Housing in the posher parts of global cities has become a distinct asset class

Centre Point, a tower that looms over central London, was empty for so long in the 1970s that it lent its name to a homelessness charity. Recently it was converted from offices to flats. Half are yet to find buyers. So the developer has taken them off the market pending a clearing of the political fog over Britain. Its boss complained to Estates Gazette, a trade paper, of bids that were “detached from reality”. One-bedroom flats were on sale for £1.8m ($2.4m).

Even flats with less hefty price tags have been hard to shift lately. Property prices in London are falling. Sellers are waiting for better prices. It is tempting to put all the blame on Brexit, but that would ignore the broader picture. House prices in big global cities increasingly move together. What happens in London has a growing influence on what happens in New York, Toronto and Sydney—and vice versa. And trouble is brewing in some of these other markets, too.

Property used to be thought of as an inflation hedge. But in recent years it has become a substitute for low-yielding Treasury bonds—a safe asset in which the globally mobile can store their wealth. After years of rapid price rises, houses in the most favoured markets are overvalued. Rising bond yields, tighter mortgage credit and shifting politics are now combining to push prices down.

The value of homes in the posher parts of global cities move in sync because they have become a distinct asset class. Private-equity firms and investment trusts, not just individuals, own them. Prices in such cities are explained more by global factors, such as the yields on the safest government bonds, than by local conditions. This global influence is particularly marked in financial centres that are open to capital flows, such as London, New York, Toronto and Sydney. It has extended into smaller European cities, such as Amsterdam.

Demand from emerging markets such as China and Russia has been growing. Buyers are willing to pay steeply to secure a safe place for their savings—or a bolthole for themselves. Cristian Badarinza of the National University of Singapore and Tarun Ramadorai of Imperial College London have shown that political trouble in Russia, parts of Africa and the Middle East predicts a rise in the price of prime London property. The same sort of influence is also found in less ritzy neighbourhoods, says Mr Ramadorai. For instance, property prices in Hounslow and Southall, which have lots of settlers from South Asia, picked up in the early 2000s, a period of political tensions in India.

Foreign demand has spillovers. If an oligarch buys a house, it drives up the prices of smaller properties nearby. A paper by Dragana Cvijanovic of the University of North Carolina and Christophe Spaenjers of hec Paris finds similar effects in Paris’s property market. Foreign buyers, mostly from China, have been a force behind booms in the big cities of Australia and Canada.

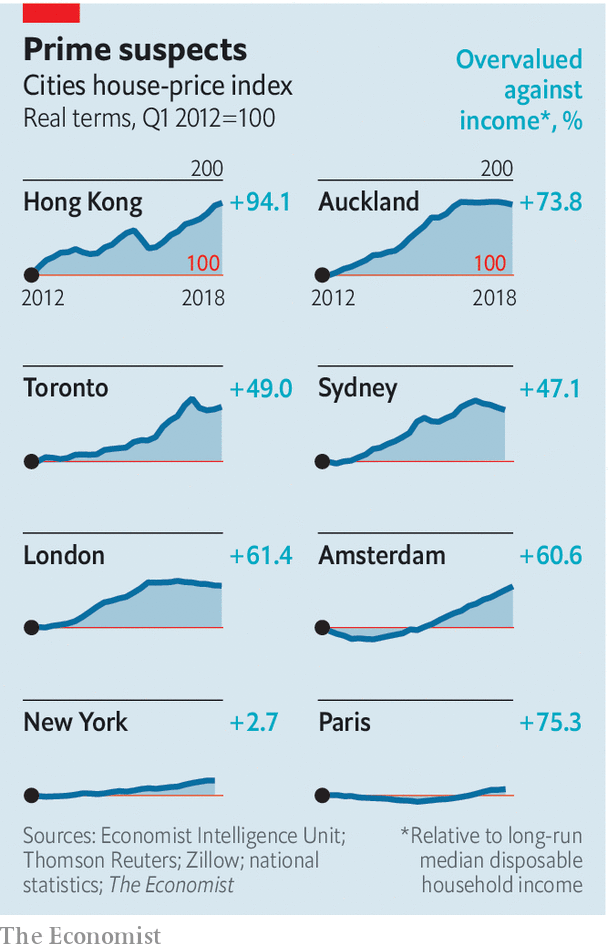

But the tide has changed. Global cities look awfully dear. The rental yield on investment homes worldwide fell below 5% for the first time ever in 2016, according to msci ipd, a financial-information firm. House prices relative to incomes are well above their long-run average in Amsterdam, Auckland, London, Paris, Sydney and Toronto (see chart).

And prices are falling in some of the dearer cities, in response to a variety of forces. The yield on Treasury bonds, the world’s benchmark safe asset, is rising. A tightening of credit standards on mortgages in Australia and Canada has squeezed housing in cities there. Uncertainty about Brexit has made London a place of political risk rather than a refuge from it. Meanwhile, capital is moving less freely. Governments are charier of Russian money. China is shaking down its super-rich for taxes and is zealous in its policing of capital outflows.

A corollary of stronger links between global cities is a kind of “waterbed” effect. For instance, when taxes were levied on foreign homebuyers in Vancouver in 2016, the market cooled, but Toronto took off. There are buyers who will compare prices in, say, Mayfair in London and Park Avenue, New York. They look for value. But it is vanishingly scarce. The market is turning. Those who bought at the peak, or are hoping to sell, will slowly adjust to a new reality.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.