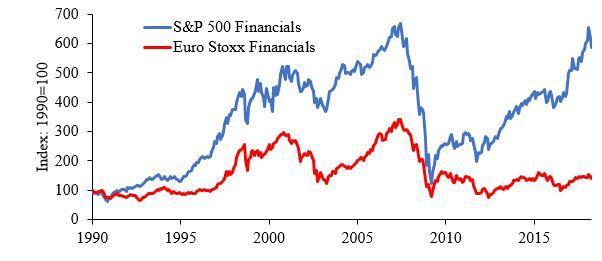

Ten years after the outbreak of the global financial crisis, banks in the euro area have not recovered. The Euro Stoxx Financials is only 40% above its March 2009 low, well below its pre-crisis level (Fig. 1). By contrast, the S&P Financials index in the US has risen by 320%. The different fates of European and US financial institutions could be due to the different monetary and regulatory crisis therapies of the European Central Bank (ECB) and the Fed.

Fig. 1: US and Euro Area Financial Stock Prices

Source: Thompson Reuters Datastream.

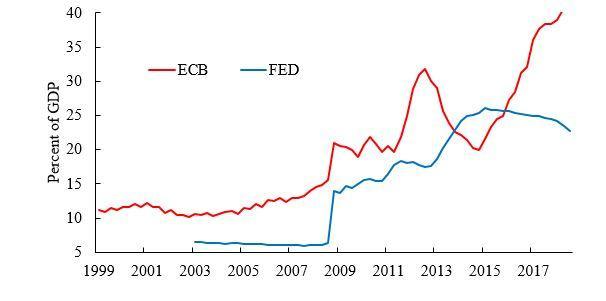

The Fed lowered its key interest rate faster than the ECB (Fig. 2) and expanded its balance sheet more quickly via quantitative easing (Fig. 3). The Fed dropped its benchmark rate down to an all-time low of 0.25% in December of 2008. The Fed's asset purchases included risky securitized mortgage loans, which helped prevent a financial meltdown during the crisis. The US Treasury also purchased more than $400 billion worth of securitized mortgage loans and bank shares under the Troubled Asset Relief Program (2009-2012). Thus, the banks were forcibly recapitalized. As asset and real estate prices recovered thanks to the Fed’s monetary policy, banks’ balance sheets were further stabilized.

In contrast, the ECB was more hesitant to lower key interest rates toward zero. The main refinancing rate only touched the zero bound in 2015 (Fig. 2). Tumbling banks in the southern euro states and Ireland inflated government debt, which finally triggered the European sovereign debt crisis from 2012 onwards. Large-scale outright purchases of assets only set in beginning in March 2015, after the first expansion of the ECB balance sheet via (targeted) long-term financing operations had gradually expired. Out of the ECB’s latest 2,600 billion euro asset purchases 80% were attributed to government bonds (Fed: 47%), which makes the quantitative easing of the ECB look more like a rescue program for ailing governments than for banks.

Fig 2: Key Interest Rates for Fed and ECB

Source: ECB, Federal Reserve Bank of St. Louis.

The large asset purchases of the Fed and the ECB through the quantitative easing programs led the commercial banks to maintain huge reserves at the central banks. The Fed decided to remunerate these excess reserves in 2008. With the interest rate on excess reserves climbing to 2.4% over the past few years, the Fed has transferred 95 billion dollars to US banks via this channel. In contrast, since 2014 the ECB has maintained a negative interest rate on commercial bank deposits (currently -0.4%), thus charging interest for excess reserves. German banks, for instance, have payed 20 billion euros to the ECB.

The Fed ended its ultra-loose monetary policy earlier than the ECB. Since the end of 2015 the Fed has been slowly pushing up the effective federal funds rate, which now stands at 2.3% (Fig. 2). As the Fed is cautiously reducing its balance sheet (which it began doing in 2016), long-term interest rates have also risen. The Fed has thus relieved US financial institutions of the burden of continuously shrinking interest margins. For instance, the net interest margin of J.P. Morgan climbed to 2.38% in 2018, up from 1.98% in 2017.

Fig 3: Size of Fed and ECB Balance Sheets

Source: ECB, Federal Reserve Bank of St. Louis.

In contrast, the ECB has sent no signals of higher key interest rates or a reduction in the huge holdings of government bonds. As a result, for instance, the interest margin of German banks has fallen from around 3.0% in March 2009 to 1.8% today. The transformation margin between yields on 10-year German government bonds and overnight money was reduced during the same time span from 2.8% to around 0.7%. Net interest earnings of German banks shrank from 66 billion euros in 2008 to 28 billion euros in 2018. As the ECB’s key interest rates remain low, net interest income of euro area banks is expected to shrink further.

On the regulatory front, Basel III increased capital requirements in the US and Europe. Both governments have taken additional steps to regulate financial institutions. In the US, the Dodd-Frank Act tightened regulatory requirements, while the Volcker Rule restricted lucrative proprietary trading. US financial supervisors have closed down 541 insolvent banks since 2008. Recently, however, the reporting requirements for almost all (but the largest) US financial institutions were relaxed again. Proprietary trading is still indirectly possible for large institutions via market making.

In the euro area, the ECB's Single Supervision Mechanism has been monitoring the 130 largest financial institutions in the euro zone since 2014. The euro area banks have to pay 60 billion euros into a bank rescue fund until 2023. The EU also created restrictions on proprietary trading that have led to a considerable decline in securities holdings. Frequent stress tests by the ECB are a burden on euro area banks, but they have done little to identify risks early, for instance at Dexia, BBVA/Garanti, Carige and Banca Monte dei Paschi.

In the euro area, shaky banks survive because they are kept afloat with national tax injections or via opaque network of rescue institutions such as EFSF, ANFA, EFSM, and ESM. The ECB's asset purchases and the TARGET2 payment system have turned out to be a quasi unconditional credit system: around a trillion euros have been handed out via TARGET2 to ailing southern European banks, with gradually eased collateral requirements. As a result, since 2008, the "Failed Bank Tracker" has reported only 52 bankruptcies for the entire euro area.

Shrinking interest margins and high regulatory costs are driving many small banks into mergers. (In Germany, the number of banks has fallen by 12% since 2008.) Failing banks are taken over by (still) more solid competitors - usually with the help of politicians. The volume of bad loans in the euro area is estimated to be between 650 and 1,000 billion euros. In 2018, the officially reported share of non-performing loans was 45% in Greece, 12% in Portugal, and 10% in Italy (1.3% in the USA). In reality, the shares may be larger. In particular in the southern euro area, funding by central banks are keeping a growing number of zombie banks afloat.

Finally, the diverging interest rate levels and the different successes of financial stabilization measures have triggered large capital flows from the euro area to the United States. The unresolved financial and government debt crises, the extended low interest rate policy of the ECB, and EU pressure toward fiscal austerity have all contributed to the huge capital outflows from the euro area (around two trillion euros since 2012). This has further destabilized European banks and enterprises. In contrast, the rising interest rates and the successful financial stabilization policies of the Fed have attracted large shares of these capital flows to the US, which have strengthened the quality of US credit portfolios.

The upshot is that the ECB’s monetary policy and financial supervision leaves the euro area banks unprepared for the upcoming economic downswing. The ECB may soon only be able to stabilize euro area banks through even larger purchases of securities and unconditional credit provision. This would be tantamount to progressive zombification, which promises nothing good for economic and political instability in Europe.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.