Stocks are a decent inflation hedge in the long run, but over shorter horizons, there is an inverse relationship

In places where it has been long absent, it is hard to remember what a curse inflation is. In other places, it is hard to forget it. Take Zimbabwe. In 2008 it suffered an inflation rate in the squillions. Prices doubled every few weeks, then every few days. Banknotes were so much confetti. Some people turned to equities as a store of value. A share purchased on Monday might be sold on Friday. Harare’s stock exchange was almost like a cash machine.

In principle, equities are a good hedge against inflation. Business revenues should track consumer prices; and shares are claims on that revenue. In some cases, they may be the only available hedge. Iran, for instance, has had one of the better performing stockmarkets, because locals have sought protection from inflation. Sanctions make it dangerous to keep money offshore.

Rich-country investors have a different sort of headache. Though the immediate outlook is for inflation to stay low, it could plausibly pick up later on. If it does, edge cases like Zimbabwe or Iran are a bad guide. The link between inflation and equity returns is not straightforward. Stocks are a decent inflation hedge in the long run. But over shorter horizons, there is an inverse relationship. Rising inflation is associated with falling stock prices, and vice versa.

Start with the evidence that stocks beat inflation over the long haul. In the most recent Credit Suisse global investment returns yearbook, a long-running survey, Elroy Dimson, Paul Marsh and Mike Staunton show that global equities have returned an average 5.2% a year above inflation since 1900. You may quibble that the survey covers the sorts of stable places that have had a long run of stock prices in the first place, such as Britain and America. Even so, the finding fits with intuition. When you buy the equity market, you buy a cross-section of a country’s real assets.

Yet stock investors still need to be mindful of inflation. Markets tend to put a lower value on a stream of cash flows when inflation rises; and a higher price on cash flows when it falls. There are competing theories for the inverse relationship; many date from the late 1970s and early 1980s. A paper written by Franco Modigliani and Richard Cohn in 1979 put it down to “money illusion”: rising inflation leads to falling stock prices because investors discount future earnings by reference to higher nominal bond yields. The correct discount factor is a real yield (ie, excluding compensation for expected inflation). Other theories said that inflation is merely a reflection of deeper forces that hurt stock prices: an overheating economy; rising uncertainty; political instability.

In the decades since then, inflation has steadily declined. Stocks have re-rated. Investors have been willing to pay an ever-higher price for a given stream of future earnings. You might put this down to the Modigliani-Cohn effect in reverse, since nominal bond yields have also fallen. But so too have long-term real bond yields. The real rate of interest needed to keep inflation stable is lower.

Now for the headache. For the most part, financial markets reflect the view that inflation will remain low. Nominal bond yields are negative in much of Europe and barely positive in America. In stockmarkets, there has for a while been a sharp divide. Companies that do well in disinflationary environments (technology, branded goods) are expensive; businesses that might do better in inflationary ones (commodities, real-estate and banking) have generally lagged behind. The immediate prospect is indeed for an excess of supply. The unemployment rate in America is close to 15%. Inflation is already falling.

Further out, though, the outlook for inflation is murkier. There is no shortage of pundits who say it is primed to pick up. They have a case.

Globalisation, a key reason for the secular decline in inflation, is reversing. Big companies are likely to emerge from the crisis with more pricing power. The rise of populism in rich countries is hard to square with endlessly low inflation. Fiscal stimulus is in favour. The more government debt piles up, the greater the temptation to try to inflate it away.

For all such speculation, it is far from clear whether, how fast and by how much inflation might rise. A modest pickup might even be good for stock prices—especially in Europe, where bourses are tilted towards the cyclical stocks most hurt by unduly low inflation. But it is foolish to believe that inflation will leave your stock portfolio unharmed—and too easy to forget the damage it can do.

In April with the world in lockdown from covid-19 and oil demand sinking faster than at any time in history, oil producers from Dhahran to the Delaware basin made the only possible choice: cut supply, fast. American output fell by about 2m barrels a day between March and May. The Organisation of the Petroleum Exporting Countries (opec) and its allies agreed to reduce supply by a record 9.7m barrels a day in May and June. The cuts helped propel the price of a barrel of Brent crude from less than $17 in mid-April to $42 on June 5th.

On June 6th, with demand still fragile, the opec alliance extended the cuts by a month. It is one thing to see supply drop when the oil market is engulfed by crisis. The more interesting question is how quickly supply will climb as normality returns. Production will respond, of course, as demand rises for jet fuel, petrol and diesel. If prices remain over $40, some shale firms and petrostates may boost output this summer. In the longer term, though, supply faces other constraints.

Global investment in future supply has collapsed. The International Energy Agency (iea), an intergovernmental forecaster, estimates that upstream investment this year will fall to its lowest since 2005 (see chart). Goldman Sachs, a bank, expects production outside opec to stagnate in the 2020s, due not to geology or even demand, but lack of investment. Bernstein, a research firm, thinks that non-opec supply, which accounts for about 60% of global output, may peak in 2025, and then only at around last year’s level.

That would mark a dramatic shift. Because oil reserves are depleted continuously, producers have usually operated under the tenet of drill or die. An analyst once asked Lee Raymond, then the chief executive of Exxon, what kept him up at night. “Reserve replacement,” he responded.

The obsession with booking reserves, not surprisingly, supported the growth of supply. In the mid-2000s, as some fretted that the world might run out of oil, both listed and state-backed firms scoured the world for projects. Over the past decade, fracking has unleashed supply across America’s heartland, transforming the country into the world’s largest oil producer (see chart). Big projects in Norway and off the coast of Brazil, where oil lies beneath a thick layer of salt below the sea floor, helped boost supply, too.

Investment began falling, though, even before the pandemic. A crash in prices from 2014 to 2016 had sapped appetite for big, risky projects. Even after prices climbed in 2017 poor returns made investors less interested in reserve replacement than cash flow. Companies have squeezed suppliers and found ways to pump more oil from existing fields. ExxonMobil and Chevron are among the giants to invest in America’s shale basins, where output is relatively easy to ramp up and down.

Oil producers can now credibly say they are able to wring more value from their capital budgets. Still, the decline in investment was steep enough to stir debate over future supply. Upstream spending on oil and gas last year was 43% below that in 2014, according to the iea. Bernstein examined the 50 biggest listed energy companies outside opec and the former Soviet Union. In 2019 they reinvested an average of 64% of their operating cash flow. The long-term average was 87%.

The pandemic has exacerbated matters. Producers have shut in wells, delayed projects and slashed investment further. Rystad Energy, a data firm, estimates that of the 3m barrels a day that were shut in last month, mainly in America and Canada, 10-15% will never restart. The iea predicts that investment in supply will be 33% lower this year than in 2019 and 62% lower than the high in 2014. There is less fat to trim than there was five years ago, the iea reckons. That means declining investment may have a greater impact on supply.

Some companies, such as ExxonMobil, remain focused on growth. But it is not clear when a broader surge in capital spending will come. Returns for many firms have fallen below the cost of capital, points out Neil Beveridge of Bernstein. Investors are unlikely to favour a return to rapid expansion; the energy sector’s performance has been poor, the rebound in demand is uncertain and greener regulation may be in the offing. In a sign of the times, JPMorgan Chase, America’s biggest bank, demoted Mr Raymond from his role as its board’s lead independent director in May, under pressure from climate activists. Michele Della Vigna of Goldman Sachs argues that the historic cycle of high prices, investment and supply may be breaking.

As for American shale, analysts are feverishly watching rig counts, pipeline data and shut-ins for signs of a surge in supply. Shin Kim of s&p Global Platts, a data firm, expects it to tick up briefly this summer, as prices recover. But there is consensus that growth in the 2020s will be muted compared with the boom. Shale output is vast and wells’ production declines are steep. Improvements to productivity have slowed. Investors can find better returns elsewhere.

This bodes well for opec and its allies, which have been battered in the past decade. In 2014-16 it waged a failed price war to wipe out American frackers. Since then the cartel and its partners, led by Russia, have propped up oil prices enough to sustain shale, but not enough to support many members’ domestic budgets. In March Saudi Arabia urged Russia to slash output; Russia refused, loth to let Americans free-ride on opec-supported prices. The ensuing price war was spectacularly ill-timed, as it coincided with the biggest drop in oil demand on record.

The desire to chasten American frackers remains, though. opec controls about 70% of the world’s oil reserves, more than its 40% market share would suggest, points out Martijn Rats of Morgan Stanley, a bank. If the world’s appetite for oil shrinks due to changing habits, cleaner technology or greener regulations, countries with vast reserves risk having to leave oil below ground. “opec will defend its market share more firmly in the future,” predicts Mr Rats. Even better, then, if state-owned firms can depend on their rivals’ paltry investment to limit supply for them.

That is the judgment a lot of investors apply to the recent across-the-board surge in asset prices. For it is not just the stockmarket that has rallied. The prices of industrial raw materials have also risen sharply in the past month or so. Iron ore has increased from $80 a tonne to over $100. Copper prices are also up 25%. This is remarkable. The global economy is only just reopening. It feels a bit early for a commodity boom.

It is tempting to see parables here. Perhaps the metals rally is a template for the post-virus economy, in which supply bottlenecks push prices up as activity gets going again. Perhaps it shows how mindlessly the ocean of liquidity created by the Federal Reserve and the European Central Bank has washed into financial markets of all kinds. For the “too-soon” school it is a sign that optimism is running ahead of reality. Perhaps it is. But quite a lot of the commodity story seems to be about China.

China’s role is both curious and obvious. It is curious because China’s economy is meant to have become more reliant on consumer spending and less on building booms financed by ever-larger dollops of debt. It is obvious because, notwithstanding this stated goal, China is still the world’s biggest buyer of industrial commodities. Almost all the seaborne trade in iron ore goes there. If metal prices are going up, it is a fair bet that something is happening in China.

And so it is. Steel mills are working flat out. In the first week of June, China’s steel blast furnaces were operating at 92% of capacity. That is a good deal above the 80-85% rates considered normal. Much of the steel manufactured in China is for buildings and for infrastructure, such as bridges, railways and subway lines. Sure enough, indicators of construction activity look strong. Sales of excavators are up by a fifth so far this year, compared to a year earlier. A pipeline of orders had already been building before the pandemic struck. In its aftermath, construction has been given an extra push by the government’s efforts to gin up the economy. China-watchers say lessons have been learned. There has been a greater focus than in the past on selecting worthwhile projects, says Sean Darby, a Hong Kong based analyst for Jefferies, an investment bank.

The supply response to this has been led by Australia, the world’s largest exporter of iron ore. It swiftly took steps to contain the virus at the outset. It has managed, at the same time, to keep its mines in the ore-rich Pilbara region open. Exports of ore have risen this year. This contrasts with Brazil, where the spread of the virus has crippled production. Such bottlenecks are one reason for higher prices. And there is a bigger picture. The mining industry suffered a brutal reckoning in 2014-16, after a decade-long boom fuelled, yes, by China. Investment was cut; mines were closed; debts were paid. The result is that the industry does not have the chronic over-capacity of many other cyclically sensitive ones—think European banks or global carmakers.

There is a speculative element to the rise in metal prices, too. Buying or selling copper futures is a popular way to express a view about the world economy. Indeed copper can be all about belief, says Max Layton of Citigroup, a bank. Many of the bets laid on it are by trading algorithms, which mechanically respond to financial signals that have worked well in the past. The dollar, which has fallen by 6% against a basket of currencies since March, is usually part of the semaphore. A weaker dollar allows for easier terms of finance in emerging markets. Anything that helps emerging-market economies is generally good for commodity prices. So the algorithms buy.

The complex of price changes becomes self-reinforcing. Higher ore prices bring higher-cost producers back to the market. But their profit margins are then squeezed as their home currency appreciates, because that raises the cost of labour in dollars, in which commodities are priced. To restore margins, prices must go up. Moreover, marginal costs rise when the prices of steel (used for mining parts) and oil (used for energy and chemicals) go up. These higher costs push up prices further, says Mr Layton.

A pattern in markets is that a lot happens by rote. China’s response to a weak economy is to build; investors’ response to the Fed’s easing is to buy stocks; the algorithms’ response to a weaker dollar is to buy commodities. Higher prices beget higher prices. The sceptics, the too-sooners, note that this also works in reverse. Quite so. But the momentum is now with the believers

Two months ago, when the market was in a state of near-total chaos as a result of a sudden collapse in global supply chains due to the hasty coronavirus lockdowns, one market that saw unprecedented turmoil was that of physical gold.

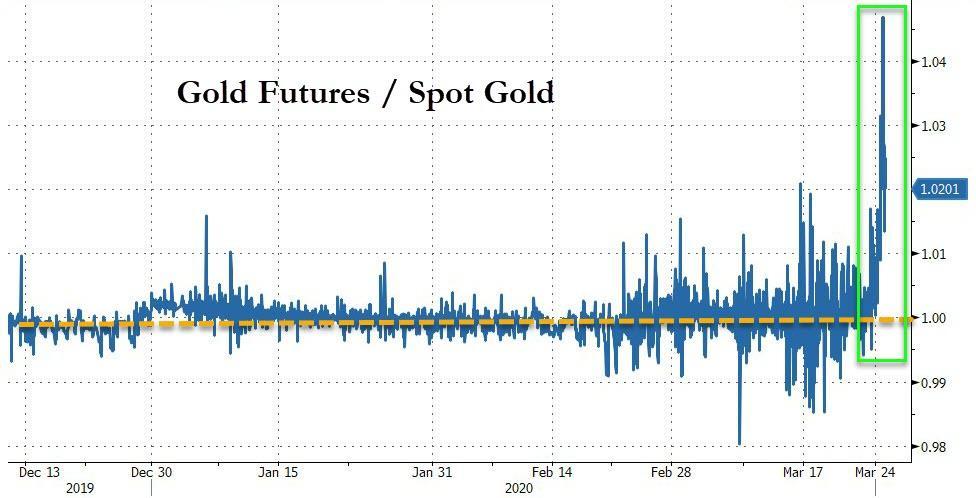

As it was pointed out in late March, due to a sudden breakdown in physical gold supply as the world's top gold refiners, those located in the southern Swiss town of Ticino, namely Valcambi, Pamp and Argor-Heraeus, suddenly stopped producing gold, the result was a record divergence in the price of spot gold vs gold futures contracts...

... with gold futures decoupling and trading far above spot prices.

The resulting record divergence in gold futures vs spot (in some way analogous to what happened to the price of the prompt WTI contract in April, when the May WTI contract traded as low as ($40) as traders were willing to pay buyers to store oil in a world where there was suddenly no space for the physical commodity), unleashed a flood of physical gold into the US as a record scramble by traders rushing to take advantage of this arbitrage opportunity by shipping bullion to New York sparked what Bloomberg said "may be one of the largest ever physical transfers of the metal."

"The flows into New York are unprecedented," Allan Finn, the global commodities director at logistics and security provider Malca-Amit told Bloomberg as his company’s teams in New York have been working 24 hours a day to cope with unprecedented demand for physical gold while navigating lockdowns, flight disruptions and social distancing.

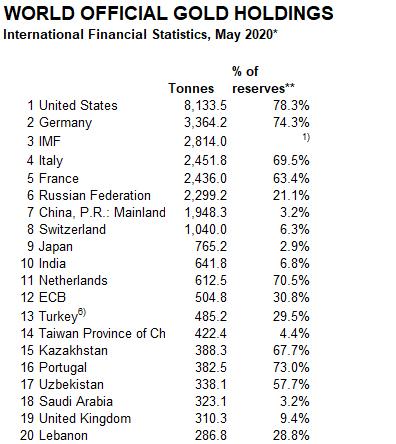

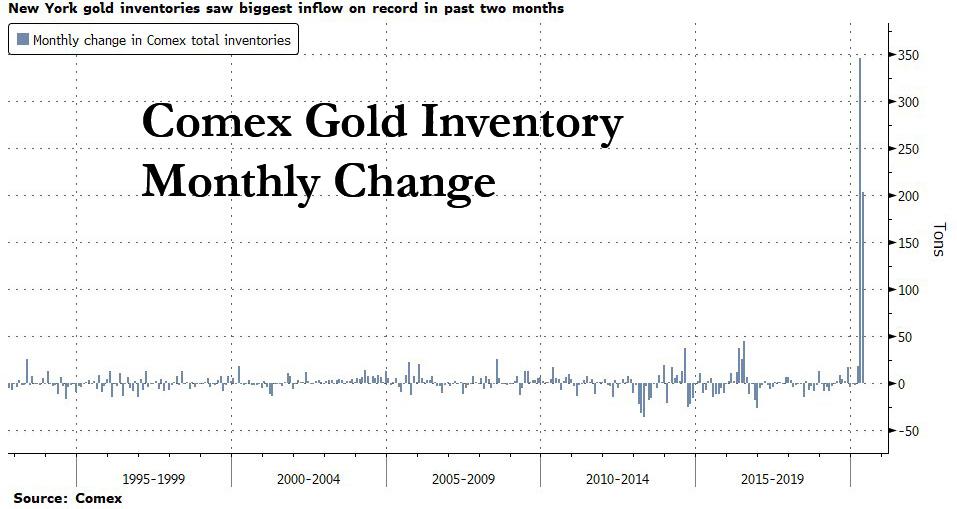

Since late March, no less than 550 tons of gold - worth $30 billion at today’s price and roughly equal to global mine output in the period - have been added to Comex warehouse stockpiles; hundreds of tons of that was imported. On its own that amount of gold would represent the 11th largest sovereign holding, larger than the ECB's official 504.8 tons of gold.

Traditionally, while tens of billions of dollars of gold change hands every day in financial markets, a much smaller amount tends to physically move between vaults in trading hubs like London, Zurich and New York. But that has not been the case in the past two months: it all started to change as the Covid-19 crisis affected the supply chain. As Bloomberg explains what we first highlighted two months ago:

"when planes were grounded and Swiss refineries closed in late March, traders were worried they wouldn’t be able to get gold to New York in time to deliver against futures contracts. That caused futures, which typically trade in lockstep with the London spot price, to soar to a premium of as much as $70 an ounce.

That created an opportunity for enterprising traders: buy gold somewhere in the world at the spot price, sell futures, and benefit from the difference by shipping the metal to New York."

The scale of the trade has been revealed in exchange reports, import and export data and comments from some of the leading precious metals shipping and vaulting companies. It all came to a head on Thursday, when traders declared their intent to deliver a record 2.8 million ounces of gold against the June Comex contract, the largest daily delivery notice in exchange data going back to 1994.

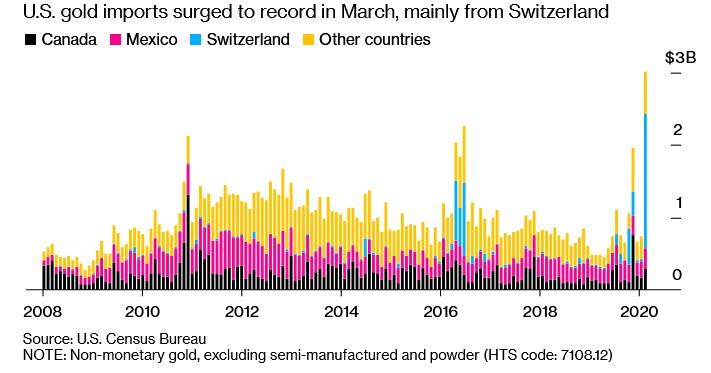

The bulk of this gold came from Switzerland, as Swiss gold exports to the US surged, reaching 111.7 tons in April, the highest on record. Already in March gold imports topped $3 billion, according to the Census Bureau, the highest in at least a decade.

To meet the unprecedented demand for physical gold, refineries as far away as Australia have ramped up output of kilobars - the form typically delivered on the Comex - to ship to New York.

For Brink’s Managing Director Mark Woolley, the spike in demand to ship gold to New York has been unlike anything he’s seen in 20 years in the market.

“The amount of metal that we’ve successfully moved into New York is pretty significant,” he said Thursday on a webinar hosted by the London Bullion Market Association. “It’s probably not far off the total amount of metal that’s been mined in this period.”

As discussed previously, the CME Group which owns Comex, responded to the unprecedented market dislocation and the sudden lack of physical gold in New York by introducing a new contract allowing the delivery of 400-ounce bars, the type traded in London. Still, “other changes need to be at least considered,” according to LBMA Chairman Paul Fisher.

Valcambi 400 oz "Good Delivery" Gold bar.

With investor demand for physical off the charts, the enormous movement of gold has been a blessing for logistics companies but also a curse: not only have passenger flights - on which shipments are typically transported - been grounded, but New York City, where many Comex warehouses are located (recall JPM's giant gold vault just happened to be located right next to the NY Fed's), has also been a hotspot for the virus.

To deal with flows, Loomis International U.K. opened up additional vault capacity. Malca-Amit considered using airports in Boston and Philadelphia, but hasn’t needed to yet, Finn said.

That said, while large volumes and virus-related restrictions at vaults and airports caused some delivery delays, much of the spike in the premium for futures contracts in March - which left banks such as HSBC suffering hundreds of millions in losses - was driven by perception rather than reality, Finn said.

Still, the bonanza for precious metals shippers may last a while. As it was pointed out last week, large deliveries have seen June Comex futures drop to a discount to spot prices this week, but later dated futures are still at a premium. In fact, according to BofA, in a world in which central banks are flooding markets will trillions in freshly printed fiat and faith in the monetary system is quietly shrinking one day at a time, the one asset the "smart money" wants - as it dumps stocks - is, you guessed it, gold.

In fact, a simple correlation between the flood in the global money supply and the price of gold suggests the yellow metal has about $1000 of upside.

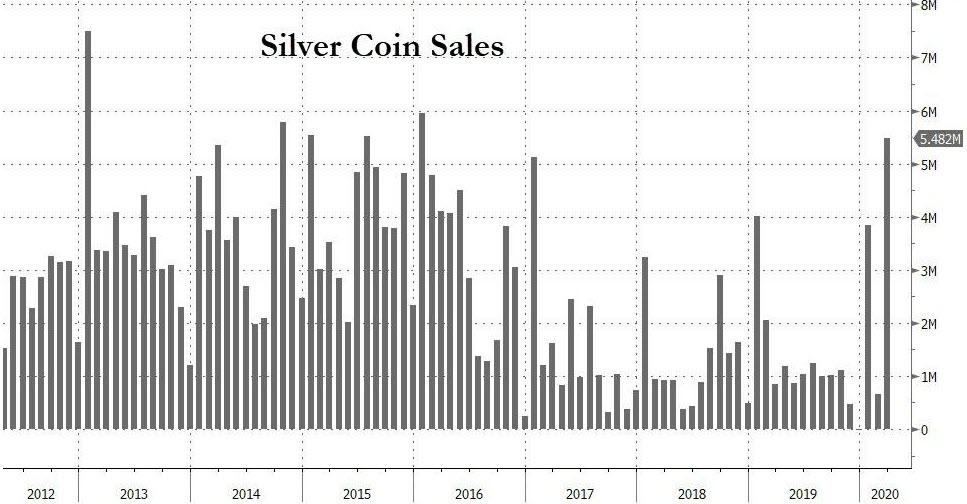

Meanwhile, as investor interest in other precious metals picked up, futures for silver and platinum have also traded at premiums to spot: “The guys in New York have done a great job,” said Brian Hayward, head of Loomis International U.K.

"We’re seeing a lot of silver head that way right now" Hayward said in what may be very good news for fans of silver, which recently hit record lows against gold...

Supermajors claim their prospects are not as bleak as they seem

The annual shareholder meetings of ExxonMobil, Chevron and bp, all held on May 27th, each resembled a yearly check-up in a burning clinic. Covid-19 has caused the deepest collapse of demand for the oil giants’ products in history. In April Royal Dutch Shell, an Anglo-Dutch firm, cut its dividend for the first time since the second world war. On May 1st ExxonMobil reported its first loss since the mega-merger that formed the group in 1999.

Even before the pandemic investors were searching elsewhere for lower risk and higher returns. Energy was the worst-performing sector in the s&p 500 index in four of the past six years. Yet the supermajors argue that, for all that, their prospects aren’t bad.

They have half a point. Many of them have become more resilient since the last downturn, in 2014, pursuing more profitable projects and cutting costs. The oil price required to cover capital spending and dividends for the seven biggest—ExxonMobil, Shell, Chevron, Total, bp, Equinor and Eni—is about half what it was in 2013, reckons Goldman Sachs, an investment bank (see chart).

More oil firms are also preparing for a low-carbon future. In December Repsol of Spain pledged to reach net-zero emissions from its operations and the sale of its products by 2050. bp, Shell, Eni and Total have since announced their own commitments.

Moreover, as smaller oil firms reel from the virus, particularly in America’s shale basins, bigger ones may scoop up their assets. The supermajors’ spending cuts may slow their oil production. But that is only a problem if you think there is value in production growth, says Michele Della Vegna of Goldman Sachs. If excessive growth is the problem, he says, then cuts could be part of the solution.

There are two hitches. The break-even price for some firms, though lower than it was, remains high. ExxonMobil’s stands at $70, double what oil trades at today. And it is unclear how quickly—or if—supermajors should move away from oil investments. ExxonMobil and Chevron, America’s biggest oil firms, think not. Neither has set a goal for curbing emissions from the sale of their products. On May 27th ExxonMobil’s shareholders voted against splitting the roles of chairman and chief executive. Green investors had hoped an independent chairman might spur change.

European supermajors look like Birkenstocked tree-huggers in comparison. Still, their promises are loose. Italy’s Eni said in February that its oil-and-gas production would plateau by 2025, but left wriggle room for a “flexible decline” for oil thereafter. On May 5th Total vowed to reach net-zero—but only for products sold in Europe. Shareholders will consider a resolution for more expansive goals on May 29th. bp, under pressure from activists, is working to explain how it can meet climate targets.

The firms have a way to go. Norway’s Equinor devoted about 8% of capital spending last year to renewables; Shell’s figure was 2%. Meanwhile, a new type of rival is emerging. At $68bn, the market value of Iberdrola, a Spanish utility that develops solar and wind farms, has overtaken Eni’s and Equinor’s, and is chasing bp’s

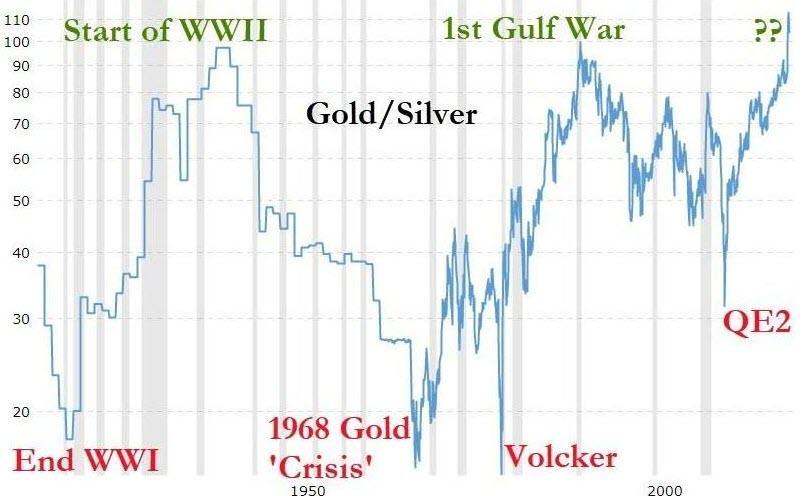

There’s a debate in gold bug circles over whether the price difference between gold and silver – the gold/silver ratio – tells us anything useful.

Some skeptics, for instance, view the original gold/silver ratio of 15 - from America’s 18th century bi-metallic system – as just a political number pulled more-or-less out of thin air by Alexander Hamilton and therefore useless today. Others note that gold is a purely monetary metal and silver is part industrial, part monetary, and conclude that it’s apples to oranges - and therefore not an indicator of future prices.

Both points are factually defensible, sort of. But they’re also irrelevant. The real reason the gold/silver ratio has tended to fluctuate within a broad but well-defined range is that humans have a vivid visual imagination.

Here’s how it works:

Early in a precious metals bull market, people are skeptical of the need for safe-haven assets, so the money that flows into the sector goes mostly to the big-name, super-safe choice, which is gold. Gold goes up relative to silver, and the gold/silver ratio expands.

Gold keeps rising and new money – much of it attracted by the metal’s newfound price momentum rather than an understanding of the nature of money – flows in, pushing gold even higher.

The early gold investors register big gains and begin to feel smart and therefore more willing to take on a bit of extra risk in return for potentially even bigger gains. They look around for “the next gold” and find silver, the other monetary metal, languishing at a relatively low price.

Then they start thinking in images. First, they picture a single one-ounce gold coin and consider what it would cost. At gold’s new, higher price, this seems like a lot of money for such a small, though admittedly pretty, thing.

Next, they consider the price of silver and envision how many – also very pretty – one-ounce coins they can buy for the price of a single ounce of gold. And their imagination conjures up something like this:

Suddenly, silver looks extremely cheap. For the price of a single Gold Eagle, one can get two heaping handfuls of shiny, heavy silver ounces.

A bit more consideration reveals that in a SHTF scenario, silver coins are actually more useful than gold because their smaller denominations allow them to function as $20 bills rather than gold’s illiquid $1,000 +. You can buy groceries and bullets with silver coins.

Suddenly aware of silver’s advantages, investors conclude that at current relative prices, the choice is a no-brainer. Silver is the precious metal to load up on.

Adjust this thought process for the global pandemic’s distortion of most markets and convert it into a chart, and you get the past two months’ gold/silver ratio, which depicts a bout of hair-on-fire panic followed by a trend back towards traditional norms:

So what happens now? Historically, both precious metals keep rising, with silver rising faster than gold until the imagined pile of silver required to buy a single ounce of gold looks something like this:

Then the process shifts into reverse, with a single gold coin looking better in the mind’s eye than a paltry few bits of silver.

We are nowhere near that point, so expect investor imaginations to work in silver’s favor for years to come.

{kind=link}