A commonly watched indicator of financial stability may produce too many false alarms.

ON THE morning of December 7th 1941, George Elliott Junior noticed “the largest blip” he had ever seen on a radar near America’s naval base at Pearl Harbour. His discovery was dismissed by his superiors, who were thus unprepared for the Japanese bombers that arrived shortly after. The mistake prompted urgent research into “receiver operating characteristics”, the ability of radar operators to distinguish between true and false alarms.

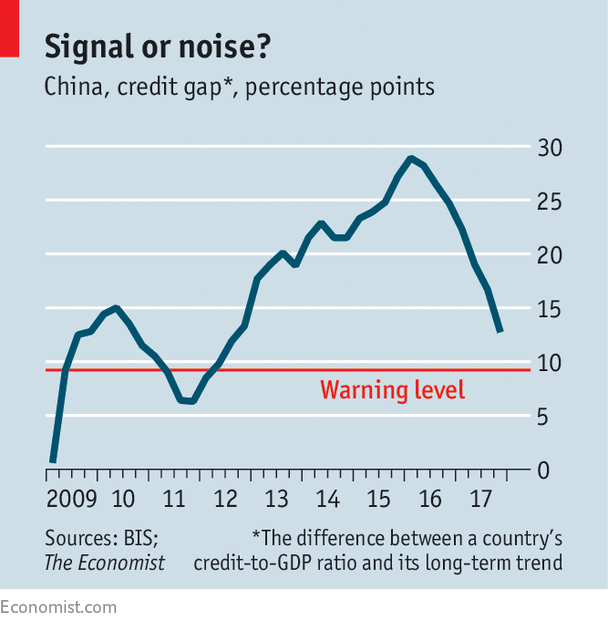

A similar concern motivates research at the Bank for International Settlements (BIS) in Basel, Switzerland. Its equivalent to the radar is a set of economic indicators that can potentially detect the approach of financial crises. A prominent example is the “credit gap”, which measures the divergence between the level of credit to households and non-financial firms, expressed as a percentage of GDP, and its long-term trend. A big gap may reflect the kind of unsustainable credit boom that often precedes a crisis. Anything above 9% of GDP is reason to worry, according to Iñaki Aldasoro, Claudio Borio and Mathias Drehmann of the BIS.

The biggest blips on the oscilloscope include Canada (9.6%), Singapore (11.1%) and Switzerland (16.3%), according to the latest readings, released on March 11th. But the one that has kept everyone’s eyes peeled is China, with a gap of 16.7% in the third quarter of 2017 (the latest BIS figure available).

As a crisis-detector, the credit gap has some appealing operating characteristics. It can stand alone. It can be estimated quarterly across many economies. And, according to Mr Aldasoro and his co-authors, it would have predicted 80% of the crises since 1980 in the countries and periods for which data are available.

The problem is that it has also predicted many crises that never arrived. When such early-warning indicators flash red, the chance of a crisis in the next three years is “around 50%”, says Mr Drehmann. The BIS provides over 5,200 credit-gap readings for the period since 1980. In over 850 instances, the gap exceeded 9% but skies remained clear.

The problems seem worse in emerging markets. Their data are patchier, covering just 13 crises. Of this unfortunate number, only eight were preceded by a big credit gap. (Another three struck within three years of the start of the data, which may be too early to provide a fair test of the indicator.) There have been many false alarms. The credit gap flashed red almost continuously in Chile in 1993-2002, reaching over 24%, but no crisis followed. It was also persistently large in the Czech Republic in 2007-14 and in Hungary in 2000-10 without any great trauma ensuing. The indicator successfully predicted the “Asian flu” in Indonesia, Malaysia and South Korea in the late 1990s, but only after sounding a false alarm in all three countries in the 1980s.

What about China? Paul Samuelson, a Nobel-prize winning economist, once joked that the stockmarket had predicted nine out of America’s last five recessions. Similarly, the credit gap predicted at least three out of China’s last zero crises. It rose above 9% in mid-2003, mid-2009 and mid-2012, where it has stayed since. China’s comeuppance may still arrive. But the gap is now closing rapidly. It has decreased from almost 29% in the first quarter of 2016 to less than 13% at the end of last year, according to The Economist’scalculations.

One obvious explanation for China’s resilience is that its credit is mostly home-grown, extended by domestic banks and other Chinese lenders. By contrast the crisis-struck emerging economies mostly relied on inflows of foreign capital to finance their current-account deficits with the rest of the world. Looking at both current-account gaps and credit gaps may provide better predictions, says Michael Spencer of Deutsche Bank. He calculates that China’s risk of a financial crisis this year is less than 8% (assuming a credit gap of under 13%) partly because it runs a current-account surplus of about 1.4% of GDP. If China’s government keeps credit stable as a share of GDP this year, this crisis-risk could fall to about 5%.

On that day of infamy in 1941, Mr Elliott took the radar blip far more seriously than his fellow operator did, despite being less experienced. Perhaps this should not be surprising. After less than three months of radar-watching, Mr Elliott was not yet jaded by routine. If a financial crisis eventually strikes China, many people will be caught out—not because of a lack of warnings, but because of too many.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.