Phase two

Russia’s economic problems move from the acute to the chronic

DMITRY MALIKOV, a wavy-haired crooner, normally sings schmaltzy love tunes. But his latest clip, which he calls “A New Year’s Appeal to the Rouble”, captures the zeitgeist in Russia. “Sure, it’s a bit tough, but happiness is ahead,” he belts. “Just wait, just wait, don’t fall.” Despite his plea, the rouble is falling: on January 21st it dropped to more than 85 to the dollar, a record low. References to the economic “crisis” pepper daily conversation; news broadcasts lead with breathless coverage of the oil markets, and even the patriarch of the Russian Orthodox church was asked his thoughts on the exchange rate during his annual Christmas interview.

Russia’s economy had a torrid 2015. As the oil price tumbled from its mid-2014 peak of over $100 a barrel, Russia’s exports and government revenues, heavily dependent on oil and gas, collapsed. GDP shrank by nearly 4%; inflation ran close to 13%. Having lost half its value against the dollar in the second half of 2014, the rouble dipped a further 20% in 2015. But in the autumn the contraction slowed. Vladimir Putin, Russia’s president, triumphantly declared that “the peak of crisis” had passed.

Recent turbulence in the oil market has put hopes of a speedy recovery to rest. The IMF reckons GDP will contract again this year, by 1%. Senior officials speak morosely of a “new reality”, acknowledging that their energy-driven growth model has exhausted itself. Yet Russia is unlikely to see a repeat of the acute problems that befell it in late 2014. For one thing, Russian businesses have much healthier finances. Their foreign debt has fallen by a third since 2014. From now until May, firms and banks are due to repay less than they did in December 2014 alone. The second half of the year will be about as easy.

The banking sector is looking better, thanks to a raft of measures from the central bank to recapitalise it and to allow greater forbearance on souring debts. The big oil companies, meanwhile, have coped with a weak currency. Their operating expenses are priced in roubles but most of their revenues come in dollars. Progressive oil and gas taxes have also helped: when prices fall, the state budget absorbs much of the pain. Total oil production grew by 1.4% in 2015, reaching record highs. The profitability of beasts like Rosneft, Lukoil and Bashneft is higher than it was in 2014, according to Moody’s, a rating agency.

The government’s finances, however, are shaky. The budget for 2016 assumes an average oil price of $50 a barrel, which was to have produced a deficit of 3% of GDP. However, the arithmetic of Russia’s public finances is unforgiving: the budget deficit rises by roughly 1% of GDP for every $5 drop in the oil price. At the current $30 a barrel (and assuming no change in spending plans or the exchange rate), the deficit would probably hit 7%.

Yet Mr Putin has decreed that the deficit should not exceed 3%. In response, the finance ministry has called for cuts of 10% (defence and social spending are largely exempt). Officials have also suggested privatising state assets. All this, though, is unlikely to yield enough to plug the growing deficit. Filling the gap by issuing bonds would be expensive: yields are high. Moreover, Russia’s default in 1998-99 left its elite with an aversion to debt.

The government can always tap its rainy-day fund, but it holds only $50 billion, down from $90 billion a year ago. If the budget deficit hits 6% of GDP the fund will be empty by the end of the year, says Timothy Ash of Nomura, a bank. A second fund, which is supposed to finance pensions, holds a further $70 billion, but many of its assets are illiquid.

If the government runs out of ready cash, Mr Putin may be tempted to repeat a well-worn trick—printing roubles. But that would boost inflation and hasten the rouble’s decline, further sapping the purchasing power of Russian firms and families. Deep cuts to government spending, on the other hand, will also add to the travails of the non-oil economy.

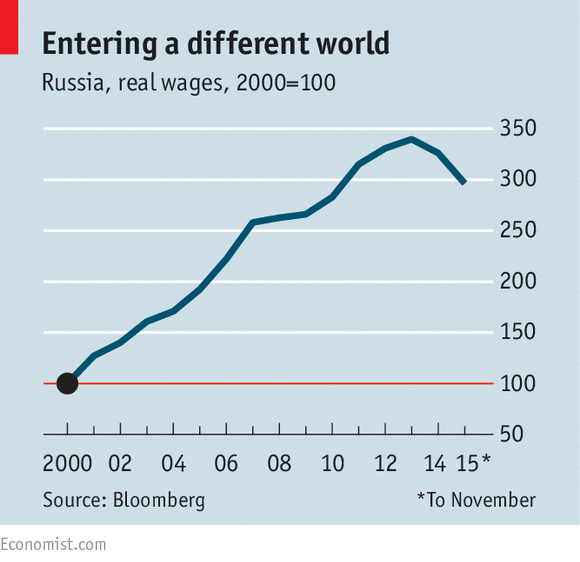

Russians face a fundamental degradation of their quality of life, says Natalia Zubarevich of the Independent Institute for Social Policy, a think-tank. Real wages fell by 9% in 2015 and 4% in 2014, the first dip since Mr Putin came to power in 2000 (see chart). GDP per person is down from a post-Soviet peak of close to $15,000 in 2013 to around $8,000 this year. While official unemployment is just 6%, wage arrears are up. More than 2m people fell into poverty in 2015, and the share of families that lack funds for food or clothes rose from 22% to 39%. Pensions are normally indexed to inflation, but in 2016 they will rise by just 4%.

In turn, consumer spending, once the engine of Russia’s economy, has withered. Retail sales dropped by 13%, year on year, in November. Foreign travel during the recent holiday season dipped by 30% compared with a year ago. Even those seeking darker escapes are finding them ever less affordable: the price of heroin (mainly smuggled from Afghanistan) has doubled in roubles over the past year.

In theory the 25% fall in the inflation-adjusted exchange rate in the past year provides a golden opportunity to diversify away from hydrocarbons. To a foreign buyer, labour is now cheaper in Russia than in China. However, foreign investment is wilting too. FDI inflows, which were sliding before the crisis, fell from a quarterly peak of $40 billion in early 2013 to $3 billion in the second quarter of 2015. Foreigners are likely to become net divestors soon. Small wonder that manufacturing production was down by 5% year on year in the first half of 2015; agricultural output is stagnant. The first, most dramatic phase of Russia’s crisis may indeed be behind it, as Mr Putin claimed. But for ordinary Russians, phase two will not seem much better

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.