Saudi Aramco

A possible IPO of Saudi Aramco could mark the end of the post-war oil order.

“THE amounts of oil are incredible, and I have to rub my eyes frequently and say like the farmer: ‘There ain’t no such beast.’” So wrote an American oilman in the Persian Gulf a few years after the discovery in 1938 of a gusher of oil from Saudi Arabia’s Well Number Seven, 4,727 feet (1,440 metres) below the desert floor.

You could say the same today about Saudi Aramco, the state-owned firm that for decades has had exclusive control of Saudi Arabia’s oil and is the world’s biggest, most coveted and secretive oil company. On January 4th the kingdom’s deputy crown prince, Muhammad bin Salman, told The Economist that Saudi Arabia was considering the possibility of floating shares in the company, adding that personally he was “enthusiastic” about the idea.

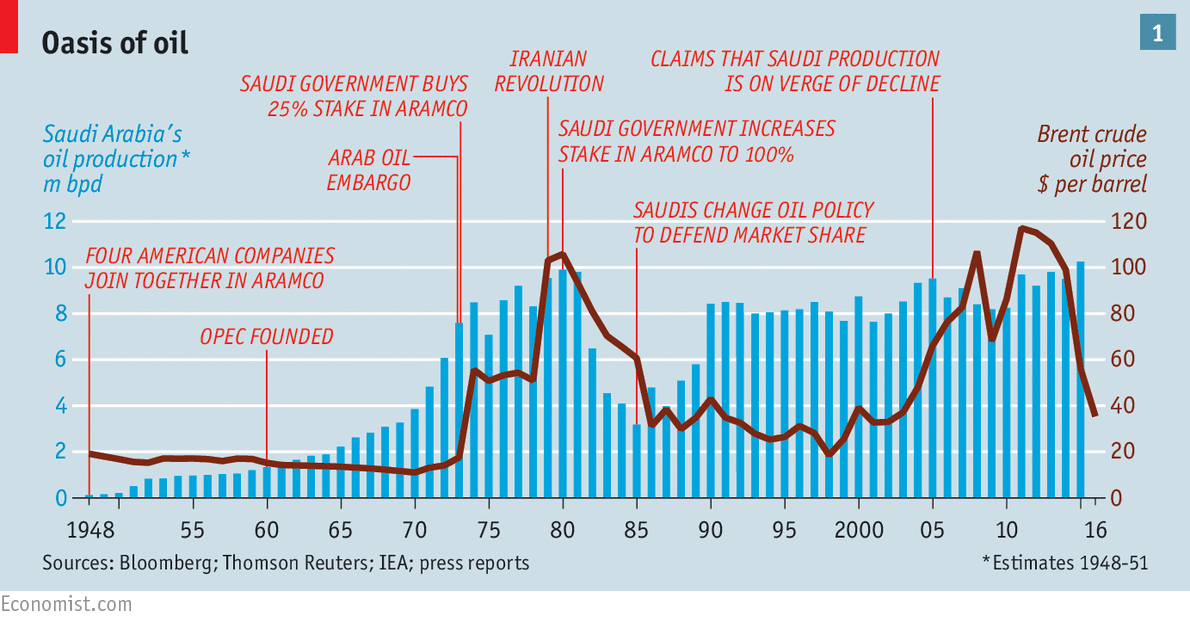

It was a stunning revelation. Officials say options under preliminary consideration range from listing some of Aramco’s petrochemical and other “downstream” firms, to selling shares in the parent company, which includes the core business of producing crude. The staggered nationalisation of the Arabian American Oil Company (Aramco), made up of four big American firms, in the 1970s was emblematic of a wave of “resource nationalism” that has helped define the industry (see chart 1).

Aramco is worth, officials say, “trillions of dollars”, making it easily the world’s biggest company. It says it has hydrocarbon reserves of 261 billion barrels, more than ten times those of ExxonMobil, the largest private oil firm, which is worth $323 billion. It pumps more oil than the whole of America, about 10.2m barrels a day (b/d), giving it unparalleled sway over prices. If just a sliver of its shares were placed on the Saudi stock exchange, which currently has a total market value of about $400 billion, they could greatly increase its size.

Prince Muhammad says a listing would not only help the stockmarket, which opened to foreigners last year. It would also make Aramco more transparent and “counter corruption, if any”. A final decision has yet to be taken. Yet the prince has held two recent meetings with senior Saudi officials to discuss a possible Aramco listing and diplomats say investors are being sounded out. The talk is of at first floating only a small portion of the company in Riyadh, perhaps 5%. In time that could rise—though not by enough to jeopardise the kingdom’s control of decision-making.

The aim would be to foster greater shareholder involvement in Saudi Arabia; a senior official said there was no intention of surrendering control of Aramco or its oil resources to foreign firms. But it is part of a frenzy of reforms proposed by the prince that his government is rushing to keep pace with. “Everything is on the table. We are willing to consider options we were not willing to get our heads around in the past,” an official says.

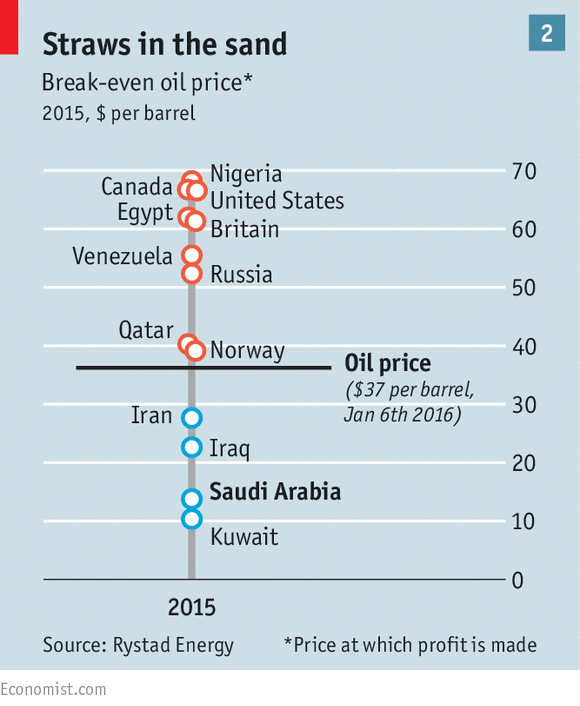

For many investors, a listing of Aramco, however partial, would be a prize even at today’s low oil prices. Its “upstream” business is mouth-watering. Rystad Energy, a Norwegian consultancy, says no other country except Kuwait can produce oil at a lower break even cost (see chart 2).

By the standards of national oil monopolies, analysts say that Aramco is well run. In the 1940s and 1950s, when the American consortium recruited young Saudis, it was an “unlikely union of Bedouin Arabs and Texas oil men, a traditional Islamic autocracy allied with modern American capitalism”, writes Daniel Yergin in “The Prize”. Under American ownership, it built towns with schools, wiped out malaria and cholera, and helped farmers become entrepreneurs, officials recall, explaining why it was popular with Saudis.

It was a different story in Iran and elsewhere, where citizens grew sick of the colonial-era concessions taken by British and French firms, and a wave of nationalisation began. The Saudis, having declared their first 25% stake in Aramco in 1973 “indissoluble, like a Catholic marriage”, were unable to resist the tide. Full nationalisation of Aramco came in 1980. But an American business ethic survived. Just over a decade ago Matthew Simmons, an American banker, argued that Saudi wells were past their prime and that production would soon peak. Yet Aramco has increased output by more than 1m b/d in the past five years, reaching record highs. “They’ve proven their resilience,” says Chris DeLucia of IHS, a consultancy.

Questions surround the company, though. Mr DeLucia says 87% of its output is oil; it needs to develop more gas to satisfy the country’s needs for cleaner, cheaper power. Some argue that its reserves, which have barely budged since the late 1980s, are overstated. Internal documents about them are “phenomenally closely guarded secrets” says a local observer.

The company does not report its revenues. Its fleet of eight jets, including four Boeing 737s, and a string of football stadiums suggest that it is not run on purely commercial lines. It is the government’s project manager of choice even for non-oil developments, and runs a hospital system for 360,000 people. A listing would require it to become more transparent.

But even with greater disclosure, minority shareholders may play second fiddle. The company is integral to the social fabric of Saudi Arabia and the survival of the ruling Al Saud dynasty, providing up to nine-tenths of government revenues. Cuts in its output have been a foreign-policy lever through which OPEC, the producers’ cartel, has often sought to rescue oil prices.

Investors in Russia’s Gazprom, another national champion, have watched in frustration as the company has been used as an arm of the Russian foreign ministry. Elsewhere, selling stakes in national oil companies has had mixed results.

Prince Muhammad’s desire for reform fits a pattern that some consider reckless. Saudi Arabia has recently forced OPEC to maintain production despite oil falling from a peak of $120 a barrel to below $35. Its decision on January 3rd to suspend diplomatic relations with Iran, a fellow OPEC member, makes it harder for both to agree on production cuts, though Saudi officials are in any case adamant that they have no intention of rescuing prices.

Others believe Saudi Arabia’s strategy makes sense. They think it wants to protect its share of the global oil market by driving high-cost producers to the wall at a time when unconventional forms of oil, such as American shale, have had gushing success.

Another threat is alternative forms of energy, such as wind and solar, which may well challenge fossil fuels. Selling shares in Saudi Aramco could thus be intended to cash in before the “decarbonisation” of the economy starts to gain credibility. It would also fit with a trend that has started to transform the oil industry for the first time in half a century—denationalisation.

Paul Stevens of Chatham House, a British think-tank, says a cadre of well-educated technocrats from oil-producing nations are wondering whether their national oil companies are “ripping us off”, through corruption or inefficiency. Brazil’s corruption-plagued Petrobras proves that public markets are no guarantee of probity. But as in Mexico, which is opening up its oil industry for the first time since 1938, many want to impose market-based checks and balances, so that no company can operate as a state within a state. If that happens to Saudi Aramco, the biggest of them all, it will have global repercussions

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.