As we noted in Thursday’s missive on why QE may not work this time, Central Bankers globally have jumped back into the “emergency measure” pool.

- The Fed

- Has announced it will be “patient” with future rate hikes.

- The pace of QT, or balance sheet reduction, will not be on “autopilot” but instead driven by the current economic situation and tone of the financial markets.

- It is expected the Fed will announce in March that QT will end and the balance sheet will stabilize at a much higher level, and;

- QE is a tool that WILL BE employed when rate reductions are not enough to stimulate growth and calm jittery financial markets.

- China has launched its version of “Quantitative Easing” to help prop up its economy which grew at the slowest pace in nearly 30-years.

- China has taken fiscal and monetary policy measures such as fast-tracking infrastructure projects

- Additional monetary support for the economy

- A cut in taxes, and;

- A Reduction banks’ reserve requirements

- The ECB, after downgrading Eurozone growth, announced

- They will not raise rates in 2019, and;

- They will extended the TLTRO program, which is the Targeted Longer-Term Refinancing Operations scheme which gives cheap loans to struggling Eurozone banks, into 2021. (Currently, Italy, Spain, Greece, and Portugal all borrow more than they deposit and more tha $800 billion from the previous TLTRO is set to mature over the next two years. Without the extension of the program, defaults could rise sharply.)

But there is nothing to worry about, right?

Maybe, but if there is nothing to worry about, then why the sudden pivot by Central Banks? What are they seeing that you don’t?

As we discussed in our analysis, the macro-environment in the U.S. is markedly different than it was in 2009. The Fed’s starting point to battle the next recessionary environment is far weaker than it was then when the Fed funds rate was twice as high and the balance sheet four-times smaller.

Here is the important point. We, as investors, have been trained over the last decade to “buy” whenever Central Banks are engaged in monetary interventions. So far it has worked in lifting asset prices higher. But therein lies the risk of complacency.

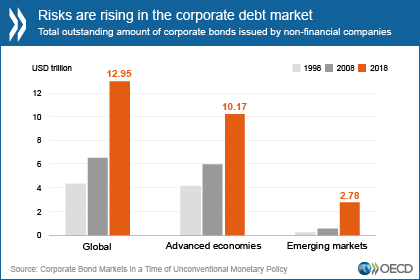

In 2009, most of the risk in the financial and credit markets had been wrung out from the decline. Today, the markets are more exposed than ever to leverage and credit risk throughout the global ecosystem.

My friend Doug Kass had a great note Friday related to this risk.

“Astonishingly I heard a ‘talking head’ on one of the business media platforms earlier this week who said that none of the excesses that existed in past recessionary periods are in place today.To say excesses, systemic issues, and possible instability, don’t exist is borderline irresponsible.As I see it, there are several measurable excesses and associated risks that represent this cycle’s new challenges that may be summarized into these five categories:

- An untenable level of global (private and public sector) debt

- Structural instability and growth threats in the form of rising deficits and demographic trends (i.e., slowing population growth)

- Lack of (sovereign) cooperation

- Unparalleled political instability and rising policy risks

- A dangerous shift in market structure

DebtDebt that is not self-funding is future consumption brought forward.Through years of unprecedented monetary ease, we have enjoyed unsustainable consumption and growth which cannot continue at its current pace in the future. Debt, then, is a drag on future growth, and the amount of debt the world now has will be a monster drag on that growth.The fact is that the global economies are over levered with debt in our private and public sectors that are excessive. As I chronicled in “Why Interest Rates Are the Bull Market’s Most Serious Threat,” in the fullness of time, the weight of debt will act as a governor to economic growth – it saps capital. To think otherwise is foolhardy.

Deficits and Demographic ThreatsUnder the weight of rising and uncontrolled deficits (supported by both parties) and slowing population growth, intermediate to longer-term economic and profit growth prospects are diminishing. Near term, domestic economic growth is already weakening (as supply side economics is being further discredited). At the same time Chinese growth is failing to stabilize and it appears that Europe is entering a deepening recession – underscoring the fragility of the global economic system that is still being propped up by low or negative interest rates.ChinaIt is my core expectation that U.S. and China will fail to agree on trade. (My baseline expectation is that investors will view a likely, superficial agreement as no agreement at all). We will find out shortly whether my view is accurate and that there will be no big deliverables with regard to IP theft and/or technology exchange. The consequences for the global economy are obvious – China accounts for only about 14% of world GDP but accounts for about one third of the delta in global economic growth.Earnings & RiskMost importantly, for investors, the consensus expectations for corporate profits, and economic growth expectations, remain far too optimistic.”

I will steal his last line as I agree that risks currently remain to the downside which explains our cautious outlook for 2019-2020.

If the message that Central Banks are sending comes to fruition, it will likely be a challenging backdrop for equities in the months ahead.

Currently, it certainly seems these concerns are outlandish and far fetched but the data is all too present and real. After a scorching run in the first two months of the year, it is hard to see anything as being bearish, but therein lies the risk.

As an investor, our job should be an honest evaluation of our portfolio allocations and our investment strategy with relation to the relevant market risks.

In other words, ask yourself this one simple question:

“What will happen to my money if something goes wrong?”

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.