As rates rise, stress levels will, too

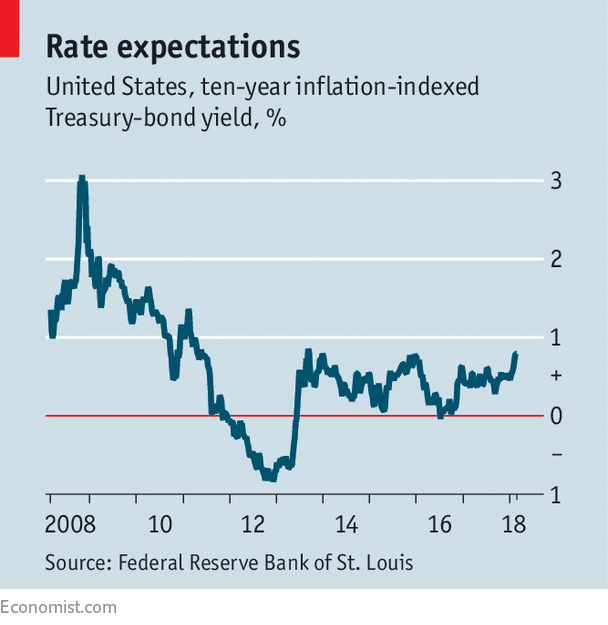

REAL interest rates in the developed world have been low ever since the financial crisis of 2008-09 (see chart). The global economy might have struggled to recover had that not been the case; higher rates would have caused many more companies and homeowners to default.

Central banks are now starting to push rates slightly higher. And according to a new paper* from Bain, a management consultancy, the trend towards robotics will push them higher still—at least for a decade. That could be a shock for the financial markets.

Bain estimates that by 2030 American companies will have invested as much as $8trn in automation. As companies scramble to borrow money in order to buy machinery and robots, the resulting investment boom will drive up rates.

Automation will boost productivity, which has grown sluggishly in recent years. This slowdown may have been caused by the shift from manufacturing to services, where productivity gains are harder to achieve. Between 1993 and 2014, the American car industry more than doubled its productivity, but lost 28% of its workforce. By contrast, over the same period hospitals added 28% more jobs and increased productivity by just 16%.

But automation is about to come to a wide range of service industries. Though that will be a boon for productivity, Bain estimates that 20-25% of current jobs could be eliminated by 2030. This shift will be much faster than previous labour-market transformations, such as that from agriculture to industry at the start of the 20th century. Lower-skilled workers, such as waiters, will take the biggest hit.

The result would be an even more unequal economy, because a greater share of income would go to highly paid workers. They are more likely to save and invest than lower-paid workers, who spend virtually all their income. So after the initial interest-rate surge, the increase in saving and the hit to demand could cause interest rates to plunge again, falling back to zero in real terms.

In a paper** written last year for the Bank for International Settlements, a central-bankers’ club, Charles Goodhart and Manoj Pradhan came up with similar predictions for interest rates using a different chain of reasoning. They thought demography would be the main reason interest rates would rise. Real rates adjust to balance the desired levels of savings and investment. The current low level of real rates indicates that the former has exceeded the latter as the baby boomers have made provision for their old age. But global population growth is slowing and the size of working-age cohorts in the advanced economies and China will decline.

As workers retire, they will run down their savings pots. Companies will substitute capital for labour as the workforce shrinks. A smaller pool of workers will earn higher wages, pushing up the labour share of GDP and (in a divergence from the Bain line of reasoning) thereby reducing inequality, but also driving up inflation. Keeping it under control will require higher nominal interest rates. Furthermore, desired savings will fall faster than desired investment, and real rates will rise.

What about the argument that “secular stagnation” will keep interest rates low? Andrew Smithers, an independent economist based in London, says that because there is no reason to expect world growth to be slower than average over the next decade, global interest rates could well rise to more normal levels. However, he adds, growth may be less important for rates than is the balance between fiscal and monetary policy. With fiscal policy easing in both America and Europe, monetary policy will need to be tightened, he reckons.

That would make the road to higher rates a bumpy one. The piles of debt accumulated before the financial crisis have been redistributed rather than eliminated. A sudden rise in rates might hurt economic activity, and thus be self-limiting, if central banks have to reverse policy. Financial markets have translated low rates into high valuations. Equities are priced as the discounted value of future profits; the lower the discount rate, the higher the price. But in the Goodhart/Pradhan scenario, shares might face a double whammy. As employers compete for scarce workers, the discount rate would rise and profits would be squeezed. Homeowners, and companies with lots of debt on their balance-sheets, would get a nasty shock. As rates rise, stress levels will, too.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.