Mining firms and oil producers reel from another downward lurch in prices.

COMMODITY busts have left more of a mark on the barren mining region of northern Chile than the booms that preceded them. On the road to Sierra Gorda, a ramshackle copper-mining village in the middle of the Atacama Desert, dusty adobe cemeteries hold the remains of hundreds who died in penury after exports of potassium nitrate, or saltpetre, collapsed in the decade after the first world war.

Sierra Gorda itself looks like it is heading toward a similar decrepitude, despite huge copper mines carved into the hills around it. Chile, the world’s biggest copper producer, was a big beneficiary of the China-led commodities boom, yet the only hints of the past decade of high copper prices are newly installed streetlights. The sole open business on a recent afternoon was a woman selling empañadas from a tatty tent

From Chile to China the sense that another once-in-a-generation raw-materials boom has come to a definitive end is haunting global commodities markets. On December 9th shares of mining and oil companies took a fresh battering as iron-ore prices sank below $40 a tonne for the first time in a decade, and Brent crude, the global benchmark, briefly dipped below $40 a barrel, its lowest level since early 2009. On the same day Anglo-American, a mining conglomerate, said it would shed up to 85,000 jobs, almost two-thirds of its global workforce; shrink its business by 60%; and suspend the dividend at least until the end of 2016.

The biggest question hanging over the commodities markets is when, or indeed whether, Chinese demand will recover. This week a report showing a slump in China’s imports and exports in November was read differently by bulls and bears; though the value of imports of commodities fell year on year, the volumes of copper, iron ore and oil rose slightly compared with the previous month, according to Capital Economics, a consultancy. But with stocks of most commodities at unusually high levels, even a mixed message from China is mostly a reason to fret.

The supply situation is more clear-cut, but no less worrying. OPEC, the oil producers’ group, helped trigger the latest sell-off of crude by scrapping its already generous production quotas altogether at its annual meeting, which ended on December 4th. Likewise the world’s biggest miners, BHP Billiton and Rio Tinto, have stuck to plans to dig up more iron ore and other metals, shovelling more pain onto weaker rivals such as Anglo.

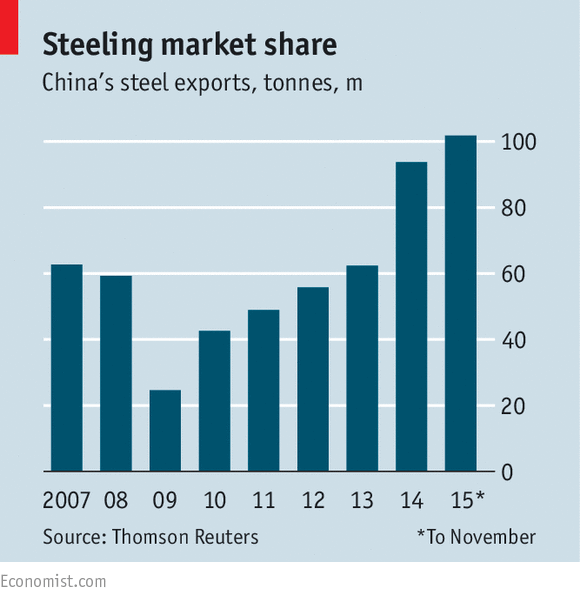

This glut is apparent throughout the supply chain. The steelmaking industry provides a striking example. Analysts at UBS, a Swiss bank, estimate the world has roughly a third more capacity than it needs. China produces roughly half of the global annual output of 1.6 billion tonnes a year. On one estimate, its hundred biggest steel firms lost some $11 billion during the first ten months of this year, an amount roughly double the profits earned last year. Unwanted products are finding their way onto global markets, even at a loss. Official data released this week confirm that China has, in the year through November, exported over 100m tonnes of steel for the first time. That is more than the total steel production of any country save Japan.

Excess supply on this scale will not disappear overnight. For places like Sierra Gorda and the firms that operate in them, the dust has not yet settled.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.