Peak profits

Big listed firms’ earnings have hit a wall of deflation and stagnation

THE idea that profits grow is embedded in the corporate world. Bosses’ pay rises if they boost earnings per share. Managers who admit their firms may shrink are viewed as cowards and taken outside and shot. Lenders assume that firms’ cashflows will grow, allowing them to repay debts. In a daft ritual, Wall Street analysts start most years by collectively forecasting that earnings per share will rise at double-digit rates. Actual growth has been lower but has still had a dazzling run, averaging 8% over the past 30 years for the S&P 500 index of big American firms. Even after the 2007-08 crisis floored the global economy, profits recovered smartly.

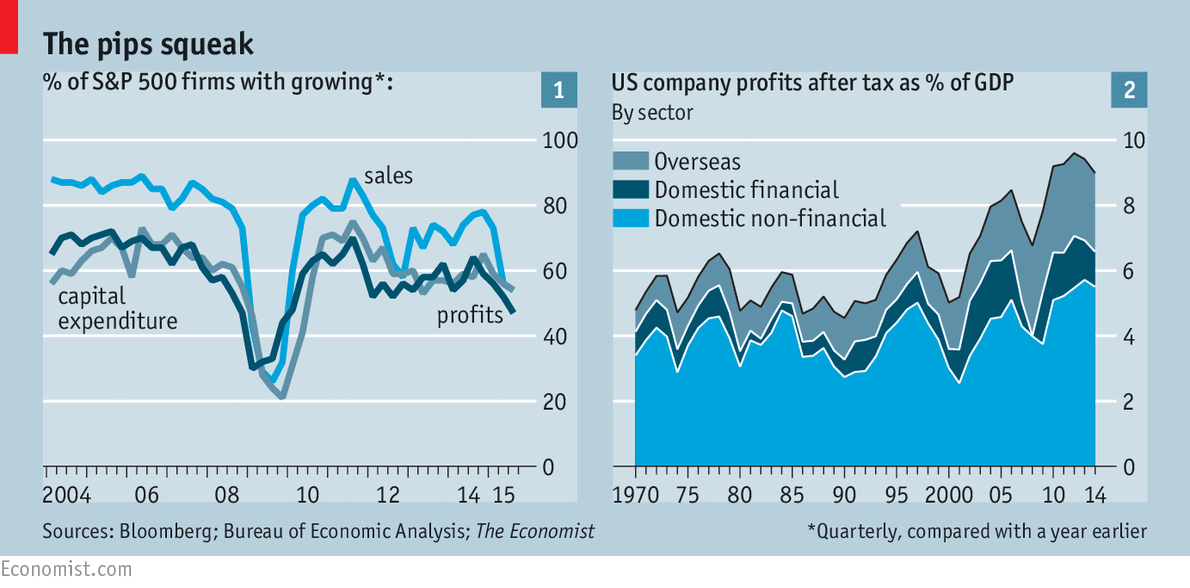

Perhaps that is why reality has yet to sink in: the business world is stagnating. For the second quarter in a row the sales and profits of members of the S&P 500 are expected to fall; for the three months to September they are forecast to be 3-5% lower than in the same period last year. Earnings recessions are rare, happening only about once in each decade.

The Panglossian response this time is to blame one-off factors, in this case low energy prices and a strong dollar. The latter crimps the value of foreign income once it is translated into greenbacks.

Alas, corporate sloth is a far deeper and more widespread problem than that. Consider that half of big listed American firms now have shrinking profits (see chart 1). Even excluding energy and the dollar, S&P 500 earnings growth is slow. Many bellwethers—Walmart, IBM, General Electric (GE)—face flat or declining top lines. While traditional industries, from hotels to television, grumble that technology firms are eating their lunch, even the tech industry’s earnings are flat, with the likes of Alphabet (formerly known as Google) approaching middle age. Sluggishness is everywhere. Worldwide earnings per share have stopped growing, measured in dollars. In local-currency terms sales growth has stalled in Asia, slowed in Europe and is expected to collapse in Brazil. On October 16th Nestlé, Europe’s second-most-valuable firm, said it would miss its long-standing sales target this year.

At the economy-wide level companies’ sales are closely related to nominal GDP growth (which includes inflation). So it should be no shock that firms are struggling given that deflation stalks rich countries and growth is slowing in the emerging world. After two lost decades, Japanese firms’ sales per share are still similar to the level in the 1990s. For Western firms there is also a suspicion that the methods used to crank out profits during the golden era were unsustainable. The unease is compounded by the fact that earnings are high relative to two yardsticks. S&P 500 earnings per share are 28% above their ten-year average. And in America profits are stretched relative to GDP (see chart 2).

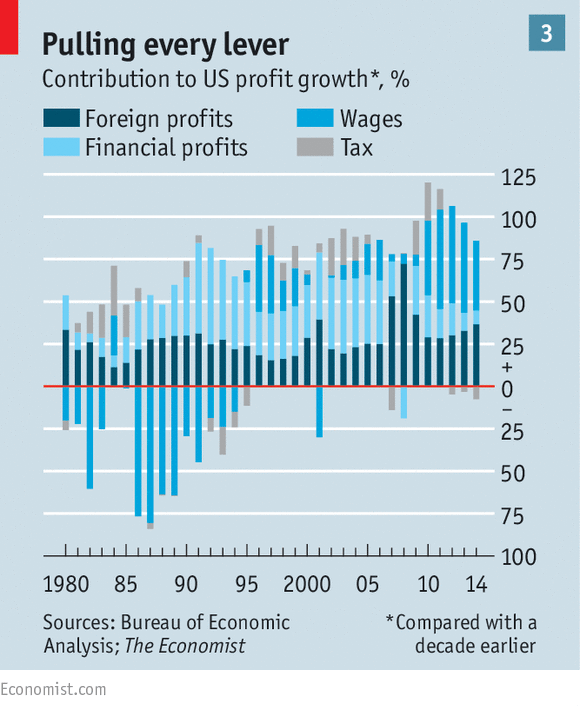

Since the 1970s American firms have yanked on three big levers to boost profits. First, multinationals expanded abroad, with foreign earnings supplying a third or so of long-term earnings growth. Today, however, it seems that emerging economies are at the end of their 15-year boom. Second, finance was a crucial prop for profits in the two decades to 2007 (see chart 3), with the banking industry expanding rapidly and industrial firms such as GE and General Motors building huge shadow banks. The regulatory clampdown since the financial crisis means this adventure is now over.

Third, after 2007-08 firms relied heavily on pushing down the share of their profits that they paid out in wages. But now there are hints that wages are rising. On October 14th Walmart said that higher pay and training costs would lower its profits by $1.5 billion, or just under 10%, in 2017. A week later Chipotle, a fast-food chain specialising in burritos big enough to ballast a ship, blamed falling margins on labour costs. If the share of domestic gross earnings paid in wages were to rise back to the average level of the 1990s, the profits of American firms would drop by a fifth.

Faced with stagnation, the quick fix is share buy-backs, which are running at $600 billion a year in America. They are a legitimate way to return cash to investors but also artificially boost earnings per share. IBM spent $121 billion on buy-backs over the past decade, twice what it forked out on research and development. In the third quarter its sales fell by 14%, or by 1% excluding currency movements and asset disposals. Big Blue should have invested more in its own business. Walmart spent $60 billion on buy-backs even as it fell far behind Amazon in e-commerce.

A radical option is to embrace torpor. The Brazilian investment firm 3G has become a specialist in buying mature firms and cutting what it claims is fat. Sales at its most recent target, Kraft, are falling at a rate of 5% a year. 3G is the force behind the proposed $120 billion takeover of the brewer SABMiller by AB Inbev. Inbev’s volumes are shrinking at a rate of 2%. In America the telecoms, cable and health-insurance industries are consolidating. The aim is to create stodgy oligopolies.

For business as a whole profit margins may eventually erode as wages rise. Regardless of whether that happens, though, most firms will still be faced with static top lines. Relative to sales and assets, capital investment in America has at least been steady and the shift of production to China and technological changes may mean the “natural” rate of investment firms need has fallen. But there is little doubt that a splurge in capital spending is necessary to get big companies growing again.

For all their obsession with growth, big listed firms appear paralysed. They long to expand, yet also want to protect peak profits, restrain wages and investment, buy back shares and hold armfuls of excess cash on their balance-sheets. What might make sense at the firm level causes stagnation across the economy, which in turn guarantees firms will stagnate. How many big companies will summon the strength of will to escape this exquisite trap?

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.