…and why it might not fall by very much soon

PERHAPS the most vexing thing for those watching the oil industry is not the whipsawing price of a barrel. It is the constant updating of theories to explain what lies behind it. In March 2014, when the price of a barrel of Brent crude was in three figures, the then boss of Chevron, an oil giant, observed that the scarcity of cheap oil meant “$100 per barrel is becoming the new $20”. Two years later, when the oil price slumped below $28, the talk was of a global oil glut caused by the furious efforts of the OPEC cartel to regain market share. Now that oil prices have tested $70, analysts are again scratching their heads.

In “1984”, George Orwell coined the term “doublethink”, the ability to believe two contradictory things. Oil analysis seems to require similar cognitive gymnastics. Three big questions arise. First, why has the oil price more than doubled in the space of two years, against all expectation? Second, why has this surge been met with cheers from global stockmarkets and not concern for the world economy? Lastly, where might the oil price eventually settle?

tart with the journey to $70. The slump in prices two years ago was in part a response to weak demand—with the fragility of China’s economy a big concern—and in part to abundant supply. Few believed then that OPEC would, or even could, cut output. Saudi Arabia, the world’s largest oil exporter, appeared to have every reason not to. Plentiful oil supply would check the growth of the shale-oil industry in North America. It would also stymie Iran, its bitter rival, which was back in the market following the lifting of sanctions.

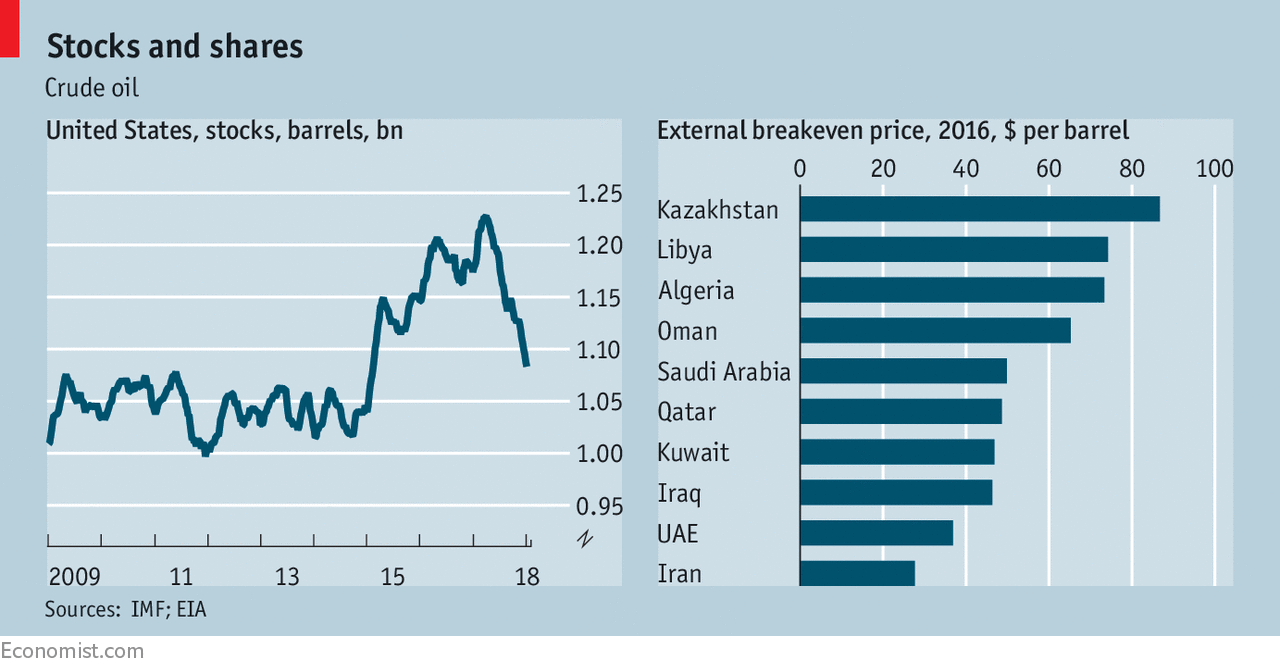

Yet demand recovered quickly. China pepped up its economy with faster credit growth and other fillips to spending. Commodity prices surged. Within months clear signs of a broad-based global economic upswing were palpable. And OPEC proved better able to curb production than anyone had imagined. A deal reached in November 2016 to restrict output had little immediate effect but by late last year started to pay off. Oil stocks fell, notably in America (see left-hand chart). Demand was outstripping supply. Prices duly rose.

It is still surprising they have risen so far. Higher prices are often blamed in part on the messy politics of the Middle East. The usual worries are there but “there has been no impact on physical supply,” says Martijn Rats of Morgan Stanley. Shale was also seen as the oil industry’s flexible response to price signals. Too high, and the wildcatters in Texas would drill for fresh supply. But small producers are showing a new restraint, because their financiers want greater focus on profits and less on output. And it takes several months from drilling wells for oil to come on-stream.

The financial markets show little sign of anxiety about the oil-price surge. Stockmarkets remain buoyant, which is itself another puzzle. Since the oil shocks of the 1970s, markets have associated a sudden run-up in oil prices with economic calamity. The world is both producer and consumer of oil, so in principle the overall effect of oil-price increases is neutral. But in practice, the net impact had been to reduce global demand, because oil exporters in the Middle East tended to save a big chunk of the windfall income they gained at the expense of oil consumers in the West.

Over time, however, the rich world has become less reliant on oil. Demand in America peaked in 2005, for instance. Meanwhile, oil exporters became ever more dependent on high oil prices to pay for lavish government budgets and imported consumer goods. Most of the big oil producers in the Middle East need an oil price above $40 to cover their import bill (see right-hand chart on previous page).

In this new arrangement, dearer oil is both far less damaging to rich-world consumers and soothes the strained finances of the big oil exporters, not just in the Middle East but in Africa, too. For all the other trouble-spots, investors seem to find the world economy a safer place. And they have other reasons to feel cheery. The shale industry means that dearer oil is a shot in the arm for investment in America, which adds to GDP growth. And a rising oil price is taken as a sign of healthy growth in China, the world’s biggest oil importer.

Beneath the dramatic ups and downs in the oil price and its changing influence on the world economy are some big themes: the rise of the shale-oil industry and how OPEC responds; the dependence of the big oil exporters in the Middle East on high oil prices; the peak in oil demand in America and eventually elsewhere. These forces will have a big say in where oil prices eventually settle.

How they will play out is the subject of a new paper by Spencer Dale, chief economist of BP, another oil giant. The critical change in the oil market, he argues, is from perceived scarcity to abundance. When oil was considered scarce and expensive to find, it seemed wise to ration it. It was more like an asset than a consumer good: oil in the ground was like money in the bank. But new sources of supply, such as shale oil, and improved recovery rates of existing reserves, along with the emergence of mass-market electric vehicles, have changed the reckoning. There is a fair chance that much of the world’s recoverable oil will never be extracted, because it will not be needed. It thus makes sense for the five big producers in the Middle East (Saudi Arabia, UAE, Iran, Iraq and Kuwait), which can extract oil for less than $10 a barrel, to undercut high-cost producers and capture market share while the demand is there. The financial logic has changed to “better to have money in the bank than oil in the ground,” notes Mr Dale.

Does that mean oil prices are poised to plummet? Probably not, unless shale producers ramp up output again. The peak in global oil demand might be decades away, argues Mr Dale, and it will not tail off sharply. And for now, the big oil exporters cannot sustain very low oil prices for long. Their “social cost” of production, taking in government spending reliant on oil revenue, is about $60 a barrel on average. Sustaining an oil price close to the cost of extraction will require reforms, which do not usually happen quickly. Translated into doublespeak: oil prices are too high; but they may not fall, in large part because big oil producers have got used to them.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.