Baby boomers may recall, perhaps wistfully, how the golden-arched sign outside every McDonald’s restaurant would proclaim how many customers had been served by the chain. As they became adults, the number kept on climbing: 5bn in 1969; 30bn in 1979; 80bn in 1990. Jerry Seinfeld, a wry chronicler of the trivial, was moved to ask: “Why is McDonald’s still counting?” Do we really need to know about every last burger? Just put up a sign that says, “We’re doing very well.”

The counting stopped. The signs said simply: “Billions and billions served”. If this seems unhelpfully vague, that is how the counting business sometimes is. Many of America’s biggest companies, including McDonald’s, report a negative book value, a gauge of a firm’s net assets. Many more have a book value that is small relative to their market value: their shares look dear on a price-to-book basis. Much of this is down to the complexity of valuing a firm’s assets in the digital age. But the result is that price-to-book is a bad guide to a stock’s true value.

Stockpickers make a distinction between the price of a share and what it is truly worth. Price is a creature of fickle sentiment, of greed and fear. Value, in contrast, depends on a firm’s capabilities. There are various shorthand measures for this, but true “value” investors put the greatest store by the price-to-book ratio. It is the basis for inclusion in benchmarks such as the Russell value index. Countless studies have shown that buying stocks with a low price-to-book is a winning strategy.

But not recently. For much of the past decade, value stocks have lagged behind the general market and a long way behind “growth” stocks, their antithesis. Perhaps this is because, as the industrial age gives way to the digital age, the intangible assets that increasingly matter are not easy to put a value on. The tangible world is easier. Factories, machines, land and office buildings count as capital assets on a firm’s books, because they will generate profits for many years. It is a fairly straightforward business to come up with a value for them: it is what the firm paid. This value is gradually written off (depreciated) over time to reflect wear and tear and obsolescence.

Such fixed capital assets, along with current assets (cash, stocks of unsold goods, and so on) typically make up the bulk of book value. The problem is what it leaves out. These days, the value of a firm lies as much in its reputation, its processes, the know-how of staff and relationships with customers and suppliers as in tangible assets. Putting an accounting value on these intangibles is notoriously tricky. By their nature, they have unclear boundaries. Not every dollar of r&d or advertising spending can be ascribed to a well-defined asset, such as a brand or patent. That is in large part why, with a few exceptions, such spending is treated as a running cost, like rent or electricity.

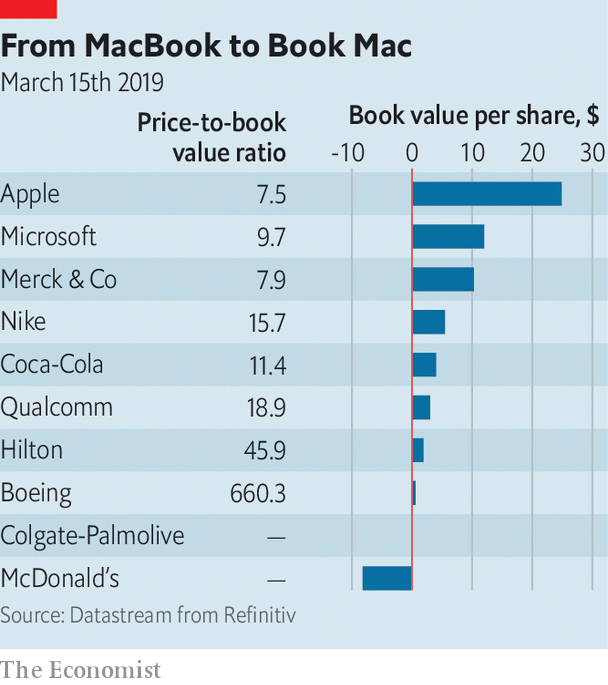

Increasingly price is detached from book value. The median price-to-book of s&p 500 stocks is 3.0. But plenty of well-known companies, whose competitive edge rests on brands or patents, have much higher ratios or even negative book values (see chart). McDonald’s has considerable brand value, which is not on its balance-sheet. It also has property assets that have been fully depreciated.

Some have called for accounting rules to change. But the more leeway a company has to turn day-to-day costs into capital assets, the more scope there is to fiddle with reported earnings. Better to spur the disclosure of spending that adds to intangible value. Analysts can then make their own judgments. Mr Harris finds that adjusting book value to reflect past r&d and advertising spending makes for more useful comparisons across stocks. It is not a perfect gauge. But no single measure—whether price-to-book or billions of customers served—can ever tell the whole story.The effect of mergers is to make things murkier. If, say, one firm pays $100m for another that has $30m of tangible assets, the residual $70m is counted as an intangible asset—either as brand value, if that can be gauged, or as “goodwill”. That distorts comparisons. A firm that has acquired brands by merger will have those reflected in its book value, says Simon Harris, of gmo, a fund-management firm; a firm that has developed its own brands will not. Share buy-backs make things murkier still. For any firm with a price-to-book greater than one, a buy-back will diminish book by proportionately more than it lowers the value of outstanding stock. So price-to-book rises further.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.