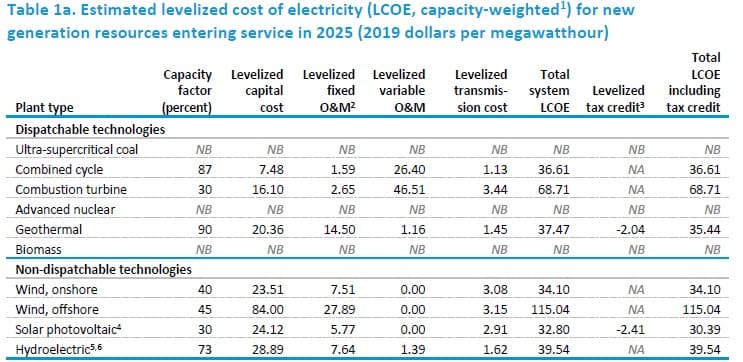

The capacity-weighted average is the average levelized cost per technology, weighted by the new capacity coming online in each region. The capacity additions for each region are based on additions from 2023 to 2025. Technologies for which capacity additions are not expected do not have a capacity-weighted average and are marked as NB, or not built.