Perennial domestic weakness, and America’s recent protectionist turn, make it hard for India to sell more abroad.

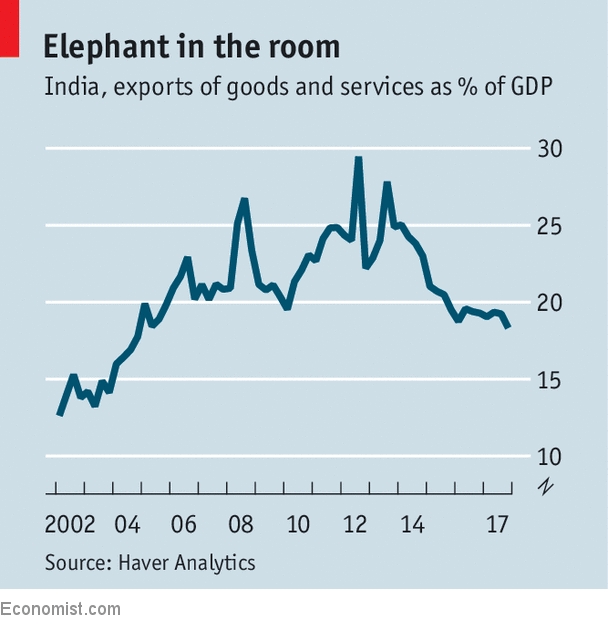

IN THE spring of 1991, Indian officials desperate to fend off a balance-of-payments crunch secretly airlifted 20 tonnes of gold confiscated from smugglers into the vaults of UBS, a Swiss bank. That crisis prompted liberalising reforms that helped integrate India into the global economy. By 2013 India’s exports as a percentage of GDP had nearly quadrupled, to over 25%, not far from the global average. But an exporting funk since then has pushed the figure to its lowest level in 14 years. Paired with a rise in imports, the trend has revived questions about the competitiveness of Indian firms—if not the government’s ability to finance a growing current-account deficit.

A repeat of the 1991 drama is not in the offing. India’s economy today is growing at a world-beating pace. Its central bank holds enough foreign reserves to pay for nearly a year’s worth of imports. Foreign investors are on hand to finance both government and corporate borrowing. Yet economists are left pondering why India has been unable to boost exports even as the global economy has purred along.

In the 12 months to March 2018, $303bn of Indian goods ended up overseas. That was up on the previous year, but still short of the $310bn achieved in 2014, when the Indian economy was a quarter smaller. Imports, meanwhile, have increased to $460bn, pushing the merchandise deficit to $157bn last year, up from $109bn in 2016-17 and its highest level in five years. A surplus in services such as IT outsourcing helps reduce the overall trade deficit by around half, but even there imports are growing faster than exports.

The shortfall is swollen by the rising price of oil, lots of which India imports (and some of which is also sold on as refined products). The surge from around $30 per barrel in early 2016 to over $70 now goes a long way to explaining the rise in India’s current-account deficit, which is expected to reach 2% of GDP this fiscal year, triple last year’s reading. Gold imports, used for saving or jewellery, have their own unpredictable rhythms, but also deepen the deficit.

The current trade lull extends beyond gold and oil, however. Exporters across the economy are being squeezed by the poor implementation of a goods-and-services tax that came into force last July. Perhaps 100bn rupees ($1.5bn) of refunds due to exporters once they can prove they have shipped their wares abroad is being held up by sclerotic administration. That is working capital which small-time exporters cannot easily replace.

Worse, a $2bn suspected fraud by a diamond dealer in February has resulted in regulators banning certain types of bank guarantees that exporters use to ensure they get paid promptly, exacerbating their funding problems. These snafus come as many firms are still recovering from the ill-advised “demonetisation” of November 2016, when most banknotes were taken out of circulation overnight. The move snagged local supply chains, giving foreign rivals opportunities to fulfil orders that would have gone to hobbled Indian firms and to gain market share in India itself.

Those woes come on top of perennial frailties. Crippling red tape means most Indian firms are small: the country lacks the mega-factories hosting thousands of workers making T-shirts or mobile phones that are common elsewhere in Asia. All but a few firms lack the heft to participate in global supply chains. A relatively strong rupee in recent years has not helped.

Unwilling to enact labour and land-acquisition reforms that might foster larger firms, the Indian government is instead shielding its industry from foreign competition. In recent months it has imposed tariffs on a dizzying array of goods, from mobile phones to kites. Though those will no doubt help stymie imports, it is just as likely that trade measures imposed by other governments will hobble India’s exports.

For it is India’s misfortune that Donald Trump’s America is its biggest source of trade surpluses. Mr Trump’s administration has multiplied the salvos against India, whether decrying supposed export subsidies, making it harder for Indian IT workers to get visas or accusing India of artificially weakening its currency. Unlike many American allies, India has not been exempted from imminent steel tariffs.

India would be seriously damaged by any further escalation in trade conflicts. It needs hard currency from exports not only to finance imports and economic growth, but also to repay external debts. These have swelled to around $500bn, or roughly a fifth of GDP, more than 40% of which is due in less than a year. Economists at DBS, a bank, say that this, together with India’s trade slump, has put “external financing risks back on the radar”. Keen to woo the investors it needs to fill the gap between exports and imports, India recently made it easier for outsiders to buy short-dated bonds, a move it had previously resisted for fear that investors might pull out suddenly if sentiment turned.

In a benign global macroeconomic environment, none of this matters too much. But investors’ appetite for funding emerging-market deficits ebbs and flows. A previous bout of monetary-policy tightening in America in 2013 led to a “taper tantrum” in which money rapidly sloshed out of emerging markets. India used to be shielded from such turns in global sentiment. But its poor trade record means it is becoming more exposed.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.