It was evident from the very beginning on April 20 that the oil market was headed for trouble.

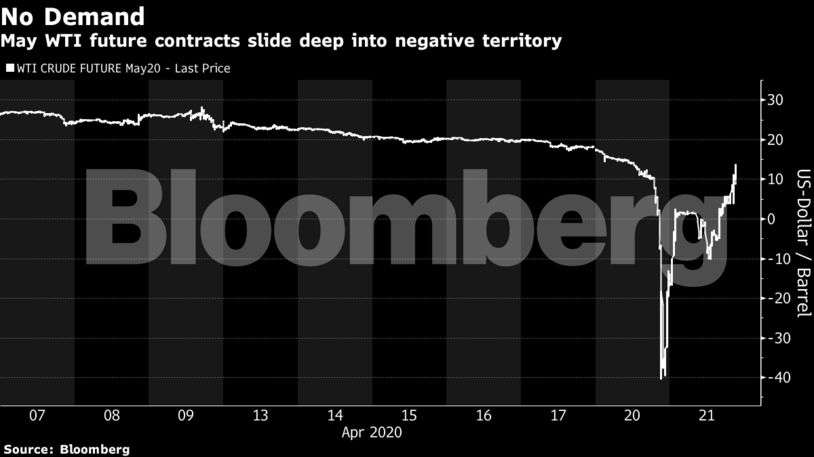

Frantic sell orders had been pouring in overnight and any traders who connected to the Nymex platform that morning could see a bloodbath was coming. By 7 a.m. in New York, the price on a key futures contract -- West Texas Intermediate for May delivery -- was already down 28% to $13.07 a barrel.

Thousands of miles away, in the Chinese metropolis of Shenzhen, a 26-year-old named A’Xiang watched events unfold on her phone in stunned disbelief. A few weeks earlier, she and and her boyfriend had sunk their entire nest egg of about $10,000 into a product that the state-run Bank of China dubbed Yuan You Bao, or Crude Oil Treasure.

As the night wore on, A’Xiang began preparing to lose it all. At 10 p.m. in Shenzhen -- 10 a.m. in New York -- she checked her phone one last time before heading to bed. The price was now $11. Half their savings had been wiped out.

As the couple slept, the rout deepened. The price set new low after new low in rapid-fire succession: the lowest since the Asian financial crisis of the 1990s, the lowest since the oil crises of the 1970s, the first time ever below zero.

And then, in a 20-minute span that ranks among the most extraordinary in the history of financial markets, the price cratered to a level that few, if any, thought conceivable. Around the world, Saudi princes and Texan wildcatters and Russian oligarchs looked on with horror as the world’s most important commodity closed the trading day at a price of minus $37.63. That’s what you’d have to pay someone to take a barrel off your hands.

Many things about the explosive, flash-crash-like nature of the sell-off are still not fully understood, including how big a role the Crude Oil Treasure fund played as it sought to get out of the May contracts hours before they expired (and which other investors found themselves in the same position). What is clear, though, is that the day marked the culmination of the oil market’s most devastating crisis in a generation, the result of demand drying up as governments around the world locked down their economies in an attempt to manage the coronavirus pandemic.

For the petroleum industry, it was a grimly symbolic moment: The fossil fuel that helped to build the modern world, so prized it became known as “black gold,” was now not an asset but a liability.

“It was mind-bending,” said Keith Kelly, a managing director at the energy group of Compagnie Financiere Tradition SA, a leading broker. “Are you seeing what you think you’re seeing? Are your eyes playing tricks on you?”

US. ETF Pain

While the deeply negative prices of that Monday were largely limited to the U.S., and in particular the soon-to-expire WTI contract for May delivery, the world felt the shockwaves, with ripple effects dragging global prices to the lowest since the late 1990s.

Traders are still piecing together the confluence of factors that led to the collapse. And regulators are scrutinizing the issue, according to people familiar with the matter.

For small-time investors in Asia like A’Xiang who bet enthusiastically on oil, though, it has been a reckoning.

She awoke to a text at 6 a.m. from Bank of China informing her that not only had their savings been lost but that she and her boyfriend may actually owe money.

“When we saw the oil price start plunging, we were prepared that our money may be all gone,” she said. They hadn’t understood, she said, what they were getting into. “It didn’t occur to us that we had to pay attention to the overseas futures price and the whole concept of contract rolling.”

In all, there were some 3,700 retail investors in Bank of China’s Crude Oil Treasure fund. Collectively, they lost $85 million.

Soon, events would catch up with mom-and-pop American investors who had made much the same bet as A’Xiang -- that oil had to go back up -- by buying the United States Oil Fund, an exchange-traded fund known as USO.

That fund, into which investors poured $1.6 billion the previous week, hadn’t been holding the May WTI contract on last Monday. But the rout sparked a chain reaction in the market that burned these investors, too.

The day’s events were set in motion more than two weeks earlier, with the pandemic shattering economies and stalling demand for oil: flights were grounded; traffic jams disappeared; factories ground to a halt.

The below-zero price scenario was, in some corners of the market, starting to be considered. On April 8, a Wednesday, CME Group Inc, which owns the oil-futures exchange, advised clients that it was “ready to handle the situation of negative underlying prices in major energy contracts.”

That weekend, producing nations led by Saudi Arabia and Russia finalized their response to the crisis: a deal to slash production by 9.7 million barrels a day, amounting to a tenth of global production. That wouldn’t be nearly enough. Refineries started shutting down. Buyers for cargoes of oil for immediate delivery in physical markets disappeared.

Futures prices remained, for a while, relatively steady.

That was in part thanks to folks like A’Xiang. In China, investors large and small were betting on higher commodity prices, believing the world would overcome the virus and that demand would bounce back. Bank of China branches posted ads on Wechat, showing an image of golden barrels of oil under the title “Crude oil is cheaper than water”.

Yet on April 15, CME offered clients the ability to test their systems to prepare for negativity. That’s when the market really woke up to the idea that this could actually happen, said Clay Davis, a principal at Verano Energy Trading LP in Houston.

“That’s when the dam broke,” he said.

Physical Delivery

By the time Monday April 20 rolled around, most ETFs and other investment products -- though not the Crude Oil Treasure fund -- had shifted their position out of the May WTI contract into the next month.

Futures contracts are settled by physical delivery, and if you happen to get stuck with one when it expires, you become the owner of 1,000 barrels of crude. Rarely does it come to that.

But now it was.

The physical settlement for the benchmark WTI takes place at Cushing, Oklahoma. When storage tanks there fill up, the price on the expiring contract can plunge and become disconnected from the global market. With demand evaporating, inventories at Cushing were soaring. In March and April, they climbed 60% to just under 60 million barrels, out of a total working capacity of 76 million –- and analysts reckon much of the remaining space is already earmarked.

So on the crucial Monday, the penultimate day of trading in the May WTI contract, there were precious few traders able or willing to take physical delivery.

Much of the market was focused then on the settlement price, determined at 2:30 p.m. in New York. Investment products –- including Bank of China’s –- typically seek to achieve the settlement price. That often involves so called trading-at-settlement contracts, which allow oil traders to buy or sell contracts ahead of time for for whatever the settlement price happens to be.

No Buyers

On that afternoon, with trading volumes thin and sellers outnumbering buyers, the trading-at-settlement contracts quickly moved to the maximum discount allowed, of 10 cents per barrel. For a period of around an hour, from 1:12 p.m. until 2:17 p.m., trading in these contracts all but dried up. There were no buyers.

The result was the carnage of that afternoon. At 2:08 p.m., WTI turned negative. And then, minutes later, sank to as low as minus $40.32 before rebounding slightly at the close.

“The trading at settlement mechanism failed,” said David Greenberg, president of Sterling Commodities and a former member of the board at Nymex. “It shows the fragility of the WTI market, which is not as big as people think.”

Prices in the U.S. physical market, set by reference to the WTI settlement, also plunged, with some refiners and pipeline companies posting prices to their suppliers as low as minus $54 a barrel.

Bank of China’s investment product offers an explanation of why the move below zero was so dangerous. The bank had demanded investors like A’Xiang put up the entire cost of what they were buying in advance. That meant the bank’s position looked risk-free.

But not if prices dropped below zero: then there wouldn’t be enough money in the investors’ accounts to cover the losses.

The bank had a total position of about 1.4 million barrels of oil, or 1,400 contracts, according to a person familiar with the matter. It wound up having to pay about 400 million yuan ($56 million) to settle the contracts.

Across the investing world, others were faced with similar risks. ETFs could be bankrupted if the price of the contracts they held went below zero. Facing that possibility, they shifted a large chunk of holdings into later delivery months. Some brokers barred clients from opening new positions in the June contract.

The moves amounted to a new wave of selling that swept across oil markets. On Tuesday, the June WTI contract plunged by 68% to a low of just $6.50. And this time it was not limited to U.S. contracts: Brent futures also plunged, hitting a 20-year low of $15.98 on Wednesday, driving the price of Russian, Middle Eastern and West African oil that is priced relative to it to levels near zero.

CFTC’s Top Priority

Harold Hamm, chairman of Continental Resources Inc., called for an investigation, saying that the dramatic plunge in the last minutes of Monday “strongly raises the suspicion of market manipulation or a flawed new computer model.”

Within the Commodity Futures Trading Commission, unpacking what occurred during those final minutes of trading on April 20 has since become top priority, according to people familiar with the matter. While reviews and investigations into what occurred are just beginning, thus far, top officials believe the moves were likely the result of a confluence of economic and market factors, rather than the result of market manipulation.

An issue the CFTC is exploring is whether the storage capacity data posted by the U.S. Energy Information Administration accurately reflected the actual availability of space, two of the people said.

“The temporarily negative price at which the WTI Crude futures contract traded earlier this week appears to be rooted in fundamental supply and demand challenges alongside the particular features of that futures product,” CFTC Chairman Heath Tarbert told Bloomberg News.

Nonetheless, he added: “CFTC is conducting a deep dive to understand why the WTI price moved with the velocity and magnitude observed, and we will continue to oversee our markets’ role in facilitating convergence between spot and futures prices at expiration.”

The CME, for its part, argues that Monday’s plunge was a demonstration of the market working efficiently. “The markets worked exactly how they’re supposed to do,” CEO Terry Duffy told CNBC. “If Hamm or any other commercials believe that the price should be above zero, why would they have not stood in there and taken every single barrel of oil if it was worth something more? The true answer is it wasn’t at that given moment in time.”

Whoever is right, the events of the week have changed the oil market forever.

“We witnessed history,” “For the sake of oil-market stability,” this “should not be allowed to happen again.”

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.