The process of withdrawing monetary stimulus is fraught with danger

AS WITH London buses, don’t worry if you miss a financial crisis; another will be along shortly. The latest study on long-term asset returns from Deutsche Bank shows that crises in developed markets have become much more common in recent decades. That does not bode well.

Deutsche defines a crisis as a period when a country suffers one of the following: a 15% annual decline in equities; a 10% fall in its currency or its government bonds; a default on its national debt; or a period of double-digit inflation. During the 19th century, only occasionally did more than half of countries for which there are data suffer such a shock in a single year. But since the 1980s, in numerous years more than half of them have been in a financial crisis of some kind.

The main reason for this, argues Deutsche, is the monetary system. Under the gold standard and its successor, the Bretton Woods system of fixed exchange rates, the amount of credit creation was limited. A country that expanded its money supply too quickly would suffer a trade deficit and pressure on its currency’s exchange rate; the government would react by slamming on the monetary brakes. The result was that it was harder for financial bubbles to inflate.

But since the early 1970s more countries have moved to a floating exchange-rate system. This gives governments the flexibility to deal with an economic crisis, and means they do not have to subordinate other policy goals to maintaining a currency peg. It has also created a trend towards greater trade imbalances, which no longer constrain policymakers—the currency is often allowed to take the strain.

Similarly, government debt has risen steadily as a proportion of GDP since the mid-1970s. There has been little pressure from the markets to balance the budget; Japan has had a deficit every year since 1966, and France since 1993. Italy has managed just one year of surplus since 1950. In the developed world, consumers and companies have also taken on more debt.

The result has been a cycle of credit expansion and collapse. Debt is used to finance the purchase of assets, and the greater availability of credit pushes asset prices higher. From time to time, however, lenders lose faith in borrowers’ ability to repay and stop lending; a fire sale of assets can follow, further weakening the belief in the creditworthiness of borrowers.

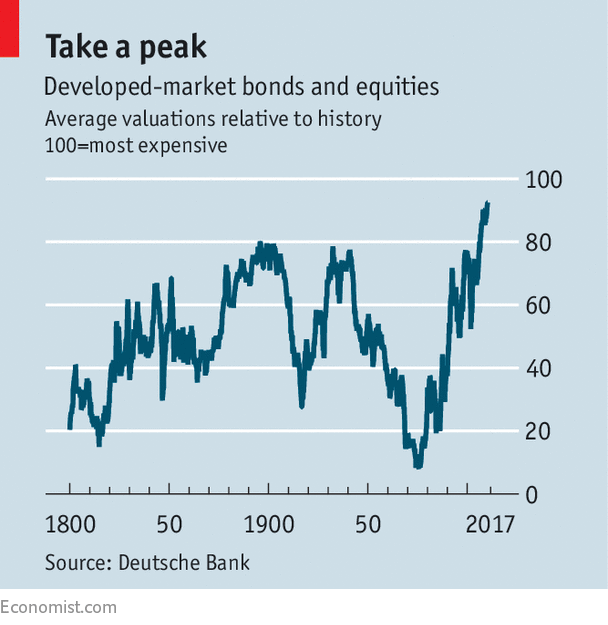

Central banks then step in to cut interest rates or (since 2008) to buy assets directly. This brings the crisis to a temporary halt but each cycle seems to result in higher debt levels and asset prices. The chart shows that the combined valuation of bonds and equities in the developed world is higher than ever before.

All this suggests that the financial system could be due another crisis. Deutsche makes several suggestions at to what might cause one, from a debt-related crash in China, through the rise of populist political parties to the problem of illiquidity in bond markets.

The most likely trigger for a sell-off is the withdrawal of support by central banks; after all, the monetary authorities are generally credited with having saved the global economy and markets in 2009. In America the Federal Reserve is pushing up interest rates and reducing the size of its balance-sheet; the European Central Bank seems likely to cut the scale of its asset purchases next year; the Bank of England might even increase rates for the first time in more than a decade.

Central banks are well aware of the dangers, of course; that is why interest rates are still so low, even though developed economies have been growing for several years. But the process of withdrawing stimulus is tricky. A big sell-off in the government-bond markets in 1994 started when the Fed tightened policy after a period when rates were kept low during the savings-and-loan crisis.

The high level of asset prices means that any kind of return to “normal” valuation levels would constitute a crisis, on Deutsche’s definition. That might mean that central banks are forced to change course and loosen policy again. But the process would take a little time; central banks will not want to appear too enslaved to the markets.

Many investors will want to ride out the volatility; that has been a winning strategy in the past. The problems will emerge among those investors who have borrowed money to buy assets—in America the volume of such debt exceeds the level reached in 2008. The big question is which is the most vulnerable asset class. American mortgage-backed securities were the killers in 2008; it is bound to be something different this time round.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.