A Chinese electric vehicle maker, BYD, is attracting a lot of positive sentiment from analysts covering the company, according to a Bloomberg poll among 27 analysts. A total 18 of these have a “buy” stance on the company despite it losing US$3 billion in market cap because of lower government subsidies and intensified competition from foreign manufacturers.

The revision in the subsidy regime for electric vehicles hurt the company badly. BYD recently said its first-quarter income would be a staggering 92 percent lower than in the previous quarter because of the lower subsidies. Yet the company will later benefit from higher subsidies that Beijing will continue providing for longer-range electric vehicles.

Speaking of long-range electric vehicles, BYD is one of the Chinese companies driving a potentially major decline in diesel fuel demand in China with their fast-growing electric bus fleet. This fleet could displace almost 280,000 bpd in fuel demand.

Bloomberg reported today that electric bus fleets across Chinese cities are expanding at the rate of 9,500 every five weeks. Last year, 99 percent of all electric buses in the world—some 380,000 of them—were in China. BYD’s electric bus production to date is 35,000, but it now has the capacity to roll out 15,000 annually.

Foreign competition is not a cause for concern for BYD, according to the analysts Bloomberg polled, even from Tesla or Nissan, which produces the most-sold electric car, the Nissan Leaf. In fact, Bloomberg estimates that BYD’s earnings per share this year will jump by 32 percent, which will outperform the rest of the sector in the country. For the Chinese EV industry as a whole, Bloomberg has estimated EPS growth at 29 percent.

China is pushing electric vehicle adoption urgently as part of efforts to deal with pollution. Beijing has a target of a sevenfold increase in the sales of the so-called new energy vehicles and is considering a ban on gas guzzlers. Still, the subsidies for new energy vehicles are planned to be phased out by 2020, which means that local and international EV makers have less than three years to find ways to survive on their own without subsidies.

The most immediate risk is a trade war, not a turn in the cycle

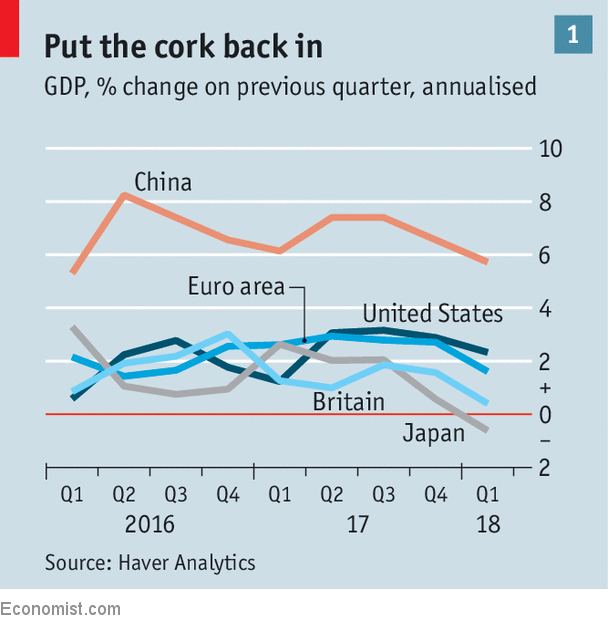

IN 2017 the global economy broke out of a rut. It grew by 3.8%, the fastest pace since 2011. Surging animal spirits accompanied a rebound in business investment across the rich world. Global trade growth rose to 4.9%, also the fastest rate since 2011. Emerging-market currencies appreciated against the dollar, keeping inflation low and debts affordable. Financial markets wobbled in February, but only after reaching all-time highs. In April the IMF said that the global economic upswing had become “broader and stronger”.

Since then that healthy glow has begun to fade. First, economic surveys in Europe took a turn for the worse (presaging growth in GDP of only 1.6%, annualised, in the first quarter). Then the rest of the world seemed to catch the same cold (see chart 1). In the first quarter America’s growth slowed to 2.3%, annualised, from close to 3% in the preceding six months. At the same time, Japan’s economy shrank by 0.6%, ending a growth spurt sustained since the start of 2016. Investors have begun to wonder if the period of global exuberance is over. Even policymakers in China, which has seemed relatively immune to the slowdown, have taken note of weakening domestic demand. In mid-April they loosened monetary policy slightly by allowing banks to hold fewer reserves.

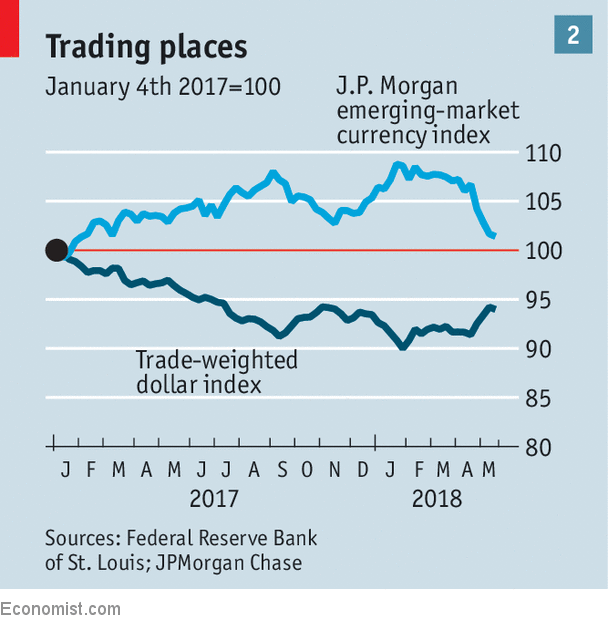

Meanwhile, the slow upward march of American bond yields—the result of expectations of higher inflation and interest rates—has turned the screw on emerging-market currencies, which have fallen by 5.4% since the start of April (see chart 2). A run on the peso has forced Argentina to ask for an IMF bail-out and raise interest rates to 40%. The Turkish lira has also taken a beating, in part because the president, Recep Tayyip Erdogan, says that low interest rates reduce inflation . On May 15th he promised to take more control of monetary policy after the upcoming election.

Make no mistake: world growth has slowed, but it remains strong. Surveys of activity in China, America and Europe are, when combined, higher than they have been 83% of the time over the past decade, according to UBS, a bank. Poor weather may have depressed European growth in early 2018. America’s economy often seems to slow early in the year, only to rebound, a phenomenon dubbed “residual seasonality”. Strong retail sales and high consumer confidence suggest that if a downturn is coming, Americans have missed the memo.

In a way, however, that is part of the problem. Demand is piling up where it is least needed. American core inflation, which excludes volatile food and energy prices, is now 1.9%, according to the Federal Reserve’s preferred measure. That is only just below the central bank’s target. And the economy has yet to feel the full impact of the tax cuts and spending rises President Donald Trump recently signed into law.

Outside America, however, inflation is falling short almost everywhere. In the euro zone it is only 1.2%, no higher than at the end of 2016. The Bank of Japan recently abandoned its pledge to raise inflation to 2% by fiscal year 2019—a target it had already postponed six times. Inflation in most emerging markets has been subdued, too. Even in Brexit Britain, where a big fall in the pound pushed inflation well above the 2% target in 2017, it has tumbled more quickly than expected.

In theory, the world economy would be better off if this demand were spread around. Unfortunately, the mechanism that could achieve that is a dangerous one: a stronger dollar. In theory a rising greenback should allow Americans to buy more imports, stimulating foreign economies. In practice a rising dollar can play havoc with emerging markets that have dollar debts. And because so much trade is invoiced in dollars, a stronger American currency reduces trade between other countries, too. Four of the past five Fed tightening cycles have eventually triggered a crisis in emerging markets.

Yet there are reasons to be more confident this time. Among the ten largest emerging markets, only Turkey and Argentina ran current-account deficits greater than 2% of GDP in 2017. Most have dollar debts that are comfortable compared with the size of their economies.

Another threat talked up by bears is the oil price, which has risen to close to $80 a barrel. They think this will push inflation up further, forcing higher interest rates. But the Fed usually ignores temporary inflation driven by energy prices. And predicting the impact of oil prices on the world economy has become trickier than it was before the shale revolution. Pricier oil now tends to boost American investment. In any case, it is driven at least partly by demand, reflecting healthy growth.

The biggest risk to the world economy remains the possibility of a trade war. Mr Trump is negotiating with China and others with the aim of closing America’s trade deficit. That is difficult to square with a rising dollar sucking in imports. The danger is that slightly slower global growth, combined with ongoing stimulus in America, lays bare this problem and further provokes Mr Trump’s protectionism. That could set off a downturn that would really be worth worrying about.

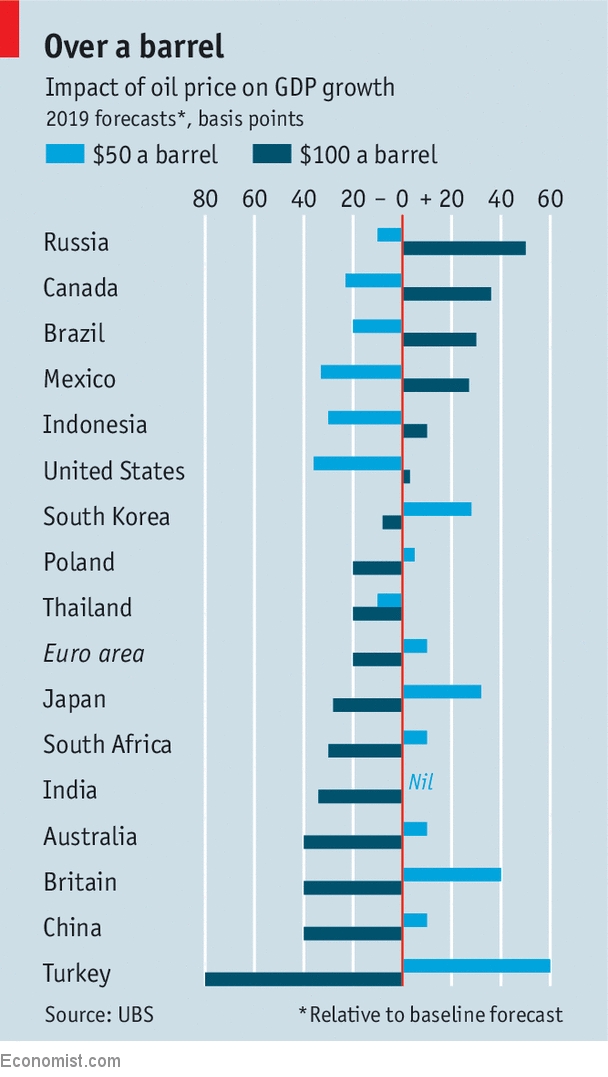

When they are not fretting about the American dollar or Chinese debt, policymakers in emerging economies keep a close eye on the oil market. The price of Brent crude has risen by nearly 50% in the past year to around $80 a barrel. It ranks as the 11th-biggest spike in the past 70 years (adjusted for inflation), according to UBS, a bank. So should emerging markets now worry that oil prices will carry on rising above $100, or that they will tumble below $50? The answer is yes.

Many emerging economies import oil; others export it. As a rule, higher prices hurt the first group and lower ones hurt the second. But it can be more complicated than that. Indonesia, for example, is a net importer of oil, but a net exporter of “energy”, more broadly defined, including coal and palm oil. Since coal, palm and oil prices tend to rise roughly in tandem, Indonesia would benefit overall from $100 oil, according to UBS. Mexico, like America, is also a net importer of crude. But in both countries a higher oil price will help investment and employment in the oil industry by more than it hurts household spending.

The impact of a price change also depends on the price level. A jump from cheap to dear oil works differently than a jump from dear to even dearer. In America, many rigs that are not profitable at $40 become viable at $60 or more. Conversely, most rigs that would be lucrative at $120 are already viable at $100. So an increase in price from $40 to $60 might inspire a lot of additional investment and employment, whereas an increase from $100 to $120 might induce less. Meanwhile, the damage to household wallets increases relentlessly.

As a consequence, the relationship between oil and growth is not straight but curvy. Prices below $50 and above $75 seem to hurt global prospects, according to calculations by Arend Kapteyn of UBS. In between, they appear to help.

Thus if the oil price remains within its recent range, the global economy should suffer few ill effects. But that is a big if. It is perilous to predict whether the oil price will lurch up or down, safer to predict that it will do one of the two.

The yuan will become more volatile, but also start to rival the dollar

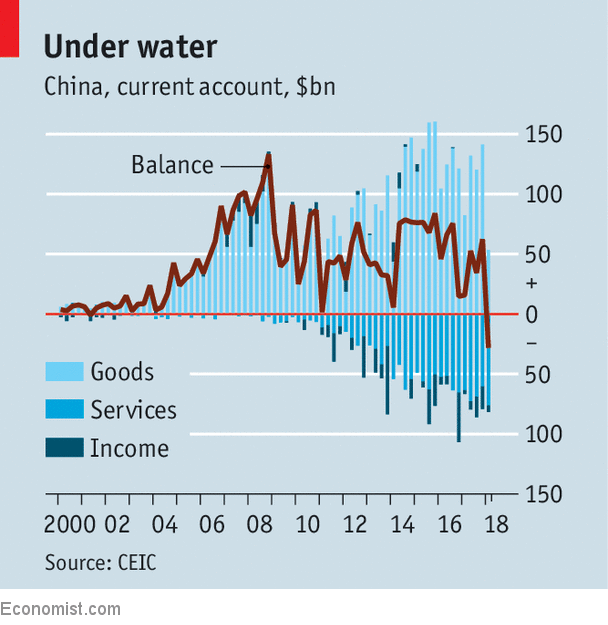

NOT long ago China was a leading culprit in global economic imbalances. Whether blame was ascribed to its undervalued yuan or its frugal people, the problem seemed clear. China was selling a lot abroad and buying too little back. One data-point summed this up: its currentaccount surplus reached 10% of GDP in 2007, well above the level that is generally seen as reasonable. Far less attention has been paid to its steady decline since then. In the first quarter of 2018 China ran a current-account deficit, its first since joining the World Trade Organisation in 2001. Just as its massive surpluses of yore had big consequences for the global economy, so does this swing in the opposite direction.

China still exports many more goods than it imports, to the tune of nearly $500bn annually. But its share of global exports appears to have peaked. At the same time its trade deficit in services is getting bigger, largely thanks to all its tourists venturing abroad (see chart).

At bottom, a current-account balance is the difference between a country’s investment and savings. When China had a big surplus, its savings, at 50% of GDP, far outstripped even its colossal investment. Data on savings are patchy in China. But it is known that investment has declined as a share of GDP. The implication is that the rate of savings has almost certainly declined more sharply, reflecting a big increase in consumption. Its economy is, in other words, better balanced than just a short while ago.

China’s current-account deficit in the first quarter was exaggerated, since exports tend to be subdued at the start of the year. It is likely to return to a surplus in the coming months. But Ding Shuang of Standard Chartered, an emerging-markets bank, forecasts that the surplus will be just 1% of GDP this year and 0.5% next year. The trade ruckus with America could reinforce the downward trend. To placate President Donald Trump, China will try to import more from America and pay more for foreign intellectual property (IP), Mr Ding says.

One probable outcome is that the exchange rate will become more volatile. In recent years capital outflows have pressed down on the yuan, but the current-account surplus has countered that effect. In the future China will have a thinner cushion. Depending on quarterly trade swings, the yuan will be as likely to fall as to rise.

If China’s current-account deficits become more frequent, it will have to run down its foreign assets or borrow more from abroad to pay for its consumption. Should its external liabilities—that is, money it owes the rest of the world—increase rapidly, that might signal greater financial vulnerability. But as long as the increase is moderate, it could actually help China by boosting the yuan’s global profile.

To fund its deficit, China might choose to sell more bonds to foreign investors. And in paying more for goods and services than it earns, it could supply its currency abroad. By itself this would not be enough to make the yuan go global. Investors would need more faith in China’s institutions. But technically, the conditions would be ripe for the yuan’s emergence as a more credible rival to the dollar. America might find itself pining for the days when the Chinese currency was undervalued.

Around this past new year, oil prices were climbing higher and many analysts predicted that a rush of new production from U.S. shale oil fields would, over time, put a damper on prices Nearly six months into 2018, U.S. shale oil production continues to grow, yet it still does not seem to be impacting prices as predicted. This can partially be explained by geopolitical events that have pushed prices up, but it is also a result of some serious and systemic impediments facing the U.S. oil industry.

There is a possibility that each of these impediments could change in coming months. If they do, the U.S. shale production numbers and the price of oil will change as well.

1. Pipeline infrastructure

Pipelines in regions where shale oil is produced are running at around full capacity. This has caused problems for smaller oil producers who have to pay more to transport their oil. In fact, producers who do not have contracts in place for pipeline transportation have been forced to sell their oil at a discount. These types of pipeline constraints have actually plagued the U.S. oil industry for years and have forced companies to ship crude in trucks or by rail, two modes of transportation that are more expensive and more dangerous than pipelines.

Now, it seems this bottleneck may be ending. Several new pipeline deals have been announced and other pipelines are already under construction. It is possible that by the end of 2019 the price to transport U.S. oil will have fallen significantly and greater volumes of U.S. oil will be able to reach the market. This would mean that U.S. producers would be able to sell their product without the current discounts (up to $13 off per barrel for some oil, according to some reports). It would also mean that U.S. oil would reach ports more quickly. Improved pipeline infrastructure could make the entire U.S. oil industry more efficient.

2. Ports

U.S. producers have only been free to export their crude oil since the beginning of 2016 and most ports are not equipped to handle the largest tankers (VLCCs) which carry up to 2 million barrels of oil. Most ports capable of exporting oil can handle ships that carry less than half that amount. Only the Louisiana Offshore Oil Port (LOOP) can accept the VLCC tankers for export at present, though there are plans to dredge other ports, such as Texas' Corpus Christi, if funding can be accessed. The lesser capacity of most U.S. ports is another limitation on the efficiency of the U.S. shale oil industry.

3. Personnel and Supplies

Producers in shale oil regions have faced personnel constraints for months now. Companies are paying a premium for truck drivers, roughnecks, welders and other similar positions. There has also been a shortage of sand which used in fracking, although reports are that new sand mines are in the process of alleviating this constraint. Though we have seen an increase in production of U.S. shale oil, the increase is not as high as it might have been without such constraints.

4. Crude grade

Most important to consider, however, is whether there is a sufficient market for even more U.S. shale oil. The oil produced from fracking is a very light type of oil. U.S. refineries are not designed to process so much light crude. Some mix this crude with heavier grades, but the process is not ideal for the refining needs. Building new refineries is almost impossible in today’s regulatory climate. The U.S. has not built a new refinery since 1977, although two small refineries have been permitted and are under construction in South Dakota and south Texas. (Some refineries have expanded their facilities, such as Motiva in 2012 and Valero (NYSE:VLO) in 2017).

Other markets for light crude appear to be saturated as well, except, apparently, for China. According to an opinion piece by an S&P Global Platts content director, independent Chinese refineries want more of the light crude oil that the U.S. shale oil industry produces.

5. Trade War Risk

As of now, the U.S. has only sent two VLCC tankers to China with U.S. crude, but, as U.S. infrastructure constraints ease, there could be more. On the other hand, the amount of crude Chinese independent refineries can import depends on the will of the Chinese government, which issues import licenses twice a year.

It is entirely possible that U.S. crude oil exports to China could become a pawn in the ongoing trade negotiations between China and the U.S. In that case, politics, not the industry, might determine the size of the market for U.S. oil.

The economy may be chugging along, but many Americans are still struggling to afford a basic middle class life.

Nearly 51 million households don't earn enough to afford a monthly budget that includes housing, food, child care, health care, transportation and a cell phone, according to a study released Thursday by the United Way ALICE Project. That's 43% of households in the United States.

The figure includes the 16.1 million households living in poverty, as well as the 34.7 million families that the United Way has dubbed ALICE -- Asset Limited, Income Constrained, Employed. This group makes less than what's needed "to survive in the modern economy."

"Despite seemingly positive economic signs, the ALICE data shows that financial hardship is still a pervasive problem," said Stephanie Hoopes, the project's director.

California, New Mexico and Hawaii have the largest share of struggling families, at 49% each. North Dakota has the lowest at 32%.

Many of these folks are the nation's child care workers, home health aides, office assistants and store clerks, who work low-paying jobs and have little savings, the study noted. Some 66% of jobs in the US pay less than $20 an hour.

The study also drilled down to the county level.

For instance, in Seattle's King County, the annual household survival budget for a family of four (including one infant and one preschooler) in 2016 was nearly $85,000. This would require an hourly wage of $42.46. But in Washington State, only 14% of jobs pay more than $40 an hour.

Seattle's City Council just passed a controversial tax on big businesses to help alleviate the city's growing homelessness and affordable housing problems.

FEW banks can match the quaint serenity of Banco Delta Asia’s headquarters in Macau. Housed in a pastel-yellow colonial building opposite a 16th-century church, its entrance is flanked by tall vases, depicting sampan gliding between karst hills. In the tiled square outside, men laze under a banyan tree and an elderly woman peels a boiled egg for lunch.

But in 2005 this backwater bank incurred the wrath and might of the world’s financial hegemon. America’s Treasury accused it of laundering money for North Korea, prompting depositors to panic, other banks to keep their distance and the Macau government to step in. The Treasury subsequently barred American financial institutions from holding a correspondent account for the bank, excluding it from the American financial system.

Macau is over 8,000 miles from Washington, DC. But it is hard to escape the long arm of the dollar. Its dominance reflects what economists call network externalities: the more people use it, the more useful it becomes to everyone else. One person’s willingness to accept dollars from another depends on a third person’s readiness to accept dollars from them.

The dollar also benefits from a hub-and-spoke model for the exchange of currencies, the invoicing of trade and the settlement of international payments, as the late Ronald McKinnon of Stanford University argued. If every one of the more than 150 currencies was traded directly against every other, the world would need over 11,175 foreign-exchange markets. If instead each trades against the dollar, it needs only 149 or so. If you cannot buy the afghani with the zloty, you can still sell one for dollars with which to buy the other.

Likewise, if every international bank keeps an account in New York, any bank can transfer funds to any other through the same financial hub. “The global financial system is like a sewer and all of the pipes run through New York,” says Jarrett Blanc of the Carnegie Endowment for International Peace.

This gives America’s Treasury great punitive power and jurisdictional reach. Many companies that do not buy or sell wares in America nonetheless make or collect payment through New York. Because these transfers pass through American financial institutions, the Treasury can claim jurisdiction on the ground that its banks are exporting financial services to the bad guy. It can also hit companies where it hurts. For many, exclusion from America’s financial system is a more potent threat than exclusion from America’s customers. Last month, for example, the Treasury threatened to seize dollars paid to Rusal, a Russian metals firm that is one of the world’s biggest aluminium producers, crippling it and upending the global aluminium market, until the turmoil forced a rethink.

The Rusal debacle and President Donald Trump’s decision to withdraw from the Iran nuclear deal have raised fears that America might abuse its power. That may prompt foreign governments and financial institutions to think about rerouting the sewer.

Not all dollar settlements are subject to American jurisdiction. It is, for example, possible to clear large dollar payments in Tokyo, Hong Kong and elsewhere. But the pipes are narrow. America’s two big payments systems, Fedwire and CHIPS, handled transactions worth $4.5trn a day in 2017. Hong Kong’s system (which runs through HSBC, a private bank) dealt with only 0.8% of that amount. Moreover, the ability of offshore dollars to enter and leave the American financial system if necessary is vital to their appeal. The liquidity of Hong Kong’s system, for example, is buttressed by HSBC’s ability to handle dollars in New York.

China is nurturing its own international payments system, based on its own currency. It might ask Iran to accept the yuan in exchange for its oil. Certainly, America’s withdrawal from the Iran deal has increased trading in the yuan-denominated oil futures contract that China recently launched in Shanghai. Likewise, Russia and China are increasingly paying each other for goods in their own currencies, rather than America’s. Russia paid for 15% of its Chinese imports with yuan last year, according to Russia’s central bank (as cited by Russia Today, a broadcaster).

China’s capital controls and Europe’s fiscal balkanisation weaken their currencies’ claims to rival the dollar. But since China’s economy seems destined to overtake America’s, it would be strange if its currency forever lagged far behind. And although neither economic bloc is yet ready to match America’s position in the financial system, they might be able to build a set of financial pipes big enough to sustain trade with blacklisted Russian companies or a country like Iran. Previous treasury secretaries took the danger seriously. “The more we condition use of the dollar and our financial system on adherence to US foreign policy, the more the risk of migration to other currencies and other financial systems in the medium term grows,” said Jacob Lew in 2016.

Closing the sluice gate

Steering clear of American jurisdiction is not quite the same as escaping American power. Even if no payments cross American territory, America could still impose extraterritorial or “secondary” sanctions, refusing to do business with a company that does business with a blacklisted party. To blunt that threat, foreign governments would then have to foster banks, suppliers and customers that can live entirely without America.

Banco Delta Asia, for its part, has survived America’s onslaught, with the help of Macau’s government. It has yet to convince the Treasury to lift the ruling that stops it gaining access to America’s financial system. But it is not completely cut off from the dollar. At one of its bigger branches, your correspondent was able to sell 820 patacas for a crisp $100 note, bearing the signature of a former secretary of the Treasury.

It is giving new opportunities to entrepreneurs and forcing Silicon Valley's best to stay relevant.

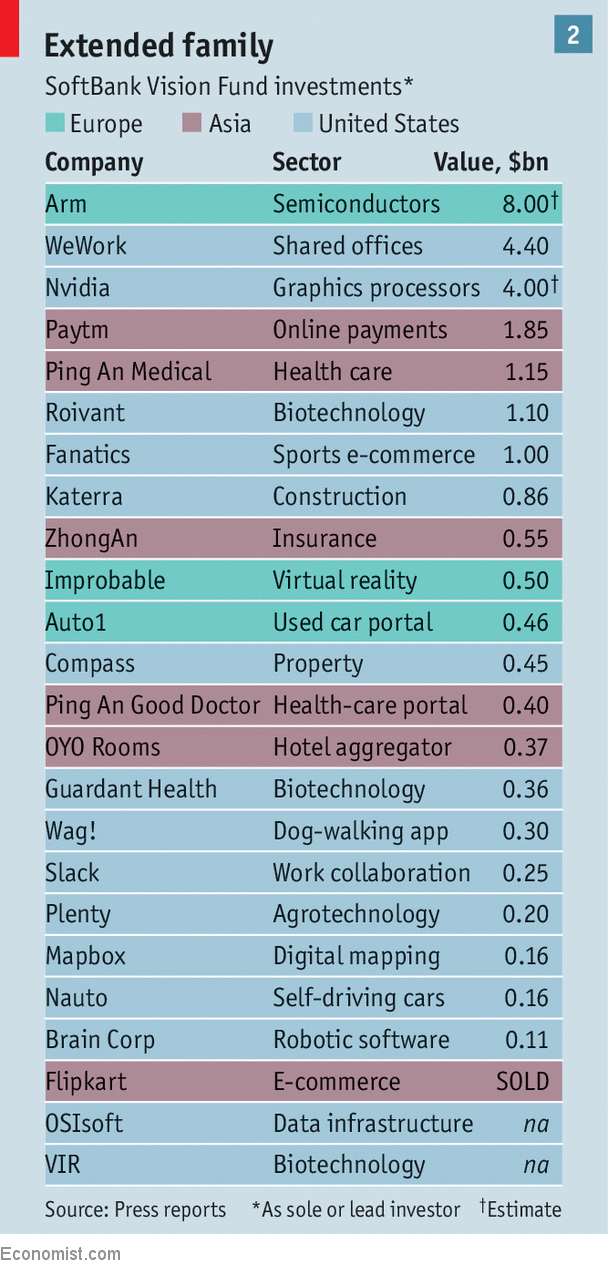

HERMAN NARULA named his company Improbable for a business plan so outlandish and fraught with computing problems that only two outcomes are plausible. As the British entrepreneur tells it, the result will be outright failure or success unmatched. He wants to create virtual worlds as detailed, immersive and persistent as reality, where millions of people can live as their true selves, earn their main income and interact with artificially intelligent robots. If that happens, it will be partly because Mr Narula drew the attention of a similarly improbable, wildly ambitious technology fund. The Vision Fund has put close to $500m into Improbable, which had previously raised only $52m.

An outsize investment in an unconventional business is typical of a fund that itself is both vast and resistant to definition. It is the brainchild of Masayoshi Son, an unusually risk-loving Japanese telecoms and internet entrepreneur. It is too big to be considered a conventional venture-capital firm, which would typically manage much smaller sums. It eschews many of the practices of private-equity funds, such as shaking up management and applying plenty of debt. Yet this impressive-but-puzzling experiment is having an impact on everyone who invests in technology. At a recent gathering of financiers in New York, Bill Gurley of Benchmark, a venture-capital firm that has invested in numerous well-known tech firms, called the Vision Fund “the most powerful investor in our world”.

Even amid the hyperbole and fervour of tech Mr Son stands out. This is partly because of his belief in mind-boggling futuristic scenarios such as the “singularity”, when computer intelligence is meant to overtake the human kind. But it is also because Mr Son’s method is to do things rapidly and on a scale other investors would shy away from. Whether backing founders lavishly, so they can roll out new business models and technology as quickly as possible, or encouraging consolidation among the world’s giant ride-hailing companies, including Uber and Singapore’s Grab, he thinks bigger than most.

Silicon Valley insiders are sceptical, saying that Mr Son is force-feeding young firms with more capital than they deserve or need and that his fund will further inflate a bubble in technology valuations. His investors may well discover how hard it is to earn high returns on huge sums invested in relatively mature firms. But entrepreneurs, some of whom regard Mr Son as superhuman, are delighted. “If he came in and levitated one day I would not be surprised,” says Mike Cagney, co-founder of SoFi, an American financial-technology company in which Mr Son has invested.

Those doubting his grand visions have been proved wrong in the past. In 1981 he founded SoftBank to distribute personal-computer software in Tokyo with two part-time employees. On the first day the diminutive Mr Son stood on two apple cartons and announced to those befuddled workers that in five years the firm would have $75m in sales and be number one. They thought “this guy must be crazy”, Mr Son later told the Harvard Business Review, and quit the same day. But Mr Son’s drive and ambition saw SoftBank eventually distributing 80% of PC software in Japan.

Rising Son

SoftBank subsequently grew into a global conglomerate with stakes in hundreds of web firms, including Yahoo. As tech valuations soared in 2000 Mr Son’s personal wealth even briefly overtook that of Bill Gates. The dotcom crash of 2001 wiped out 99% of SoftBank’s market value. But one investment—$20m sunk into Alibaba—is regarded as one of the best in history. The Chinese internet titan went public in 2014 in the world’s biggest IPO. SoftBank’s 28% stake in the firm is now worth $140bn.

Many old hands of the tech industry snootily dismiss his bets on Yahoo and Alibaba as flukes. Mr Son is bent on proving them wrong. He spent a decade focusing on SoftBank’s Japanese telecoms and internet-infrastructure businesses and on trying to turn around struggling Sprint, an American mobile-phone operator acquired in 2013 (on April 29th Mr Son beat a retreat, agreeing to merge it with T-Mobile to create an enterprise worth $146bn). Now Mr Son has returned to investing. Since reaping the riches of Alibaba’s IPO Mr Son has been using SoftBank’s capital for a series of large tech investments, including $2.5bn in Flipkart, an Indian e-commerce site which on May 9th Mr Son said he was selling to Walmart for $4bn (see article). He has also put money into Grab and SoFi. And in 2016 SoftBank bought Arm Holdings, a British chip firm, for £24.3bn ($31.9bn).

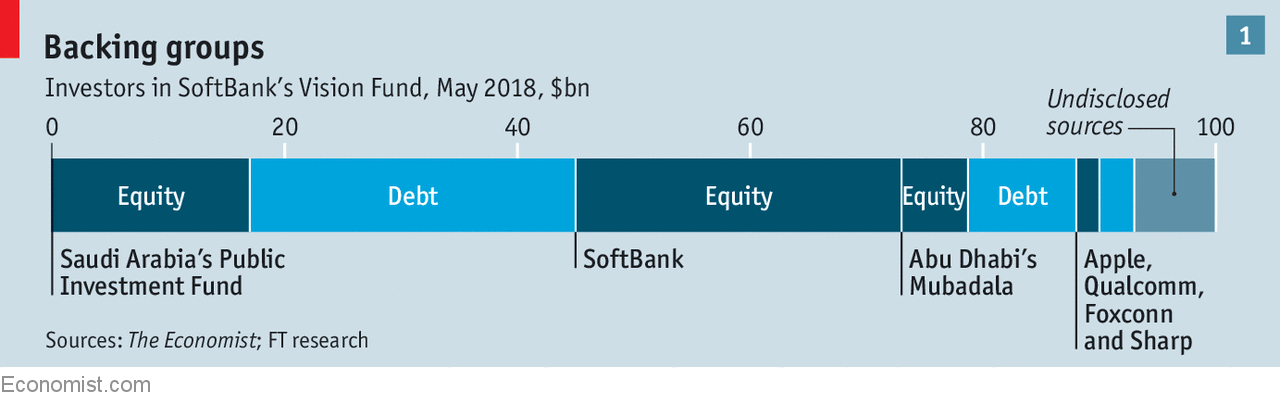

The appetite of Mr Son and his main lieutenant, Rajeev Misra, a well-connected former derivatives trader from Deutsche Bank, was far from sated. But Mr Son’s grand dreams were not matched by the depth of SoftBank’s pockets. Its acquisitions had left the firm weighed down by debt. So the two men beat a path to the Middle East. The timing was handy. Muhammad bin Salman, now Saudi Arabia’s crown prince, was preparing to launch a programme to wean the country off oil and diversify the economy. Mr Son’s sales pitch on how he could use the kingdom’s wealth to grab a stake in future technologies, rather than buying the usual Western trophy assets, saw him leave with a pledge of $45bn.

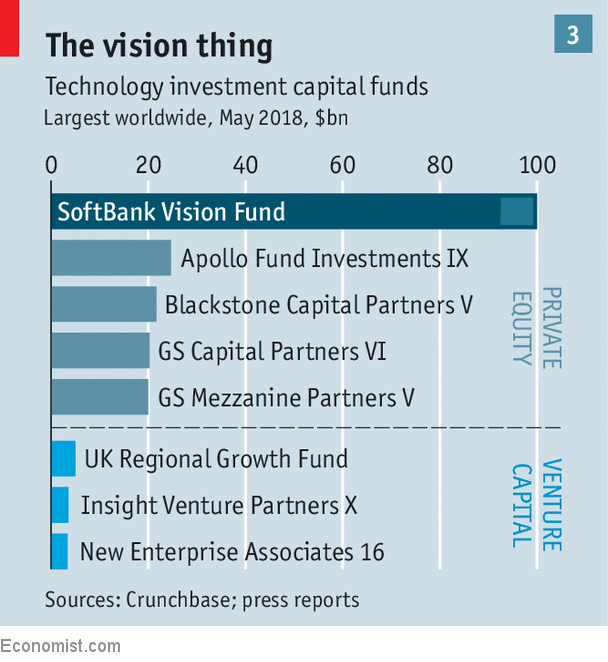

That vast sum, from Saudi Arabia’s Public Investment Fund, is the biggest chunk of the $100bn that the Vision Fund has now raised. It has also raised $28bn from SoftBank itself, $15bn from Mubadala, Abu Dhabi’s sovereign-wealth fund, $5bn from Apple and other corporate sources, and $7bn from other sources as yet unnamed (see chart 1).

Raising the stakes

Having amassed the wherewithal, Mr Son set about collecting stakes. After a year the Vision Fund boasts a family of 24 companies (see chart 2). SoftBank’s holdings in ride-sharing firms—Uber, Didi, Grab and Ola—will reportedly move into the fund within months. Other stakes are expected to move later, such as those in SoFi and OneWeb. All future investments of $100m or more that Mr Son makes will go into the Vision Fund, which plans to have invested in as many as 100 firms within five years.

Its sheer size has transfixed potential investment targets and rival funds alike. The $30bn it has already invested nearly equals the $33bn that the American venture-capital industry raised in 2017. It will not stop there. If the fund performs well, versions two, three and four could be in the offing, says Mr Son.

In some ways the Vision Fund operates like any other technology fund. It has welcomed pitches from a couple of hundred hopeful young companies. Founders visit its offices in San Carlos in San Francisco’s Bay Area or its opulent town house in London’s Mayfair, in both places greeted at the door by Pepper, a cheery robot made by SoftBank’s robotics arm. Less than 5% of the entrepreneurs who seek funding receive it, which is slightly more generous than most VC firms. When Mr Son has chosen his targets, he believes in the power of capital and the potential for synergies between his firms to help reap rewards.

The recipients of cash fall into three main areas. First there is the “frontier”—bets backing Mr Son’s instincts about revolutionary technologies in areas such as the internet of things, robotics, artificial intelligence (AI), computational biology and genomics. The internet of things was his rationale for the purchase of Arm, which Mr Son says can design the chips to enable what he believes will be a trillion connected devices by 2035. NVIDIA, another chip-design firm in which SoftBank recently bought a big stake, will provide processors for AI services. SoftBank’s interest in an American 5G network (via Sprint’s tie-up with T-Mobile) and in OneWeb, a satellite startup, will help with the connections.

Second comes investments designed to bring new tech to old industries such as transport, property and logistics. Ride-hailing falls into this category (see article). And the third area is technology, media and telecoms, where SoftBank has been investing for nearly 25 years. Its stakes here stretch from Fanatics, an online sports-merchandise retailer, to Wag!, an on-demand dog-walking service.

But alongside the futuristic vision runs a hard-nosed, opportunistic appreciation of the power of capital to create winners. Mr Son recently said that, if Steve Jobs brought to Apple an understanding of technology and art, his own formula is technology plus finance. Time and again he has cajoled and bullied founders and chief executives into accepting his money, often handing out much more than they were asking for.

Fundraising pitches are atypical of the tech world. A videoconference call to Tokyo with an awkward audio delay makes for stilted dialogue. After ten minutes Mr Son often interrupts, as one founder tells it: “Stop, I know. I’ve heard enough, how much do you want?” He then offers up to four or five times what the entrepreneur suggests. Any questions over what the firm would do with that much money and Mr Son threatens to put the cash into a rival, usually leading to capitulation. During talks with Uber, he threatened to invest in Lyft. SoFi, Didi, Grab and Brain Corp, which builds machine brains for robots, all got variations of the treatment.

Money is not the only thing that the fund offers; so is the privilege of joining the “family”. Once the Vision Fund has invested in 70-100 or so companies, it will have the world’s biggest collection of young tech firms. They will create an ecosystem where they will be each other’s customers, will merge with each other, and swap help and advice, says Mr Misra.

The idea is that such ties will help firms grow more quickly. Mr Son is intent on taking American and European startups into Asia, and vice versa, and Asian ones into nearby countries. SoftBank will act as a guide—its network in Japan, for example, is a boon to Slack, a messaging company in which it has a sizeable stake, as it expands there. SoftBank sometimes makes it a condition of investing in a young Western firm that it must enter a joint venture in Asia.

OYO Rooms, an Indian startup that overhauls and brands small, local hotels, provides another example of collaboration. It is preparing to enter Europe and is moving into China, where Mr Son’s connection to Alibaba and other firms has helped, says Ritesh Agarwal, its founder. In Shenzhen, now one of OYO’s big markets, it ran a joint ad campaign with Didi with the tagline “ride comfortably with Didi, stay comfortably with OYO”.

Mentoring is also sold as a benefit of clan membership. Executives from Grab and Ola often visit Didi to learn from its mistakes, says Mr Misra. “As the number of portfolio companies increases, the possibilities for synergies will be unlimited,” says Mr Son. “The Vision Fund is a platform where portfolio companies can stimulate and collaborate with one another.”

When the bill comes due

Mr Son’s pitch does not convince everyone. Analysts have marked down SoftBank’s shares in large part because they fear Mr Son’s big bets on the future, notes Chris Lane of Bernstein, an equity-research firm. In recent years SoftBank has traded at a 30% discount to the value of its assets, which include its holding in Alibaba. This gap has widened lately.

Some wagers in particular raise eyebrows. His investments in ride-hailing firms attract criticism because their business models are easy to copy, and because his injection of cash may, in the short-term, encourage them to burn even more of the stuff battling each other. Putting $4.4bn into WeWork, a provider of shared workspaces, valuing it at $20bn, is another risky bet. The firm leases office space, redesigns it to create a hip vibe and sublets it to startups, freelancers and some big firms. The worry is that WeWork is little more than a commercial-property company that is unjustifiably trading on a tech valuation and will soon be rumbled.

SoftBank’s shareholders are firmly on the hook when it comes to the Vision Fund. It is the only investor to contribute nothing but equity and would lose its $28bn first if the fund falls steeply in value. Of the money contributed by known outsiders, just over 60% is in the form of debt, which will receive a 7% coupon, to be paid every six months. According to people familiar with the fund, it will move in and out of investments but it will always keep a buffer of around $20bn to make follow-on investments in existing portfolio firms and to pay the coupon each six months. (That cushion underlines that the headline figure of $100bn is partly a marketing strategy.) The flipside of this structure is that SoftBank’s returns from the Vision Fund are leveraged, because it holds only equity, so it would profit handsomely if things go well. It also gets an annual management fee and a performance bonus if the fund surpasses expectations. A rough estimate is that if the underlying investments return only 1% a year for the fund’s life of 12 years, SoftBank’s annual internal rate of return (IRR) would be -4%, whereas if they returned 20% a year, the annual IRR would be 27%.

What, then, would count as success after the fund has run its course? Mr Son has repeatedly said that even without Alibaba, his investments have produced a remarkably high IRR of 42% (with Alibaba included, it rises to 44%). But IRR is a fuzzy concept with no standard measure and can be manipulated. The discrepancy between the figure of 42% and the poor relative performance of SoftBank shares may be more telling.

It seems certain that the Vision Fund is aiming high. But the bigger a fund is, the harder it is to make high returns. Success in venture capital in particular is based on the idea of making a range of bets with returns that are likely to diverge sharply. Out of a portfolio of, say, 50 investments, the chances are that 20 will fail and 20 might produce a middling return. The real money comes from the few that generate an extraordinary windfall, such as Accel achieved with its early investment in Facebook or Sequoia with Google.

Achieving such a distribution is harder when investing huge sums, in the range of $100m to $5bn. In the case of a $5bn investment, it would not be enough for the Vision Fund to exit even at $50bn; it would need an exit at $100bn or more, and such outcomes are extremely rare. Perhaps, as the portfolio is tilted heavily towards later-stage investments in more tried-and-tested businesses, the answer is that there will be fewer failures, so big wins are not as essential. But the Vision Fund has lots of early-stage bets too, such as Improbable or Plenty, an indoor-farming startup. It may require a firm such as Uber, Didi or Arm to end up worth over $500bn for the fund to meet Mr Son’s definition of success.

The complexity of the relationship between the Vision Fund and SoftBank is another potential vulnerability. Despite a strong alignment of interest, the two sets of shareholders might disagree about which firms should go where. Or Mr Son might spread himself too thin. He seldom sees anything but upside, says a person close to him. That may make him unrealistic about the need for him to stay closely involved in all the Vision Fund’s investments. He is probably the only one who fully understands the jigsaw puzzle of AI, satellites, data and so on that it comprises.

Mr Son will also run up against limits on his ability to influence founders and find synergies. The fund’s stakes are usually below 30%, so it has few formal levers to force chief executives into deals or alliances they find unappetising. And where he presses for long-term growth and advances in frontier technologies, other investors may prefer near-term profits.

Unaugmented reality

Even success would have its complications. As some firms get bigger and more dominant, regulators are casting a warier eye. In ride-hailing, the most high-profile part of the portfolio, antitrust watchdogs are stirring. It was a shock to regulators in Singapore, Vietnam and the Philippines when, after Grab merged with Uber, the latter prepared to wind down, leaving Grab as the monopoly operator. Competition reviews have begun in all three places.

Mr Son’s connections in China may also be double-edged. They could benefit firms looking to enter the local market. But amid rising nervousness in Washington, DC, about China’s clout in tech, they are also attracting attention from America’s powerful Committee on Foreign Investment in the United States. Its pending review of SoftBank’s acquisition of its stake in Uber, for example, means that Mr Misra has yet to take his seat on the firm’s board.

As for the Vision Fund’s broader impact on startups, the most controversial question is whether stuffing balance-sheets with too much capital encourages indiscipline. Startups perish more often from indigestion than starvation, runs a Silicon Valley saying. Too much money can create unrealistic expectations and lead to waste, inefficiency and sloppiness. Mr Gurley, who has long warned about a bubble, notes that the cash-burn rate of the top 200 private tech firms is now probably five times faster than in 1999, and the Vision Fund is adding to the risk.

Mr Son’s broad aim in giving out such massive cheques is to ensure that founders can focus on their businesses rather than spending time preparing for their next funding round. “Too much money has a bad effect,” he says, “but turbocharging the firms that have a great formula stimulates founders’ thinking and gives them stamina.” It seems clear, however, that smaller firms, once they get the money, are elevated above their rivals. Having lots of capital is in itself a shield against competitors. Patricia Nakache of Trinity Ventures, has dubbed Vision Fund companies “untouchable” or “super haves”.

Some founders do say “no”. One such was David Rosenberg, who set up AeroFarms, an indoor vertical-farming startup, in upstate New York in 2004. The firm is well-established and operates nine indoor farms (the most recent is the world’s largest) using its patented aeroponic system to grow many different types of leafy greens and herbs. When Mr Rosenberg found out the Vision Fund’s minimum cheque size was $100m, he turned it down. “I did not think at the time that we could spend that money in a responsible way,” he says.

Such self-denial is rare, and the wider effects of such massive sums are already being felt. The Vision Fund intensifies an existing trend for ever-greater wads of money to pour into startups, pumping up valuations. That in turn reinforces a tendency for highly valued private companies to shun the public markets for longer. Some founders now even speak of “doing an IPO to the SoftBank market”.

It also brings disruption to those who have themselves mercilessly backed upstarts in established industries (see chart 3). The fund’s reach and heft has stoked intense jealousy among American private-equity and venture-capital bosses, notes one New York-based financier close to Mr Son. The next three biggest growth funds of venture-capital firms add up to a mere $12bn, and all but the biggest are now often priced out of later-stage funding rounds.

In response, investment firms in Silicon Valley are attempting to up the ante—Sequoia, for example, is raising a new $8bn global growth fund. Some of them have taken to warning startups against accepting funding from Saudi Arabia which, despite its new and more liberal instincts, is still a deeply repressive country. But few entrepreneurs will turn down the largesse. As one quips, not all money can come from the blue-chip Rockefeller Foundation.

As a result the fund is swinging the tech pendulum a little away from Silicon Valley. Money is gushing from farther-flung places. Only around a third of the Vision Fund’s cash comes from American, Japanese and Taiwanese firms; 60% hails from Saudi Arabi and Abu Dhabi. And its money is also flowing to places where capital is in shorter supply. The beneficiary should be Europe, which has struggled to attract the sums that routinely get invested in startups in America and China.

The risks, however, are huge. Determined to invest in indoor farming, but unable to back AeroFarms, Mr Son last year put $200m in Plenty, which was founded in 2014. The firm has not yet started selling produce to customers; it plans to do so in San Francisco very shortly. Its founder, Matt Barnard, a Steinbeckian character who grew up on a cherry-and-apple farm in Wisconsin, reckons that indoor farming could help the global fruit-and-vegetable industry quintuple from $500bn today to $2.5trn. Without having sold a single lettuce, Plenty is planning expansion into China and Japan. Like the Vision Fund itself, such a firm will either fail dramatically or succeed beyond all expectations—regardless, it will happen on a grand scale.

Regardless of the underlying specifics of cryptocurrency technology, whether it's Bitcoin, Ethereum, Ripple, Cardano or EOS for example, all digital currencies are essentially borderless. They can be mined just about anywhere and generally, traded globally.

Still, not every location is as friendly to the burgeoning asset class as others. Some countries offer tax friendly considerations for crypto businesses while others have relatively easy regulations. Some are encouraging digital cash as an alternative to fiat money and some are even contemplating launching their own alt-currencies. Some countries have a variety of initiatives in play to foster cryptocurrency business and blockchain innovation.

Below are seven locations setting up systems that are cryptocurrency friendly. We're not advocating for any of them, nor in at least one case would we want to. But the level of effort these regional hubs are expending is worth attention. It's conceivable the next breakthrough in this sector could come from entrepreneurial activity in one of these locations.

1. Japan

Among Asian countries, Japan appears to have taken the lead in supporting cryptocurrencies. It's certainly way out ahead of its more restrictionist neighbor China which cracked down on both ICOs and exchange trading during the last few years.

Since the pseudonymous Satoshi Nakamoto is the name attributed the unknown person (or persons?) who developed Bitcoin, perhaps it makes sense that Japan would be at the forefront of cyrpto-friendly environments.

After the hack-plagued, Japan-based Mt. Gox exchange finally collapsed in February 2014—to date still the biggest cryptocurrency exchange scandal for the asset class—Japan’s licensed cryptocurrency exchanges gathered to form a new, self-regulatory organization which would propose guidelines for legalizing initial coin offerings (ICOs) and formulate clear industry standards in order to protect investors but also allow the industry to grow and innovate. The working association, called the ICO Business Research Group, includes lawmakers, academics, bankers and the CEO of bitFlyer, the country's largest cryptocurrency exchange. According to government research, legislation would allow potentially lucrative ICOs and crypto exchanges to continue trading while at the same time providing the government with greater insight and transparency into these activities.

2. Venezuela

The oil-rich but severely debt-ridden South American nation stirred up controversy, and much derision, when it launched its own digital currency, the oil-backed Petro which Venezuela reportedly launched in February. According to CNN, the country's president, Nicolas Maduro, has "claimed that the token—which runs on the NEMblockchain and is allegedly backed by barrels of oil—raised more than $5B during the first month of its token sale, though the prevailing sentiment among analysts is that the claim is patently false."

Still, at the end of April, news broke that Venezuela had offered India a discount on crude oil purchases of 30-percent if they pay in Petro. Bitcoin magazine reports that "Venezuela has guaranteed buyers that the Petro will carry the full weight of legal tender, acceptable as payment for fees and taxes and exchangeable for the nation's hard currency, the bolivar.

Though many are skeptical of the Petro itself, and equally of the Venezuelan government's supposed efforts to integrate the cryptocurrency into its failing economy, there are some who see merit in the effort to gain credibility for any cryptocurrency. David Garcia, managing director, SVP and partner at Ripio Credit Network, notes that Latin America is going through a transition period.

The region has suffered quite a bit due to political corruption, economic crises, and is plagued by high inflation and rapid currency devaluation. This is particularly true of Venezuela right now but could also characterize other LatAm locations. It's Garcia's view that in order to move these countries in a positive direction, innovative ideas and solutions—such as blockchain and cryptocurrencies—are a necessary solution.

3. Sweden

Sweden was the first country to authorize trading of two Bitcoin exchange traded notes (ETN) in Europe in 2015, managed by XBT Providers. The funds, Bitcoin Tracker One XBT (ST:SE0007126024) which trades in Swedish krona and Bitcoin Tracker EUR XBT Provider (ST:SE0007525332), both trade on the Nordic NASDAQ, a major Swedish exchange.

Since their launch XBT has issued versions in Denmark, Finland, Estonia and Latvia. As of early December 2017, Cointelegraph declared the Swedish ETNs to be "bigger than 80% of US ETFs." In mid-January CNBC noted that Swedish Bitcoin investments had attracted $1.3 billion in funds.

Additionally, Sweden's central bank, the Riksbank, has been considering creating an electronic currency, dubbed the e-krona, in response to the fact that Sweden is rapidly become the world's first cashless society. However, the country's banking sector is pushing back. Hans Lindberg, chief executive officer of the Swedish Bankers' Association said, during an interview on April 17, "when it comes to electronic money, there's already plenty. There are bank cards, credit cards...and other electronic solutions. The best option also going forward is probably that the Riksbank sticks to wholesale."

Nevertheless, HSBC global economist James Pomeroy believes it's still possible Sweden will be the first country in the world to issue an electronic currency, which could launch within the next few years. Venezuela may have gotten out ahead on a government backed crypto launch, but the Scandinavian country, with its stronger economy and more trusted regulatory bodies could still disrupt the asset class on this front, even as it continues to lead the European crypto sector.

4. Switzerland

Switzerland’s Financial Market Supervisory Authority (FINMA) is at the forefront when it comes to clarity surrounding crypto regulation and support for initial coin offerings (ICOs). Marc Bernegger, a Switzerland-based fin-tech expert, cryptocurrency entrepreneur and advisor at SwissRealCoin says that traditionally, the country has been a haven for wealth. This is, in part, is due to more open financial regulations and an abiding culture that drives the privacy of those that use Swiss banking institutions. Bernegger notes that Switzerland has been “forward-thinking" about crypto assests as part of overall wealth management, and is "preparing for the changing economy.”

The area around the city of Zug in north-central Switzerland has become known as is called "Crypto Valley," ever since the Ethereum ICO took place there in 2014. The surrounding region hosts one of the most active ecosystems for crypto entrepreneurs, developers and investors, explains Antoine Verdon, co-founder of Proxeus, a blockchain integrator.

“In January, the Swiss Minister of the Economy declared his ambition to make Switzerland a "Crypto Nation" and the already active ecosystem is now growing past its former base, with several companies and public administrations all over the country running proof-of-concept projects, and the recent the opening of a co-working space in Zurich dedicated exclusively to blockchain projects.”

5. Israel

Regulatory talks with a focus on cryptocurrencies continue in Israel as lawmakers look for ways to protect investors. Though the Israeli banking system hasn't helped foster Bitcoin-related business—Union Bank of Israel, the country's sixth largest bank is being sued by a local cryptocurrency miner after the bank halted fund transfers from Bitcoin exchanges to the miner; Bank Leumi, the country's second largest lender tried to stop the account activity of a local exchange—district courts as well as the country's Supreme Court have intervened. That's surely a major victory for the local cryptocurrency industry.

As well, recent reports indicate that the country's central bank, the Bank of Israel, has, for several months been looking at the possibility of a state-sponsored currency. According to the Jerusalem Post, " the digital shekel would record every transaction by mobile phone and make it more difficult to evade taxation," according to an anonymous source. The digital shekel, if and when it were to launch, would be identical in value to the physical shekel.

On the tech innovation front, Israel's start-up culture is ahead of the curve. Roy Meirom co-founder and VP of Business Development at WeMark points out that blockchain implementation is highly sought after by many of the approximately 300 multinational R&D centers operating in Israel.

He says the small Middle Eastern country, often referred to as the “Startup Nation,” is rapidly becoming a hub for blockchain-related development.

“Scientists and engineers in the workforce, many of whom are graduates of the nation’s elite military intelligence forces, have transitioned to support this staggering demand, complimented by an ever-growing number of blockchain startups and a supportive ecosystem.”

6. Bermuda

Bermuda, the tiny, Caribbean British Commonwealth located in the North Atlantic, has been showing active interest in passing cryptocurrency regulation in order to begin building an appropriate framework for fostering cryptocurrency business including exchanges, wallet services and payment providers. Recently, the Bermuda Monetary Authority's Virtual Currency Business Act (VCBA) passed through the House of Commons in the UK.

Bermuda has proposed ICO legislation which will take the form of amendments to the country's Companies Act 1981 and Limited Liability Company Act 2016. Late last year, Bermuda’s Premier and Finance Minister, David Burt launched a Blockchain task force, broken into two groups, the Blockchain Legal and Regulatory Working Group and the Blockchain Business Working Group.

7. Germany

Germany's capital, Berlin, is perhaps one of the most crypto-friendly cities in the European Union. It was dubbed the Bitcoin Capital of Europe in 2013 by the UK's Guardian, and it continues to own that position. Currently one can buy an apartment in the city, book holidays, eat and drink in a variety of trendy local eateries using Bitcoin.

Thomas Schouten, Marketing Lead for Lisk, the blockchain application platform, says Lisk, has key contractor offices in Berlin with headquarters in Switzerland. Berlin offers a vibrant startup and tech scene, with a large talent pool and a dynamic culture, he says, which makes it easy to attract staffing. Plus, he explains, Germans, as well as their government, have an open-minded approach toward blockchain technology.

This is highlighted by the fact that it was the first country to accept Bitcoin as a currency, having done so in 2014. Similarly, board members of Germany’s central bank, the Deutsche Bundesbank, have called for effective and appropriate regulation of cryptocurrency and token markets. Indeed, Joachim Wuermeling, one of its directors has spoken out about the need for international cooperation on the issue:

Effective regulation of virtual currencies would therefore only be achievable through the greatest possible international cooperation, because the regulatory power of nation states is obviously limited.

To that end, a variety of German central bank decision makers have been involved in EU wide discussion on ways to boost the sector across the region, including via the European Blockchain Partnership.