One aim is to allay fears that a current pact will unravel

OIL bears beware. On February 20th Suhail al-Mazrouei, OPEC’s rotating president and energy minister of the United Arab Emirates, said the 14-member producers’ group is working on a plan for a formal alliance with ten other petrostates, including Russia, aimed at propping up oil prices for the foreseeable future. If it comes to anything, it could be OPEC’s most ambitious venture in decades.

The result will not be, he insists, a “supergroup”. The notion of Saudi Arabia and Russia joining forces as the Traveling Wilburys of the oil world may be a bit jarring. It remains an idea in “draft” form. But whatever its chances, it attempts to shift a belief widely held by participants in oil markets: that non-American oil producers are helpless against the shale revolution.

That belief has strengthened because of a renewed flood of American shale production in the latter part of 2017 after prices of West Texas Intermediate climbed above $50 a barrel. The International Energy Agency (IEA), the industry’s forecaster-in-chief, says America could overtake the two biggest producers, Russia and Saudi Arabia, this year. Such countries, it added, faced the “sobering thought” that America’s rise to the super league was reminiscent of the first wave of shale growth that ended with an oil-price crash in 2014.

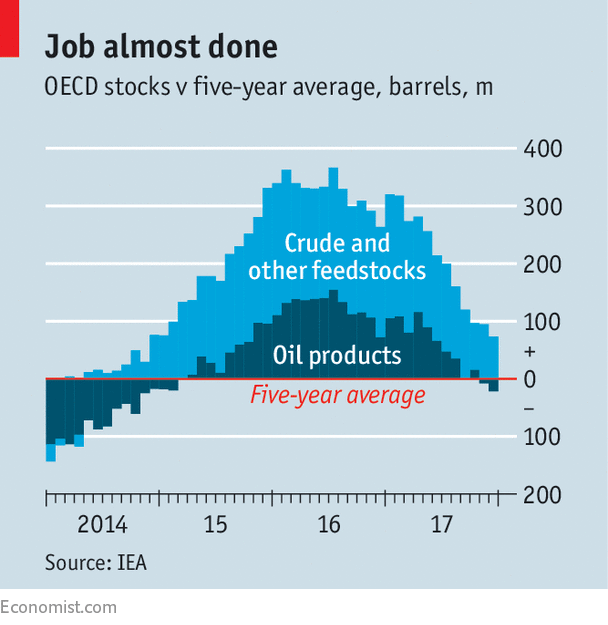

The shale resurgence comes at a delicate time for OPEC, Russia and the rest. It is largely their actions that have pushed up prices. In 14 months they have come close to their goal of curtailing oil production in order to return the oversupply of global crude to its more manageable five-year average (see chart). They still have about 74m barrels to go. As yet, Mr Mazrouei says, there is no “exit strategy” for when the agreement is reviewed in June.

A shift is under way in relations between Saudi Arabia and Russia, the two leaders of the OPEC/non-OPEC cabal. They appear to have set aside a mistrust, bordering on enmity, that was exacerbated by their support for opposing sides in the Syrian civil war. “The Russia-Saudi relationship is real. ‘Put a ring on it’, to quote Beyoncé,” says Helima Croft, an oil analyst at RBC Capital Markets. She says both countries need high prices to soothe tensions at home.Fareed Mohamedi, chief economist at Rapidan Energy Group, an American consultancy, likens their task to central bankers unwinding ultra-easy monetary policy. They risk spooking the markets if they send the wrong signal. So the proposal of a pact lasting into the foreseeable future is a way to reassure the market that the grown-ups will continue to regulate supply. “They’re saying, ‘Daddy is back’.”

Since King Salman of Saudi Arabia visited Moscow for the first time in October, the two countries’ oil ministers have frequently popped over to each other’s capitals. Mr Mohamedi says Muhammad bin Salman, the Saudi crown prince, needs oil at $70-80 a barrel to keep the economy steady as he enacts reforms, in particular the partial privatisation of Saudi Aramco, the state oil company. He believes Russia can help with that. Vladimir Putin, Russia’s president, who faces elections in March, sees eye-to-eye with Prince Muhammad.

Furthermore, the two countries are discussing unprecedented investments in each other’s oil industries. A Russian sovereign wealth fund is considering buying shares in the Aramco listing. Aramco is mulling a stake in a vast liquefied-natural-gas project in the Russian Arctic.

The possibility of long-term co-operation between the two countries to support oil prices also has a defensive logic. Not only is rising American oil production a threat, but in the coming decades demand for oil is expected to wane as it is replaced by cleaner sources of energy. This could cause a race to the bottom as big producers try to sell their oil before it becomes worthless. Restraining production is a way to postpone such feral competition, at least until Russia and Saudi Arabia can wean their economies off oil.

But the perils of such a strategy may outweigh its benefits. If it works, and prices rise sharply above $70 a barrel, it will flush out yet more production in America and other big producing countries such as Brazil, as happened before 2014. That would reinforce what the IEA calls the risk of history repeating itself. So OPEC and non-OPEC producers would need strategies to keep prices from rising too high as well as falling too low. Bassam Fattouh of the Oxford Institute for Energy Studies, a think-tank, says that might require joint investment approaches, which are “extremely difficult, if not impossible”.

If prices tumble, countries would need to cut production further. In OPEC’s history Saudi Arabia has reluctantly played the role of swing producer, regulating its output to keep the market in balance. A successful long-term arrangement would need Russia and OPEC members to share more of the burden, which they have mostly been loth to do.

A further concern is Saudi Arabia’s OPEC strategy once Aramco sells shares to investors. Mohamed Ramady, the author of a new e-book, “Saudi Aramco 2030”, says that relations between partially privatised oil companies and their governments become strained when the interests of governments clash with those of shareholders. “Privatising Aramco could then become a double-edged sword for the kingdom,” he writes.

At present, Saudi Arabia’s rulers appear to believe that the risks are worth taking. They may have more to fear from a restive population at home than shale producers abroad. But they underestimate the risk of shale, and overestimate their own ability to manage the market, at their peril.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.