But it cannot squeeze Iran and Venezuela without risking higher oil prices for its own consumers

AMerica has been a superpower for decades. As an energy superpower, however, it is barely a teenager. As recently as 2015 it was illegal to export oil. Within ten years the shale boom has transformed it into the world’s biggest producer of crude. No longer must it tiptoe around regimes whose policies it detests but whose oil it craves. President Donald Trump touts an age of “energy dominance”. He has put its burgeoning energy prowess to the test with tough sanctions on Iran and Venezuela. But dreams of dominance are running into the realities of energy markets.

On April 22nd the American administration announced that no further waivers would be granted to countries importing oil from Iran. “We are going to zero,” declared Mike Pompeo, the secretary of state. Waivers to eight countries, granted in November, were due to expire on May 2nd. Even so, investors were shocked that no exceptions were allowed. According to the state department, Saudi Arabia, the United Arab Emirates and America will help meet demand. But Brent crude, the international benchmark, quickly topped $74, the highest level in nearly six months.

The Trump administration is right to make to make a fuss about America’s oil boom. According to the International Energy Agency, by 2021 the country may be a net exporter of oil. This would be a stunning reversal. Not long ago, notes Amy Myers Jaffe of the Council on Foreign Relations, a think-tank, oil imports were the largest cause of America’s current-account deficit.

Mr Trump announced last May that America would impose sanctions on Iran and withdraw from the deal on international oversight of its nuclear capacity signed during Barack Obama’s presidency—the “worst deal ever”, as Mr Trump liked to call it. He urged the Organisation of Petroleum Exporting Countries (OPEC), privately and on Twitter, to boost production to help restrain oil prices. Saudi Arabia duly did so, increasing output by 600,000 barrels a day from June to November, when the sanctions were to take effect.But it is wrong to think it can bring about dramatic change in two petro-states without risking dramatic spikes in petrol prices. (Those concerned about climate change might welcome expensive oil; Mr Trump is not one of those people.) America’s government does not control its oil industry. Oil firms are backed by investors whose interests do not necessarily align with those of the president. Nor can it control the world’s many buyers and sellers of crude. American production accounts for about 15% of global output, a striking increase from what it was but still a small share of total supply. Complicating matters, investors have struggled to anticipate the Trump administration’s actions. Rather than stabilise oil markets, America has been as likely to do the opposite.

At the last minute, however, Mr Trump announced that eight countries would be exempt from the waivers for six months—including China and India, the biggest importers of Iranian oil. Investors and Saudi Arabia were caught off guard. The kingdom requires oil at around $80 a barrel to meet its budgetary needs; in December Brent prices sank to $51. OPEC and its allies scrambled to cut production and shore up prices. In December they said they would decrease output by 1.2m barrels a day.

The next sanctions came in January, after opponents of Nicolás Maduro’s ruinous regime in Venezuela declared Juan Guaidó, the head of its national assembly, the legitimate leader. America recognised Mr Guaidó and unveiled sanctions to choke off the country’s oil company, Mr Maduro’s main source of cash. “America now appreciates that energy is a source of foreign-policy strength rather than a vulnerability,” says Meghan O’Sullivan, a former adviser to George W. Bush and a professor at Harvard University. But using that strength effectively can be difficult.

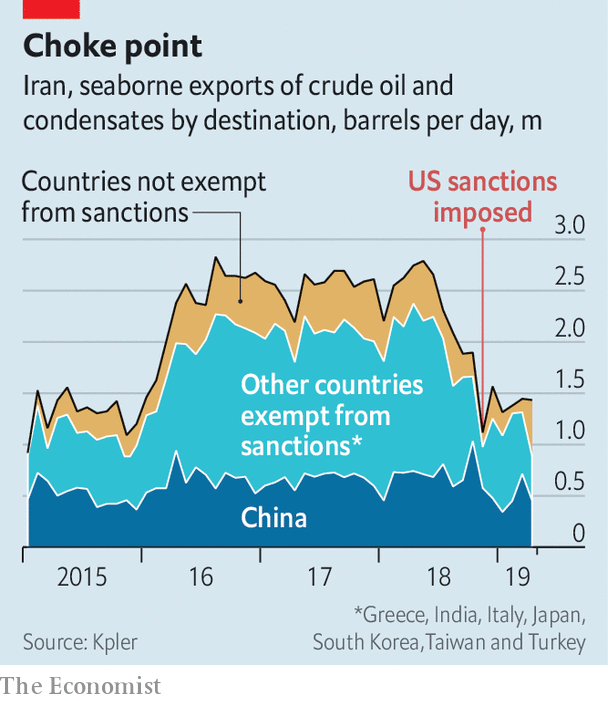

Sanctions on Iran and Venezuela have yet to produce the desired effect. Mr Maduro still clings to power. Iran has met none of Mr Trump’s demands. Its crude exports have fallen by about half since Mr Trump said America would withdraw from the nuclear deal last year, but they remained well above zero in March, at about 1.4m barrels a day, according to Kpler, a data firm (see chart). China, in particular, has continued to import Iranian oil. The announcement that waivers will expire seeks to change that. Countries that continue to import Iranian oil, the state department says, could be cut off from America’s banking system.

This manoeuvre is risky, says Helima Croft of RBC Capital Markets, an investment bank. Iran’s foreign ministry is threatening to retaliate by closing the Strait of Hormuz, a major export channel for the region’s crude. With little left to lose, it may stop allowing international inspectors to monitor its nuclear programme. Oil markets, too, face uncertainty. Prices were already rising, because of plunging output in Venezuela and civil war looming in Libya. The state department has not said how soon America might impose sanctions on countries that continue to import Iranian oil. China may do so—an official from its foreign ministry declared that China “opposes the unilateral sanctions”. That could complicate a bilateral trade dispute that had looked close to resolution.

The number of rigs drilling in America has risen since the start of the year, as the oil price has climbed. Yet American shale oil is mostly “light”. Refineries in America and elsewhere are thirsty for heavy crude, because Venezuela’s production of the stuff has dropped and demand for distillates made with it is strong. There is a “fundamental mismatch” between the type of crude the world increasingly wants and what America is pumping, says Bernadette Johnson of Drillinginfo, a research firm.

Much therefore depends on whether Saudi Arabia boosts production, as the Trump administration hopes. After last year’s flip-flops, it may be reluctant to move fast. OPEC and its partners have their next formal meeting in late June. Even if Saudi Arabia were to ramp up production quickly and dramatically, analysts debate how long that boost could be sustained. A recent bond prospectus for Saudi Aramco, the kingdom’s oil giant, disclosed that a famous oilfield is ready to sustain production of 3.8m barrels a day, about 25% less than analysts had assumed.

Neil Beveridge of Bernstein, a research firm, points out that OPEC’s spare capacity could drop dangerously low as Iran’s production falls and Saudi Arabia works to ramp up. That would leave the oil price vulnerable to supply shocks—if fighting in Libya escalates, for instance. America, the energy adolescent, can certainly roil oil markets. But it is unable to control them.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.