So unless something dramatic happens with the Chinese economy, if they comply with the US trade deal, they will be buying $100bn more from the US and less from someone else each year for the next two years.

As I discussed here, the developments so far in the trade war have backfired on the US. China's trade surplus is up $85bn in 10 months or $102bn annually for 2019. Europe has been the dumping ground for $60bn annualised in manufactured goods that would have gone to the US. The reduction from 15% to 7.5% on $120bn in goods might alleviate that a little, but only a little.

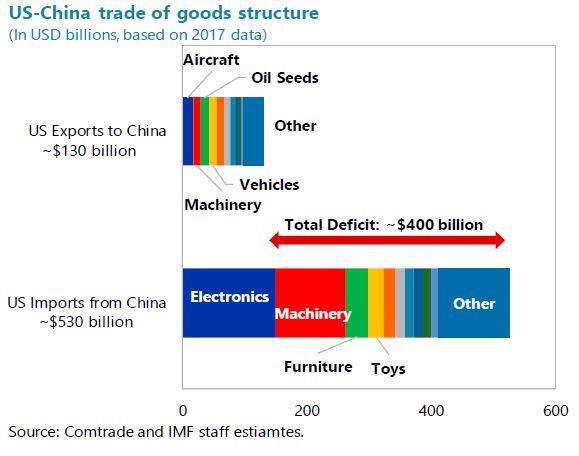

Per the deal, the Chinese will buy $100bn a year more in goods and services. China bought $130 billion in U.S. goods in 2017, before the trade war began and $56 billion in services. That's a 54% step change, which is not happening organically as a function of 6% Chinese economic growth.

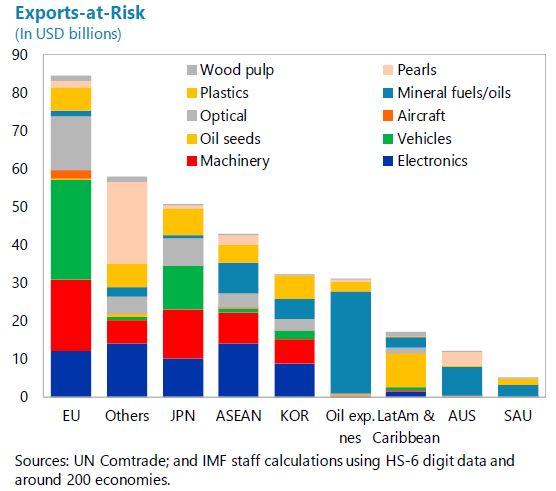

As such, the Chinese government will have to pull levers and third countries have to lose export orders. In terms of manufactured goods the only games in town are the EU, Japan and Korea. The IMF in their recent Article 4 paper on China estimated that about half of the import displacement would be born by Europe.

In the chart below, the IMF had assumed a $200bn/ year deal to halve the US trade deficit with half of that falling on the Eurozone.

Based on a $100bn a year deal the EU would lose about $42bn a year in goods exports. Korea and Singapore could potentially lose exports amounting to about 1% and 1.9% percent of their GDP.

Looking at the phase 1 deal numbers, China has committed to increase purchases of U.S. agriculture products by $32 billion over two years. That would average an annual total of about $40 billion, compared to a baseline of $24 billion in 2017 before the trade war started.

So if we deduct $16bn in Ag purchases from the $100bn, that leaves $84bn in goods and services. Its easier for the Chinese government to encourage goods substitution over services, so let's assume it's 75% goods 25% services, vs a 70%/ 30% balance between manufacturing and services in their existing US imports.

$84bn in imports x 75%, x Europe's 50% share totals $31.5bn in potentially lost Eurozone manufacturing exports.

So Eurozone goods manufactures face the combination of $31.5bn of high end manufacturing export losses and $60bn in lower to mid-end manufacturing product dumping, or potentially even higher.

That's a total of $91.5bn in final demand loss. Eurozone manufacturing is 16.6% of the Eurozone's $13.7Tn economy. That is $2.27Tn. So a final demand shock loss of $91.5bn is 4% of manufacturing output. Plus some additional losses in agricultural exports.

The Japanese and Korean exporters who will shoulder most of the balance of the export loss will also be looking to sell products into Europe.

That is catastrophic at a time of existing contraction. It will also be felt unevenly. I don't see many Chinese cars being bought in Europe or European companies losing car exports. But clothes and consumer goods will be dumped by China and Eurozone industrial equipment producers will lose export orders.

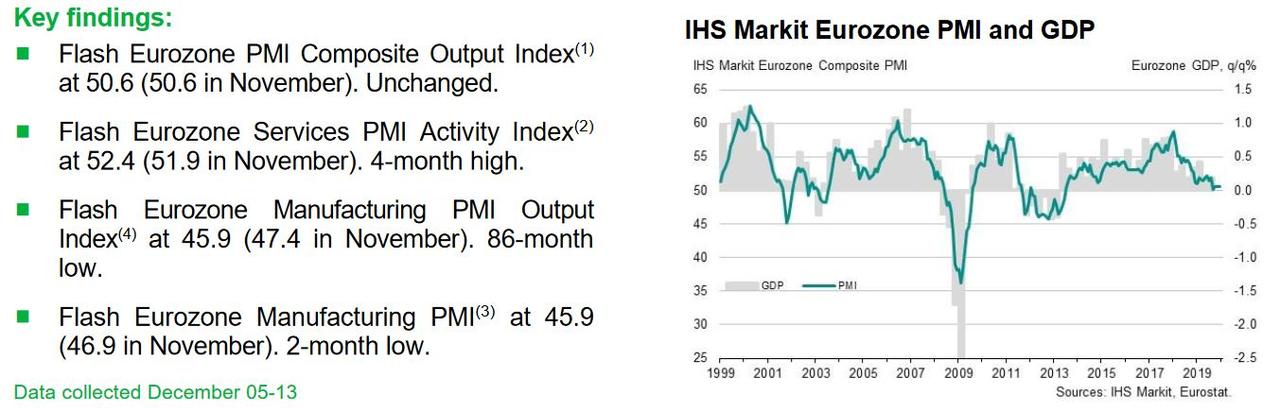

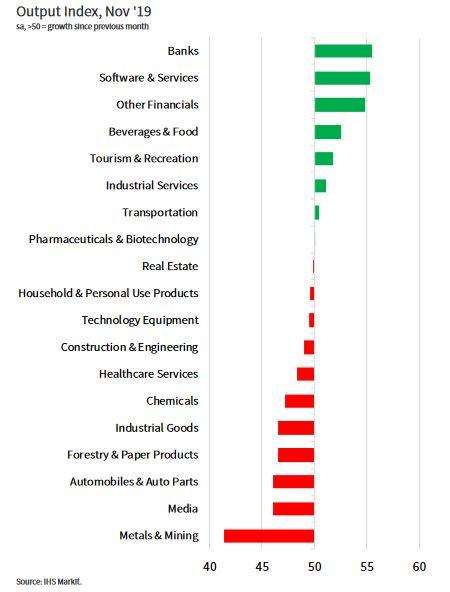

Needless to say the Eurozone manufacturing and industrial sectors have already been contracting for some time with November PMIs confirming continued weakness:

Source: MarkIt

I had predicted a year ago that Europe could be facing a perfect storm driven be a hard Brexit, product dumping as a result of the trades wars, central bank tightening and weak final demand. While demand is still weak and manufacturing has contracted, hard Brexit was avoided and monetary tightening has turned to stimulus. After the December 2018 risk off, risk has rallied this year, looking at the Dax YTD you would think Europe was booming, not kabooming!

But we still haven't seen what the impact of a FTA-based Brexit is. The UK is already one of the most popular FDI destinations in Europe and that could increase as a result of Brexit and the potential for an investment led industrial boom.

The US could also ultimately apply tariffs in its trade dispute with Europe and Europe with no real WTO recourse would have to follow suit.

So it looks like a new down leg is nearly on us for the Eurozone and Lagarde needs a crisis to get traction for a green new deal and fiscal reflation/ MMT policies.

China may also not comply with this deal, given the unrealistic size and time frames involved and by mid-2020 the outcome might look like 'go-slow' from the US perspective.

That would leave Trump, mid-election campaign, accused of either failing in his objectives or being forced to put tariffs back on. We know his typical response function to not getting his way

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.