A BIS report advises: proceed with caution.

BITCOIN, Ethereum, XRP, Stellar, Cardano: the infant world of cryptocurrencies is already mind-bogglingly crowded. Amid the cacophony of blockchain-based would-be substitutes for official currencies, central banks from Singapore to Sweden have been pondering whether they should issue digital versions of their own money, too. None is about to do so, but a report prepared by central-bank officials from around the world, published by the Bank for International Settlements on March 12th—a week before finance ministers and central-bank heads from G20 countries meet in Buenos Aires—offers a guide to how to approach the task.

The answer? With care. For a start, it matters who will be using these central-bank digital currencies (CBDCs). Existing central-bank money comes in two flavours: notes and coins available to anyone; and reserve and settlement accounts open only to commercial banks, already in electronic form (though not based on blockchain) and used for interbank payments. Similarly, CBDCs could be either widely available or tightly restricted. A CBDC open to all would in effect allow anyone to have an account at the central bank.

CBDCs could be transferred either “peer to peer”, like cash, or through the banking system. They could be held anonymously, preserving the privacy of cash, or tagged, making it easier to trace suspicious transactions. Should they bear interest, that would affect demand not only for CBDCs but also for cash, bank deposits and government bonds.

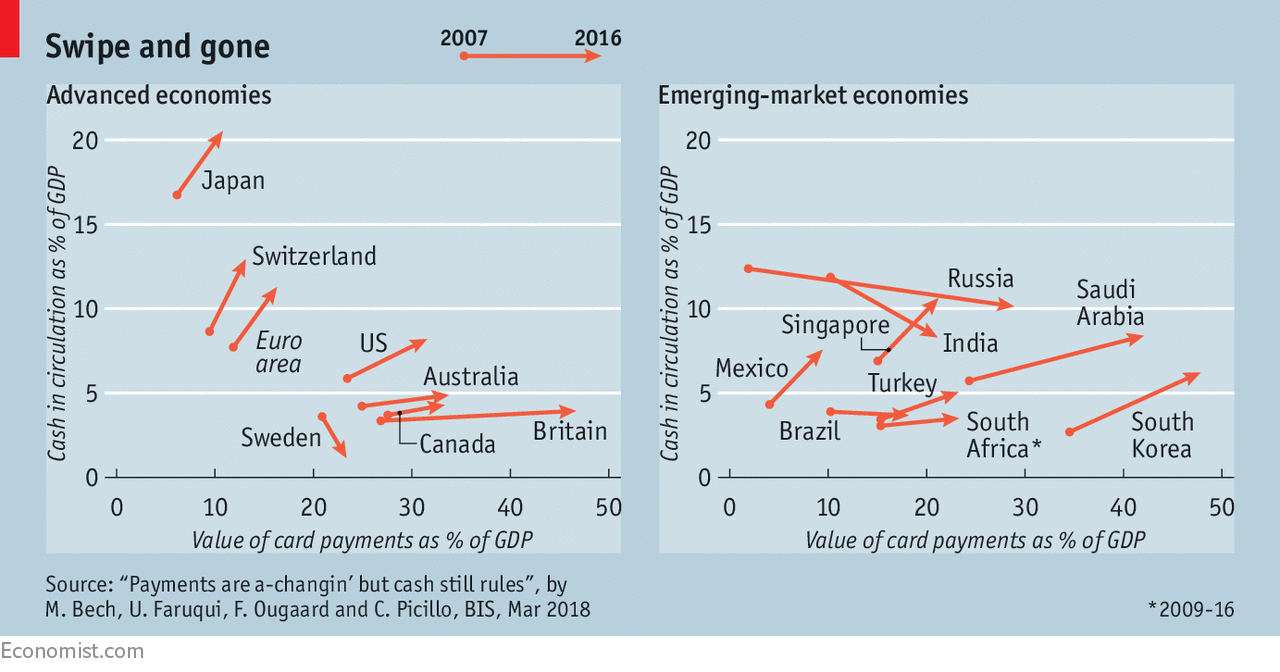

The report weighs up CBDCs’ possible effects on payment systems, monetary policy and financial stability. A steep decline in the use of cash could strengthen the case for a widely available CBDC. In Sweden the Riksbank is contemplating an “e-krona” for small payments. But in most countries, despite the growing use of cards, accelerated by the advent of contactless payments, cash remains popular (see chart). Experiments with a CBDC just for interbank payments, says the report, have “not shown significant benefits”.

A widely available, interest-bearing CBDC could, in principle, tighten the link between monetary policy and the economy. An interest rate tied to the policy rate may put a floor under money-market rates. Banks may have little choice but to pass changes in the CBDC rate on to depositors. Negative rates would be easier to implement, especially if high-denomination banknotes were abolished. But all this is uncertain. Retail depositors are less sensitive than institutional investors to changes in rates. Central banks already have plenty of tools. The authors are not sure that the putative gains yet warrant creating CBDCs.

On financial stability, they are more cautious still. In times of stress, depositors flee wobbly banks for safer homes—and a CBDC would allow “digital runs” to the central bank. Even in normal conditions, banks would face higher funding costs if they had to compete with the central bank for deposits. Digital versions of currencies used internationally (eg, the dollar) could worsen these complications, if foreigners were free to use them.

Central bankers focus more on the rise of private crypto-currencies, warning that they are speculative gambles. Expect more such admonitions in Buenos Aires—and no rush to mint CBDCs.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.