IT IS clear whom President Donald Trump blames for the Middle East’s problems. Iran’s “corrupt dictatorship”, he told the UN General Assembly on September 25th, “sows chaos, death and disruption” in the region. It used the economic benefits of its deal with America and other world powers, which curbed Iran’s nuclear programme in return for sanctions relief, to raise military spending and support terrorism, he claimed. So his administration pulled America out of the deal in May and launched “a campaign of economic pressure to deny the regime the funds it needs to advance its bloody agenda.”

Iran has responded, as usual, with defiance. Hassan Rouhani, its president (pictured), insisted he would not meet Mr Trump, denounced his “xenophobic tendencies resembling a Nazi disposition” and predicted victory over America. “The end of this war will be sweeter than the end of the eight-year war,” said Mr Rouhani, referring to Iran’s war with Iraq in the 1980s which left 600,000 Iranians dead. Though considered a pragmatist, he sounds much like Iran’s hardliners, who opposed his nuclear deal and see no room for compromise with America.

Mr Trump, though, is not the only one challenging the regime. Several gunmen killed at least 25 people, including 12 members of the Islamic Revolutionary Guard Corps (IRGC), the regime’s praetorian guard, at a military parade in Ahvaz, a city in the south-western province of Khuzestan, on September 22nd. Two different groups claimed responsibility. The first was a splinter of a local Arab separatist group, the Arab Struggle Movement for the Liberation of Ahvaz. But the Islamic State group, which a year ago stormed Iran’s parliament in Tehran, then promptly claimed the attack too, perhaps lying to boost its stature. The regime quickly, and with no hard evidence, blamed America and its regional “puppets”—Saudi Arabia, the United Arab Emirates (UAE) and Israel.

Iranian officials are fond of lurid conspiracy theories, but it is not hard to see why they suspect outsiders. Khuzestan is home to some 2m Arabs (most Iranians are Persian). In recent years Arab broadcasters have ramped up coverage of Iranian minorities, keenly supporting Arabs “under occupation by Persian forces”. Bahrain has gone as far as to name one of its streets “Arabian Ahvaz Avenue”. One of the groups that claimed responsibility for the attack did so through Iran International, a television station based in Britain and funded by Saudi investors. Last year Muhammad bin Salman, Saudi Arabia’s crown prince and de facto ruler, promised to take his country’s fight “inside Iran”.

In Iran’s eyes this Arab offensive is part of a broader, ominous front. Saudi Arabia and the UAE have set aside their differences with Israel in order to counter Iran, a shared enemy. Meanwhile, the White House is now full of officials who have spent much of their careers calling for regime change in Iran. Some senior members of Mr Trump’s team have supported the Mujahideen-e-Khalq, a cult-like dissident group that was until recently considered a terrorist organisation in Europe and America, and even provokes revulsion among reform-minded Iranians. Rudy Giuliani, Donald Trump’s lawyer, has taken the group’s cash; John Bolton, Mr Trump’s national security adviser, has hailed it as Iran’s “viable opposition”. On September 23rd an illustrious group of former American officials warned that Iran was being unwisely forced to choose between “capitulation or war”.

Iran’s sense of siege is likely to grow. On November 4th America will impose new sanctions aimed at Iran’s oil industry. As a result, Japan, South Korea, Sri Lanka and European countries plan to slash oil imports from Iran. America might offer cheap oil from its own reserves to induce India to follow. Though European states continue to uphold the nuclear deal, some have left Iran to twist in the wind. A French state-owned bank has dropped plans to finance exports to Iran, while the French government has restricted diplomatic travel to Iran and suspended the appointment of a new ambassador. Iran is seeking help from Russia and China. But Russia has gleefully filled the gap left by Iran in the oil market, while China is focused on its trade war with America.

The government’s focus on foreign plots deflects attention from problems at home. Khuzestan holds the vast majority of the country’s oil reserves but is poor and neglected. Arabs say they are kept out of local government and that the IRGC steals the region’s water as well as its oil. A plethora of dams have diverted rivers that flowed to the Gulf from central Iran, turning Khuzestan into a dust bowl. Protests have been brutally suppressed. Groups vowing to “liberate” Ahvaz claim to sabotage pipelines and shoot at officials.

The malaise is countrywide. Iran’s currency, the rial, has slumped in the past year. The poor, long the regime’s base of support, have to hoard food cans. Officials grow ever more corrupt to make up for the shrinking value of their salaries. Foreign businessmen, who flocked to Iran after the nuclear deal, have left. This year’s intake at the French school in Tehran was down from 350 to 150. Many Iranians want out, too. Such is the demand for work visas at the German consulate that applicants have to wait two years for an interview.

Years of sanctions have made Iran develop a “resistance economy”, which is diverse and in many areas self-sufficient. Prices of basics have risen, but by far less than they might have if Iran depended on imports. Cynics note that although the falling rial makes people poorer, it makes the government stronger, since Iran earns its oil revenue in foreign currency. Its reserves can survive two more years of Mr Trump, says Mr Rouhani. But suffering Iranians may prove a bigger threat to the regime.

Mining grew by 6.3 percent year-on-year (y-o-y) in the first quarter of 2018, according to data issued by the General Authority for Statistics on July 2.

Coupled with expansion in non-oil manufacturing (4.6 percent) and government services (3.4 percent), the strong performance of the mining sector helped drive overall GDP growth to 1.2 percent over the period, breaking a run of four consecutive quarters of negative growth.

The industry also helped offset slower growth in the oil industry (0.6 percent), along with contractions in retail and hospitality (-0.5 percent) and construction (-2.4 percent).

Private investment to boost mining contribution

The expansion in mining activity comes amid a push to attract private investment into the sector to further develop it as one of the main contributors to the economy.

On July 9 Khalid Al Falih, the minister of energy, industry and mineral resources, announced the completion of an adjusted mining investment system designed to incentivize investment in projects.

Under the revised mechanism, the Kingdom aims to build a comprehensive database of its mineral resources, intensify exploration and develop new funding methods for projects.

The development aligns with the Kingdom’s Vision 2030 economic strategy, which looks towards greater private sector involvement to diversify the economy away from its dependence on hydrocarbons.

As for the extent of mining’s contribution, Al Falih said the government plans to make the sector the third pillar of the economy, alongside oil and downstream petrochemical production.

The Ministry of Energy, Industry and Mineral Resources (MEIMR) seeks to increase mining’s contribution to GDP from $17bn currently to $64bn by 2030, as well as generate more than 25,000 new jobs in the industry.

Strong mineral reserves strengthen prospects

The pursuit of these goals is likely to be supported by high levels of mineral deposits: the MEIMR estimates the Kingdom’s mineral wealth at around $1.3trn, with gold reserves put at $240bn and significant deposits of bauxite, copper and phosphates.

This figure could rise further as more survey work is undertaken. In February officials said the Saudi Geological Survey had at least five more years of testing to undertake to identify and quantify new deposits.

Rising demand and commodity prices could make the country’s mining sector an attractive buy, with leading local extractor the Saudi Arabian Mining Company (Ma’aden) experiencing higher returns this year. Half-yearly results showed an 82.9 percent y-o-y rise in net profits to SR1.2bn ($320m), and the company cited an increase in sales volume and mineral prices as factors underpinning growth.

One commodity that Ma’aden is looking to develop is copper, according to Darren Davis, the company’s acting CEO.

“We would like to be a lot bigger in copper,” he told international media on August 6. “We think it is a great metal for the future.”

While looking at buying into assets overseas, Davis said Ma’aden wanted to build on its existing domestic copper operation, which currently consists of a single mine located 350 km south-east of Jeddah that began production in 2016.

Mining growth to spur development in related industries

Continued expansion in the mining industry is expected to present growth opportunities to firms operating in related sectors, with the expected quadrupling of mining’s economic output to require significant investment in dedicated infrastructure, equipment and technology.

While Saudi Arabia is investing extensively in its rail network, providing heavy-moving capacity and linking its mineral reserves with ports and logistics hubs, demand for earth moving and loading equipment, engines and rail rolling stock for moving the take from the new mines is set to rise sharply in the coming years.

In mid-May Saudi-U.S. rail services joint venture Savage Saudi Arabia delivered five new locomotives and two locomotive booster units to Ma’aden’s Wa’ad Al Shamal Phosphate Company, to be used to move mining offtake to the industrial towns of Wa’ad Al Shamal and Ras Al Khair.

Mooncakes are a useful indicator of trends, from consumption to corruption

MOONCAKES are among the most divisive treats. For some the chewy pastries are delicacies on which to gorge for the Mid-Autumn Festival, a Chinese holiday that falls this year on September 24th. For others they are dry, dense and full of calories. But for economists they are something else entirely: an indicator of important trends in consumption, innovation, corruption and grey-market trading.

Mooncakes play this role because of their status as gifts. Ahead of the mid-autumn holiday, companies give them to employees; business contacts exchange them. Consumption of mooncakes is thus less a reflection of whether people enjoy the pastries, likened by some to edible hockey pucks, and more a measure of the health of the economy. So it is heartening to know that, amid rising trade tensions with America, the Chinese bakery association has forecast that sales of mooncakes will rise by a solid 5-10% this year.

Some observers fret that Chinese consumers, burdened by rising debt, have started opting for cheaper goods. But consumers still plump for more expensive varieties of mooncakes rather than the classic nut-and-egg-yolk fillings. Shangri-La, a five-star hotel chain, has won fans with its blueberry-cheese mooncake (dismissed by traditionalists as cheesecake). Judging by long queues at Häagen-Dazs stores, mooncake-shaped ice-cream sandwiches are also booming. At least 30 listed food companies, more than ever before, are vying for a bite of the $2bn mooncake market this year.

Mooncakes have long given off a whiff of corruption. Businesses seeking favours from officials send lavishly wrapped boxes of them. When Xi Jinping, China’s powerful president, intensified his anti-graft campaign in 2013, the mooncake market shrank by more than 20%. A rebound over the past three years has naturally fuelled talk of a rebound in bribery, too. The government has denied this. Yet it is clearly worried. The front page of the newspaper published by the Communist Party’s anti-graft agency warned on September 17th that although mooncakes are small, they can point to much bigger problems.

Perhaps the tastiest morsel from mooncakes is what they reveal about China’s grey economy. Scalpers hawking mooncake gift coupons have taken to Shanghai’s streets in recent days, as they do every year, standing outside busy subway stations and popular bakeries. Most economic studies describe scalping as a phenomenon that arises when scarce tickets to sporting events or concerts are resold at a hefty markup. Yet there is no shortage of mooncakes in China. The problem is inefficient allocation: too many coupons are given to people who do not like them. China’s economy has plenty of inefficiencies, whether in the form of state-owned companies or gift-giving customs. But it sometimes also has solutions.

Currencies and stockmarkets have tumbled, though growth rates are solid

THERE are many ways to defend a currency. Ayam Geprek Juara, an Indonesian restaurant chain that serves crushed fried chicken, has offered free meals this month to customers who can show they have sold dollars for rupiah that day. The restaurant has provided more than 80 meals to these “rupiah warriors”, according to Reuters, a news agency.

Perhaps it should extend the offer to the staff of Bank Indonesia, the country’s central bank, which is only about 20 minutes away from one of the restaurant’s branches. To defend the rupiah, it has been selling billions of dollars of foreign-currency reserves, which have fallen from over $125bn in January to less than $112bn in August. Despite these sales, and four interest-rate rises since May, the rupiah has lost almost 10% of its value against the dollar this year, returning to levels last seen during the Asian financial crisis of 1997-98.

India’s rupee has fared even worse, reaching a record low against the dollar. And even where Asia’s currencies have remained steady, its stockmarkets have faltered. Hong Kong’s Hang Seng index fell by 20% from late January to September 12th, meeting one definition of a “bear market”. Mainland China’s markets are struggling.

A person returning from Mars would assume that something horrible had happened in the region, says Chris Wood of CLSA, a brokerage. But in fact Asia’s emerging economies are enjoying a happy spell of respectable growth and stable consumer prices. Only Pakistan has a combined trade and fiscal deficit as devilish as Turkey’s or Argentina’s. And not even Pakistan has anything like their double-digit rates of inflation. India’s GDP grew by over 8% last quarter, compared with a year earlier. Indonesia’s expanded by over 5% (as it almost always does). And China’s grew by over 6% (as it always does). Nor is a widespread slowdown expected this quarter.

The trade war has soured the mood in China and Hong Kong. But China’s exports to America still grew by over 13% in August, and the Canton trade fair was at its busiest for six years, according to the Institute of International Finance, an industry group. Many American customers are obviously keen to shop before the broader tariffs take effect. Some of China’s neighbours, especially Vietnam, believe they can win the trade war by taking in its refugees: the manufacturers that move out of China to escape tariffs.

India and Indonesia are largely insulated from the trade war, thanks to the strength of their domestic demand. But that same strength leaves them exposed to two other dangers—the higher oil price and America’s remorseless monetary tightening. India’s oil-import bill for the past five months was more than 50% higher than a year ago. Its current-account deficit could widen to 3% of GDP this fiscal year (which ends in March), according to some forecasts. Indonesia’s could expand similarly.

These gaps would be easy to finance if foreign investors were in an indulgent mood. But they are not. As American interest rates have risen, emerging markets have looked less rewarding and more dangerous by comparison.

In response India’s government is tweaking taxes and regulations to attract more foreign capital and fewer foreign goods. It will, for example, suspend a tax on rupee-denominated “masala” bonds sold outside India. It has also decided to curb imports of inessential items, without yet specifying what those may be.

In Indonesia the government is encouraging state firms to dilute imported fuel with biodiesel, extracted from local palm oil. It has delayed big infrastructure projects. And it has increased import tariffs on over 1,000 goods, including perfume, stuffed toys and tomato ketchup. The life of a rupiah warrior is not without sacrifices.

In theory, such ad hoc measures should be redundant in two economies that have embraced flexible exchange rates. If the trade deficit is unsustainable, a floating currency is supposed to weaken, thereby discouraging imports (and encouraging exports) automatically. By this logic, the declining rupee and rupiah will eventually resolve the problem they reflect.

But Indonesia worries that its foreign-currency debts will be harder to sustain with a weaker rupiah. These debts amount to about 28% of GDP, far below Turkey’s and Argentina’s totals, but are still too large to ignore. Moreover, about 40% of its rupiah-denominated government bonds are held by foreigners, according to Joseph Incalcaterra of HSBC, a bank. That “presents a sizeable outflow risk,” he says, which is one reason why Indonesia’s central bank has raised interest rates faster than India’s.

Both countries also worry that falls in the currency will beget further falls. After fighting the rupiah’s slide in 2013, Chatib Basri, Indonesia’s finance minister at the time, argued that a sharp drop in the currency would have revived memories of the crisis in 1997 and led to investor panic.

That wobble in 2013 followed some stray remarks from America’s Federal Reserve, which suggested it might soon slow its asset purchases. The subsequent spike in Treasury yields caused turmoil in emerging markets and threatened America’s fragile recovery, prompting the Fed to clarify and soften its position. The more recent increase in Treasury yields is different. It reflects a robust American expansion, reinforced by generous corporate-tax cuts. This time, there is little reason to expect a rethink at the Fed. America does not feel emerging markets’ pain.

Asia has long dreamed of “decoupling” from America so it can prosper even when the world’s biggest market does not. Instead, it is suffering even when America is not. And partly because America is not.

When I was young, there was nothing so bad as being asked to work. Now I find it hard to conjure up that feeling, but I see it in my five-year-old daughter. “Can I please have some water, daddy?”

“You can get it yourself, you’re a big girl.”

“WHY DOES EVERYONE ALWAYS TREAT ME LIKE A MAID?”

That was me when I was young, rolling on the ground in agony on being asked to clean my room. As a child, I wonderingly observed the hours my father worked. The stoical way he went off to the job, chin held high, seemed a beautiful, heroic embrace of personal suffering. The poor man! How few hours he left himself to rest on the couch, read or watch American football.

My father had his own accounting firm in Raleigh, North Carolina. His speciality was helping people manage their tax and financial affairs as they started, expanded, or in some cases shut down their businesses. He has taken his time retiring, and I now realise how much he liked his work. I can remember the glowing terms in which his clients would tell me about the help he’d given them, as if he’d performed life-saving surgery on them. I also remember the way his voice changed when he received a call from a client when at home. Suddenly he spoke with a command and facility that I never heard at any other time, like a captive penguin released into open water, swimming in his element with natural ease.

At 37, I see my father’s routine with different eyes. I live in a terraced house in Wandsworth, a moderately smart and wildly expensive part of south-west London, and a short train ride from the headquarters of The Economist, where I write about economics. I get up at 5.30am and spend an hour or two at my desk at home. Once the children are up I join them for breakfast, then go to work as they head off to school. I can usually leave the office in time to join the family for dinner and put the children to bed. Then I can get a bit more done at home: writing, if there is a deadline looming, or reading, which is also part of the job. I work hard, doggedly, almost relentlessly. The joke, which I only now get, is that work is fun.

Not all work, of course. When my father was a boy on the family farm, the tasks he and his father did in the fields – the jobs many people still do – were gruelling and thankless. I once visited the textile mill where my grandmother worked for a time. The noise of the place was so overpowering that it was impossible to think. But my work – the work we lucky few well-paid professionals do every day, as we co-operate with talented people while solving complex, interesting problems – is fun. And I find that I can devote surprising quantities of time to it.

What is less clear to me, and to so many of my peers, is whether we should do so much of it. One of the facts of modern life is that a relatively small class of people works very long hours and earns good money for its efforts. Nearly a third of college-educated American men, for example, work more than 50 hours a week. Some professionals do twice that amount, and elite lawyers can easily work 70 hours a week almost every week of the year.

Work, in this context, means active, billable labour. But in reality, it rarely stops. It follows us home on our smartphones, tugging at us during an evening out or in the middle of our children’s bedtime routines. It makes permanent use of valuable cognitive space, and chooses odd hours to pace through our thoughts, shoving aside whatever might have been there before. It colonises our personal relationships and uses them for its own ends. It becomes our lives if we are not careful. It becomes us.

When John Maynard Keynes mused in 1930 that, a century hence, society might be so rich that the hours worked by each person could be cut to ten or 15 a week, he was not hallucinating, just extrapolating. The working week was shrinking fast. Average hours worked dropped from 60 at the turn of the century to 40 by the 1950s. The combination of extra time and money gave rise to an age of mass leisure, to family holidays and meals together in front of the television. There was a vision of the good life in this era. It was one in which work was largely a means to an end – the working class had become a leisured class. Households saved money to buy a house and a car, to take holidays, to finance a retirement at ease. This was the era of the three-Martini lunch: a leisurely, expense-padded midday bout of hard drinking. This was when bankers lived by the 3-6-3 rule: borrow at 3%, lend at 6%, and head off to the golf course by 3pm.

The vision of a leisure-filled future occurred against the backdrop of the competition against communism, but it is a capitalist dream: one in which the productive application of technology rises steadily, until material needs can be met with just a few hours of work. It is a story of the triumph of innovation and markets, and one in which the details of a post-work world are left somewhat hazy. Keynes, in his essay on the future, reckoned that when the end of work arrived:

For the first time since his creation man will be faced with his real, his permanent problem – how to use his freedom from pressing economic cares, how to occupy the leisure, which science and compound interest will have won for him, to live wisely and agreeably and well.

Karl Marx had a different view: that being occupied by good work was living well. Engagement in productive, purposeful work was the means by which people could realise their full potential. He’s not credited with having got much right about the modern world, but maybe he wasn’t so wrong about our relationship with work.

MARX IS NOT CREDITED WITH HAVING GOT MUCH RIGHT ABOUT THE MODERN WORLD, BUT MAYBE HE WASN’T SO WRONG ABOUT OUR RELATIONSHIP WITH WORK

In those decades after the second world war, Keynes seemed to have the better of the argument. As productivity rose across the rich world, hourly wages for typical workers kept rising and hours worked per week kept falling – to the mid-30s, by the 1970s. But then something went wrong. Less-skilled workers found themselves forced to accept ever-smaller pay rises to stay in work. The bargaining power of the typical blue-collar worker eroded as technology and globalisation handed bosses a whole toolkit of ways to squeeze labour costs. At the same time, the welfare state ceased its expansion and began to retreat, swept back by governments keen to boost growth by cutting taxes and removing labour-market restrictions. The income gains that might have gone to workers, that might have kept living standards rising even as hours fell, that might have kept society on the road to the Keynesian dream, flowed instead to those at the top of the income ladder. Willingly or unwillingly, those lower down the ladder worked fewer and fewer hours. Those at the top, meanwhile, worked longer and longer.

It was not obvious that things would turn out this way. You might have thought that whereas, before, a male professional worked 50 hours a week while his wife stayed at home with the children, a couple of married professionals might instead each opt to work 35 hours a week, sharing more of the housework, and ending up with both more money and more leisure. That didn’t happen. Rather, both are now more likely to work 60 hours a week and pay several people to care for the house and children.

Why? One possibility is that we have all got stuck on a treadmill. Technology and globalisation mean that an increasing number of good jobs are winner-take-most competitions. Banks and law firms amass extraordinary financial returns, directors and partners within those firms make colossal salaries, and the route to those coveted positions lies through years of round-the-clock work. The number of firms with global reach, and of tech start-ups that dominate a market niche, is limited. Securing a place near the top of the income spectrum in such a firm, and remaining in it, is a matter of constant struggle and competition. Meanwhile the technological forces that enable a few elite firms to become dominant also allow work, in the form of those constantly pinging emails, to follow us everywhere.

This relentless competition increases the need to earn high salaries, for as well-paid people cluster together they bid up the price of the resources for which they compete. In the brainpower-heavy cities where most of them live, getting on the property ladder requires the sort of sum that can be built up only through long hours in an important job. Then there is conspicuous consumption: the need to have a great-looking car and a home out of Interiorsmagazine, the competition to place children in good (that is, private) schools, the need to maintain a coterie of domestic workers – you mean you don’t have a personal shopper? And so on, and on.

The dollars and hours pile up as we aim for a good life that always stays just out of reach. In moments of exhaustion we imagine simpler lives in smaller towns with more hours free for family and hobbies and ourselves. Perhaps we just live in a nightmarish arms race: if we were all to disarm, collectively, then we could all live a calmer, happier, more equal life.

But that is not quite how it is. The problem is not that overworked professionals are all miserable. The problem is that they are not.

Drinking coffee one morning with a friend from my home town, we discuss our fathers’ working habits. Both are just past retirement age. Both worked in an era in which a good job was not all-consuming. When my father began his professional career, the post-war concept of the good life was still going strong. He was a dedicated, even passionate worker. Yet he never supposed that work should be the centre of his life.

Work was a means to an end; it was something you did to earn the money to pay for the important things in life. This was the advice I was given as a university student, struggling to figure out what career to pursue in order to have the best chance at an important, meaningful job. I think my parents were rather baffled by my determination to find satisfaction in my professional life. Life was what happened outside work. Life, in our house, was a week’s holiday at the beach or Pop standing on the sidelines at our baseball games. It was my parents at church, in the pew or volunteering in some way or another. It was having kids who gave you grandkids. Work merely provided more people to whom to show pictures of the grandkids.

This generation of workers, on the early side of the baby boom, is marching off to retirement now. There are things to do in those sunset years. But the hours will surely stretch out and become hard to fill. As I sit with my friend it dawns on us that retirement sounds awful. Why would we stop working?

Here is the alternative to the treadmill thesis. As professional life has evolved over the past generation, it has become much more pleasant. Software and information technology have eliminated much of the drudgery of the workplace. The duller sorts of labour have gone, performed by people in offshore service-centres or by machines. Offices in the rich world’s capitals are packed not with drones filing paperwork or adding up numbers but with clever people working collaboratively.

The pleasure lies partly in flow, in the process of losing oneself in a puzzle with a solution on which other people depend. The sense of purposeful immersion and exertion is the more appealing given the hands-on nature of the work: top professionals are the master craftsmen of the age, shaping high-quality, bespoke products from beginning to end. We design, fashion, smooth and improve, filing the rough edges and polishing the words, the numbers, the code or whatever is our chosen material. At the end of the day we can sit back and admire our work – the completed article, the sealed deal, the functioning app – in the way that artisans once did, and those earning a middling wage in the sprawling service-sector no longer do.

The fact that our jobs now follow us around is not necessarily a bad thing, either. Workers in cognitively demanding fields, thinking their way through tricky challenges, have always done so at odd hours. Academics in the midst of important research, or admen cooking up a new creative campaign, have always turned over the big questions in their heads while showering in the morning or gardening on a weekend afternoon. If more people find their brains constantly and profitably engaged, so much the better.

Smartphones do not just enable work to follow us around; they also make life easier. Tasks that might otherwise require you to stay late in the office can be taken home. Parents can enjoy dinner and bedtime with the children before turning back to the job at hand. Technology is also lowering the cost of the support staff that make long hours possible. No need to employ a full-time personal assistant to run the errands these days: there are apps to take care of the shopping, the laundry and the dinner, walk the dog, fix the car and mend the hole in the roof. All of these allow us to focus ever more of our time and energy on doing what our jobs require of us.

There are downsides to this life. It does not allow us much time with newborn children or family members who are ill; or to develop hobbies, side-interests or the pleasures of particular, leisurely rituals – or anything, indeed, that is not intimately connected with professional success. But the inadmissible truth is that the eclipsing of life’s other complications is part of the reward.

It is a cognitive and emotional relief to immerse oneself in something all-consuming while other difficulties float by. The complexities of intellectual puzzles are nothing to those of emotional ones. Work is a wonderful refuge.

This life is a package deal. Cities are expensive. Less prestigious work that demands less commitment from those who do it pays less – often much less. For those without independent wealth, dialling back professional ambition and effort means moving away, to smaller and cheaper places.

But stepping off the treadmill does not just mean accepting a different vision of one’s prospects with a different salary trajectory. It means upending one’s life entirely: changing locations, tumbling out of the community, losing one’s identity. That is a difficult thing to survive. One must have an extremely strong, secure sense of self to negotiate it.

I’ve watched people try. In 2009 good friends of ours packed their things and moved away from Washington, DC, where we lived at the time, to the small college town of Charlottesville, Virginia. It was an idyllic little place, nestled in the Appalachian foothills, surrounded by horse farms and vineyards, with cheap, charming homes. He persuaded his employer to let him telework; she left her high-pressure job as vice-president at a big web firm near Washington to take a position at a local company.

My wife and I were intrigued by the thought of doing the same. She could teach there, we reckoned, and I could write. It was a reasonable train ride from Washington, if I needed to meet editors. We would be able to enjoy the fresh air, and the peace and quiet. Perhaps at some point we would open our own shop on the main street or try our hand at winemaking, if we could save a little money.

IT WASN’T THE STRESS OF BEING ON THE FAST TRACK THAT CAUSED MY CHEST TO TIGHTEN AND MY HEART RATE TO RISE, BUT THE THOUGHT OF BEING LEFT BEHIND BY THOSE STILL ON IT

Yet the more seriously we thought about it, the less I liked the idea. I want hours of quiet to write in, not days and weeks. I would miss, desperately, being in an office and arguing about ideas. More than that, I could anticipate with perfect clarity how the rhythm of life would slow as we left the city, how the external pressure to keep moving would diminish. I didn’t want more time to myself; I wanted to feel pushed to be better and achieve more. It wasn’t the stress of being on the fast track that caused my chest to tighten and my heart rate to rise, but the thought of being left behind by those still on it.

Less than a year after moving away, our friends moved back. They had found themselves bored and lonely. We were glad, and relieved as well: their return justified our decision to stay in the city.

One reason the treadmill is so hard to walk away from is that life off it is not what it once was. When I was a child, our neighbourhood was rich with social interaction. My father played on the church softball team until his back got too bad. My mother helped with charity food-and-toy drives. They both taught classes and chaperoned youth choir trips. They socialised with neighbours who did these things too.

Those elements of life persist, of course, but they are somewhat diminished, as Robert Putnam, a social scientist, observed in 1995 in “Bowling Alone: America’s Declining Social Capital”. He described the shrivelling of civic institutions, which he blamed on many of the forces that coincided with, and contributed to, our changing relationship to work: the entry of women into the workforce; the rise of professional ghettoes; longer working hours.

One of the civic groups that Putnam cites as an important contributor to social capital in ages past was the labour union. In the post-war era, unions thrived because of healthy demand for blue-collar workers who shared a strong sense of class identity. That allowed the unions’ members to capture an outsize share of the gains from economic growth, while also providing workers and their families with a strong sense of community – indeed, of solidarity.

The labour movement has unravelled in recent decades, and with it the network that supported its members; but these days a similar virtuous circle supports the professional classes instead. Our social networks are made up not just of neighbours and friends, but also of clients and colleagues. This interlaced world of work and social life enriches us, exposing us to people who do fascinating things, keeping us informed of professional gossip and providing those who have good ideas with the connections to help turn them into reality. It also traps us. The suspicion that one might be missing out on a useful opportunity or idea helps prod us off the sofa when an evening with “True Detective” beckons seductively.

This mixing of the social and professional is not new. It is not unlike Hollywood, where friends have always become collaborators, actors marry directors, and an evening out on the town has always been a public act that shapes the brand value of the star. Or like Washington, DC, in which public officials, journalists and policy experts swap jobs every few years and go to the same parties at night: befriending and sleeping with each other, exchanging ideas, living a life in which all behaviour is professional to some extent. But as hours have lengthened and work has become more engaging, this social pattern has swallowed other worlds.

There is a psychic value to the intertwining of life and work as well as an economic one. The society of people like us reinforces our belief in what we do. Working effectively at a good job builds up our identity and esteem in the eyes of others. We cheer each other on, we share in (and quietly regret) the successes of our friends, we lose touch with people beyond our network. Spending our leisure time with other professional strivers buttresses the notion that hard work is part of the good life and that the sacrifices it entails are those that a decent person makes. This is what a class with a strong sense of identity does: it effortlessly recasts the group’s distinguishing vices as virtues.

Life within this professional community has its impositions. It makes failure or error a more difficult, humiliating experience. Social life ceases to be a refuge from the indignities of work. The sincerity of relationships becomes questionable when people are friends of convenience. A friend – a real one – muses to me that those who become immersed in lives like this suffer from Stockholm Syndrome: they befriend their clients because they spend too much time with them to know there are other, better options available. The fact that I find it hard to pass judgment on this statement suggests that I, too, may be a victim.

My parents have not quite managed to retire, but they are getting there. Even with one foot in and one foot out of retirement, their post-career itinerary is becoming clear. They mean to see parts of the world they couldn’t when they were young and had no money, or when they were older and had no time. Their travels occasionally bring them to London to see me and my family. On a recent visit the talk shifted, as it often does, to when I might be planning to return to the east coast of America, much closer to the Carolinas, which is where they and most of the rest of my extended family still live. As my father walks around the house, my three-year-old son trotting adoringly behind him, they ask whether I couldn’t do my job as easily closer to home.

I get hung up on as easily. The writing I could do as easily, just about. Building my career, away from our London headquarters, would not be so easy. As I explain this, a circularity threatens to overtake my point: to build my career is to make myself indispensable, demonstrating indispensability means burying myself in the work, and the upshot of successfully demonstrating my indispensability is the need to continue working tirelessly. Not only can I not do all that elsewhere; outside London, the obvious brilliance of a commitment to this course of action is underappreciated. It looks pointless – daft, even.

And I begin to understand the nature of the trouble I’m having communicating to my parents precisely why what I’m doing appeals to me. They are asking about a job. I am thinking about identity, community, purpose – the things that provide meaning and motivation. I am talking about my life.

ndian Political Action Committee (I-Pac), an advocacy group run by political strategist Prashant Kishor, is doing more than just advising political parties on their campaigns for upcoming elections. At a time when there is a lot of curiosity surrounding Kishor's future plans, his advocacy group has launched an online platform to hunt for a leader for the 2019 Lok Sabha election.

The platform, called the National Agenda Forum, is a part-recruiting tool where people can also register to help the leader win next year's general election.

Who will this leader be? Well, that is for you to decide. People can log on to the National Agenda Forum (NAF), and vote on the issues they believe India must address on priority as well as nominate a leader they believe can address those issues.

The first part of the voting process will see people vote on a '10-point agenda' for the country. Next, people can pick a leader to execute this agenda.

"Anybody can be nominated by the voter to be a leader," I-Pac's media team told IndiaToday.in in a written reply when queried about who the leader potentially could be.

Once the voting is over on August 14 (results will be declared on August 15), I-Pac plans to approach the leader who wins the popularity poll on the NAF website. I-Pac says it will also approach the chosen leader's political party in an attempt to get the NAF's wining 10-point agenda included on the party's official 2019 election manifesto.

VOTING OPEN

The voting on the NAF website is open and will continue till August 14. Results will be announced on August 15 but I-Pac says that it hasn't yet taken a call on whether the voting will be audited by a third party.

The website offers a stock list of 18 agenda points for voters. These points have been inspired from Mahatma Gandhi's 18-point Constructive Programme, a collection of pre-Independence directives aimed at solving issues Gandhi believed India must address, I-Pac says.

Those who come to vote also have the option of submitting agenda points they believe are missing on the website's stock list.

The second step involves nominating/voting for a "leader". The winner of the leader poll, I-Pac says, will be approached to represent the winning 10-point agenda.

Voting page for picking the leader (Photo: Screengrab)

Current choices in the leader poll range from Narendra Modi and Rahul Gandhi to Akhilesh Yadav and Naveen Patnaik. Mamata Banerjee and Mayawati are also among the choices that figure on the poll.

The choices are not limited. Those taking the poll can also nominate the name of leaders not already present on the list.

The final stage of the voting process sees NAF essentially become a recruiting platform. People can choose to register as part-time associates with I-Pac and "help the chosen Leader to get elected in the upcoming General Elections".

One of the major aims of demonetisation was the destruction of black money. The idea was that those who have black money will not deposit it into the banks, for the fear of getting caught, and in this way black money would be destroyed.

Quiet Easily Done (QED), as they say.

On November 10, 2016, the finance minister Arun Jaitley explained the logic in an interview, where he said: "Obviously people who have used cash for crime purposes are not foolhardy enough to try and risk and bring the cash back into the system because there will be questions asked."

Or as the then attorney general Mukul Rohatgi put it: "There is roughly Rs 17 lakh crore rupees in circulation. Our estimate is that approximately Rs 11 to Rs 12 lakh crore will come back into the banking system through this scheme. Again, our assessment is that Rs 3 to Rs 4 lakh crore which doesn't return is prima facie is the black component of the currency in circulation."

What happened was exactly the opposite of what Jaitley, Rohatgi and many others who came out in support of demonetisation, were expecting. Around 99.3% of the demonetised currency was deposited into the banks.

This failure to destroy black money called for a change of the real aim of demonetisation and which is precisely what is happening.

Now the story going around on WhatsApp forwards and being put forward by the blind supporters of the Modi government, is exactly the opposite of the hope of the black money being destroyed.

The black money was deposited into the banks and that works for the good of the country, we are now being told.

As per this story, all the black money which was uselessly lying in the vaults and homes of people, and under their mattresses as well, is now a part of the Indian financial system, and hence, is being put to some good use. Earlier it wasn't.

While, on the face of it, this sounds like an explanation, the data doesn't really bear it out.

Let's try and understand this step by step.

1) The Reserve Bank of India recently released its annual report for 2017-2018. Among other things, this report has also declared the household financial savings. Household financial savings also include savings held in the form of currency and deposits. Let's take a look at Figure 1, which plots this out.

Figure 1:

GNDI in Figure 1 stands for Gross National Disposable Income. It defined as the gross domestic product (GDP) plus all transfers in cash and kind received from foreigners minus all transfers in cash and kind to be paid to foreigners.

Let's take a careful look at Figure 1. The deposits as a percentage of GNDI in 2016-2017 jumped to 6.3% of GNDI. They were at 4.6% of GNDI in 2015-2016.

This was primarily because of all the demonetised money that was deposited into banks. In 2017-2018, the deposits fell to 2.9% of the GNDI, from 6.3% a year earlier. Meanwhile, household financial savings held in the form of currency zoomed to a seven year high of 2.8% of the GNDI. It was at 1.4% of GNDI in 2015-2016.

What has happened here? In euphemistic terms people are building their cash positions again. Hence, a large portion of the deposits have been withdrawn and are now held as cash or currency.

This basically means that a significant portion of the black money which had been deposited into the banks at the time of demonetisation, has been withdrawn. It is back in the vaults of people in the form of cash, and under their mattresses as well. Black money is back to being black. It is no longer a part of the financial system, as we are being told.

2) Let's look at some more data.

As per the White Paper on black money released in May 2012, around 4.9% of the black money (or wealth to be more precise) found during search and seizure operations carried out by the income tax department, was held in the form of cash. This works as a good proxy for the total amount of black money which is held in the form of cash or currency. (Black money is not held just in the form of cash. It is held in other forms from gold to insurance policies to real estate).

Over and above this, the ministry of finance press release which accompanied the demonetisation decision of the Modi government, stated: "The World Bank in July, 2010 estimated the size of the shadow economy for India at 20.7% of the GDP in 1999 and rising to 23.2% in 2007."

Let's work with this figure, like the government did. Black money in India was at around 23.2% of the country's GDP. The black money held in the form of currency was around 4.9% of this. This basically meant that black money held in the form of cash amounted to around 1.4% of the GDP (4.9% of 23.2%).

The GDP of 2015-2016 was Rs 13,764,037 crore. 1.4% of this works out to around Rs 1,92,697 crore. The GDP of 2016-2017 was Rs 15,253,714 crore. 1.4% of this works out to around Rs 2,13,552 crore. Given that demonetisation happened in November 2016, which was a little over the middle of the year, we can take the average of the two numbers to come out with an estimate of black money held in the form of cash.

The average works out to around Rs 2,03,124 crore. Given that around 99.3% of demonetised money came back. We can assume that 99.3% of the black money held in the form of cash or currency was also deposited back into the banks. This works out to around Rs 2,01,702 crore, which we can round off to Rs 2,00,000 crore.

3) The savings in the form of currency in 2017-2018 were at 2.8% of the GNDI or Rs 4,75,544 crore. In 2015-2016, they had stood at 1.4% of the GNDI or Rs 1,96,243 crore. The difference works out to Rs 2,79,301 crore. Hence, the savings held in the form of currency or cash have gone up by Rs 2,79,301 crore. This is much more than Rs 2,00,000 crore, or the total amount of black money held in the form of cash or currency and deposited back into banks at the time of demonetisation.

What does this tell us? It tells us that the black money held in the form of cash which had been deposited into banks and was supposedly being put to good use, has been withdrawn, and is now all back to where it originally belonged-under the mattresses of people.

Hence, the point about the black money is being put to some good use, is basically rubbish. This also means that people who are still in the business of defending demonetisation, now need to need to think of newer advantages to WhatsApp.

Anglo American’s De Beers, the world’s No.1 diamond miner by value, has just had the lowest sales for its seventh cycle since it began releasing data in 2016, as it let customers delay acquiring smaller stones for the first time.

Sales for the cycle stood at a provisional $505 million, down 5.5 percent from the $533 million obtained in the previous cycle of the year and 0.4 percent from $507 million for same period in 2017.

“De Beers Group provided Sightholders with the opportunity to re-phase the allocation of some smaller, lower value rough diamonds.” chief executive officer, Bruce Cleaver, acknowledged in the statement.

The unusual move (De Beers is known for requiring buyers to take what’s offered) says lots about the state of the low-end diamond market. The last time the company did something similar, in fact, was two years ago, when India’s move to ban high-value currency notes pushed down demand.

Sales were down $134 million, or 21 percent compared to the same cycle in 2016, when De Beers began releasing this kind of data.

The diamond giant has about 80 handpicked clients called ightholders who are allocated parcels of diamonds sorted and aggregated in Gaborone. The 10 annual sales events are known as sights.

De Beers’ new strategy for small stones, paired with its looming entry into the lab-grown stones market, have many in the industry worrying about prices.

Cheaper diamonds, which are often small and low quality, are selling for a lot less now than five years ago. And when it comes to synthetic stones, De Beers’ entry in the market will create a big price gap between mined and lab diamonds, pressuring rivals that specialize in synthesized stones at the same time.

A 1-carat man-made diamond sells for about $4,000 and a similar natural diamond fetches roughly $8,000. De Beers new lab diamonds will sell for about $800 a carat. That’s a fifth of the price of existing man-made stones and one-tenth of the cost of buying a similar natural gem.

No wonder competitors are worried. The lab-grown industry has filed a complaint with the U.S. Federal Trade Commission, accusing De Beers of price dumping and predatory pricing.

Low sales, stable demand

In 2016, De Beers recorded sales of $639 million for the seventh of its tenth annual sales events. That is $134 million or 21 percent more than what it just made after letting buyers reject small, low-quality stones. That means that, to date, 2018 is shaping to be the worst in terms of sales for the Beers in the past two years, with combined sales of $3.93 billion against the previous year’s $4 billion and 2016’s sales of $4.12 billion.

It is not a good time to be producing power round the clock.

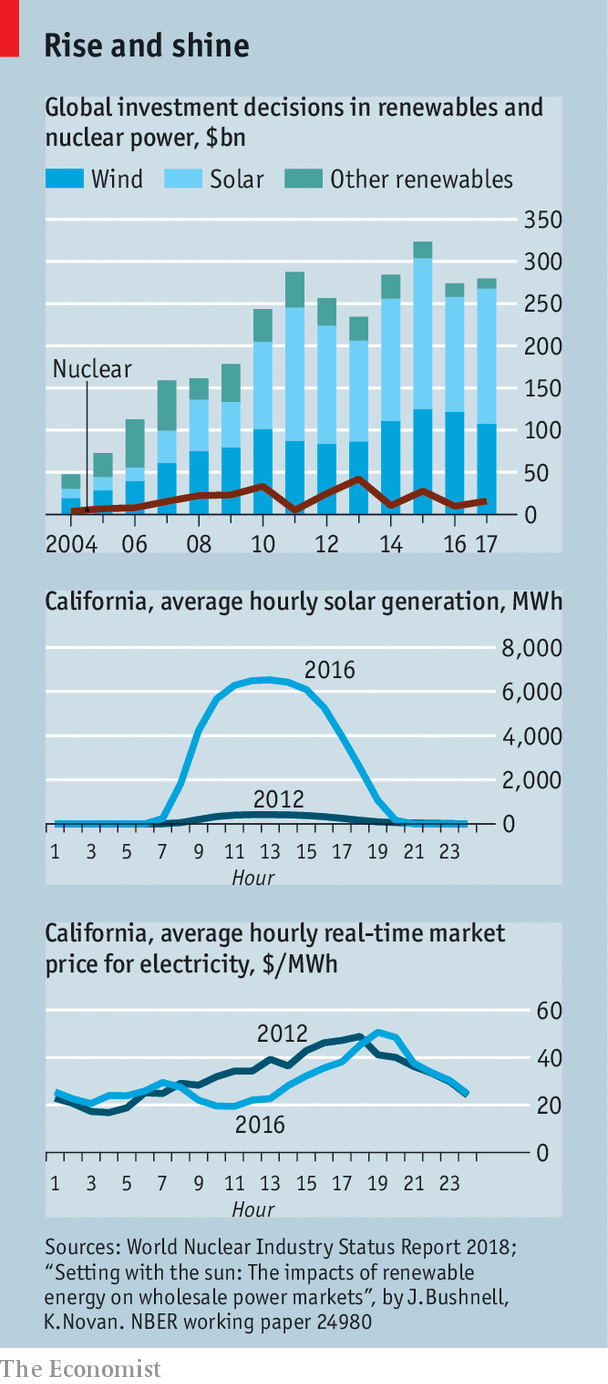

SOME call it a zero-carbon schism, others a heresy. The researchers, policymakers and environmentalists united over the need to stop global warming are divided on how to go about it. Many believe that renewable energy, especially wind and solar, has by far the biggest role to play. A dogged few, however, cling to nuclear energy, which is also carbon-free but has an image problem. The two camps barely speak to each other.

That is why three little words, “zero-carbon resources”, in a bill that landed on the desk of California’s governor, Jerry Brown, on August 29th are so important. Not only would the legislation commit the state to generating 60% of its electricity from renewables by 2030, up from a previous mandate of 50%. It also calls for generating 100% by 2045 from renewable and “zero-carbon resources”, which could include nuclear power. Of course, by then other emission-free energy technologies, such as batteries, hydrogen, and the capture and sequestration of carbon dioxide from fossil-fuel plants, could be better and cheaper than splitting nuclei. But atomic energy would stand a chance if it is still around. And in green matters, where California goes others often follow.

In 2017 almost 30% of the state’s electricity came from renewable sources, with solar and wind accounting for about 10% each. Nuclear was about 9%. A decade ago, solar was just 0.22%, and wind 2.25%, with nuclear at 15%. Nuclear’s relative decline reflects, in part, a global trend highlighted in the World Nuclear Industry Status Report (WNISR), issued on September 4th. During the past decade investment in renewables has surged, whereas in nuclear it has stagnated (see chart, top panel). Falling prices of solar panels and wind turbines, the ever-growing expense and difficulty of building nuclear facilities, and cheap natural gas all play a part.

A working paper published last month by James Bushnell and Kevin Novan of the University of California, Davis, underscores the challenge that renewables pose for nuclear and other sources of baseload power, such as coal. It shows that average output at noon from big solar farms in California increased tenfold between 2012 and 2016. That has had a big impact on wholesale power prices. The average real-time price around midday has dropped sharply, whereas after sundown average prices have increased. The more solar capacity is installed, the authors find, the worse for baseload generators—that is, those that produce electricity around the clock. The new energy mix rewards gas turbines that can be turned on for a few hours to satisfy peak demand in the evening.

But because additional solar capacity will produce power at times when there is already a glut, returns to further investment in solar capacity will decline. This points to a big flaw in state mandates, such as California’s, which assume that investment will pour into renewables even if market prices are low. The authors favour a price on carbon instead (California already has a “cap and trade” scheme), which would help spur investment in clean-energy provision at times when the sun is not shining.A working paper published last month by James Bushnell and Kevin Novan of the University of California, Davis, underscores the challenge that renewables pose for nuclear and other sources of baseload power, such as coal. It shows that average output at noon from big solar farms in California increased tenfold between 2012 and 2016. That has had a big impact on wholesale power prices. The average real-time price around midday has dropped sharply, whereas after sundown average prices have increased. The more solar capacity is installed, the authors find, the worse for baseload generators—that is, those that produce electricity around the clock. The new energy mix rewards gas turbines that can be turned on for a few hours to satisfy peak demand in the evening.

About 150 gigawatts of wind and solar were installed globally in 2017 versus 3GW of nuclear. Yet even though so much favours renewables, atomic energy is not dead. Nuclear power still provides more than twice as much electricity globally as wind, and 5.5 times as much as solar, partly because it runs all the time rather than intermittently. In June President Donald Trump instructed his energy secretary, Rick Perry, to take emergency steps to keep nuclear and coal plants running, citing national-security considerations. In April New Jersey launched a scheme to reward nuclear-power plants for producing emissions-free power, as part of the state’s goal for 100% clean energy by 2050.

China will be central to nuclear power’s future. It accounted for three of the four new nuclear plants to connect to the grid last year globally, has the most reactors under construction, and in June introduced two new classes of design. But it also leads the world in renewables. Russia’s Rosatom, a state-owned nuclear-power firm, is selling its technology abroad vigorously.

The WNISR, whose authors consider themselves industry critics, draws attention to another potential reason why nuclear power is resilient: its usefulness for nuclear-weapons programmes. The processes which produce fuel for civilian plants can also be used to produce crucial fissile material for weapons, and the training, research and industrial capabilities that come with an indigenous civilian nuclear programme can be very helpful for other purposes, such as nuclear submarines programmes. It says that only in the past few years are insiders starting to acknowledge, in countries like America, that it is hard to sustain a nuclear-weapons capability without a parallel civilian nuclear programme. That may help explain the commitment to keep alive plans to build nuclear plants among big military powers in the West and Asia, even though a mixture of renewables and natural gas could be far cheaper. Such suspicions merely widen the rift between the two carbon-free camps.