Falling bank shares

Some of the oldest financial houses are at the eye of a new financial storm

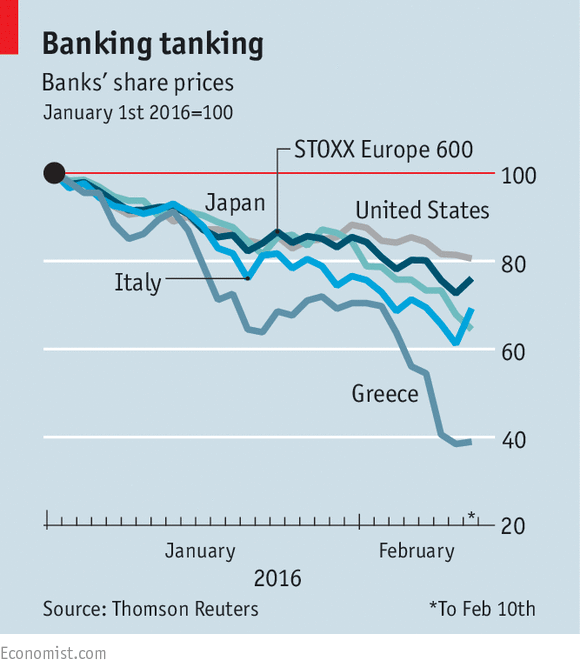

IF THE start of the year has been desperate for the world’s stockmarkets, it has been downright disastrous for shares in banks. Financial stocks are down by 19% in America. The declines have been even steeper elsewhere. Japanese banks’ shares have plunged by 36% since January 1st; Italian banks’ by 31% and Greek banks’ by a horrifying 60% (see chart). The fall in the overall European banking index of 24% has brought it close to the lows it plumbed in the summer of 2012, when the euro zone seemed on the verge of disintegration until Mario Draghi, the president of the European Central Bank (ECB), promised to do “whatever it takes” to save it.

The distress in Europe encompasses big banks as well as smaller ones. It has affected behemoths within the euro area such as Société Générale and Deutsche Bank (see next story)—both of which saw their shares fall by 10% in hours this week—as well as giants outside it such as Barclays (based in Britain) and Credit Suisse (Switzerland).

The apparent frailty of European banks is especially disappointing given the efforts made in recent years to make them more robust, both through capital-raising and tougher regulation. Euro-zone banks issued over €250 billion ($280 billion) of new equity between 2007, when the global financial crisis began, and 2014, when the ECB took charge of supervising them. Before taking on the job, it combed through the books of 130 of the euro zone’s most important banks and found only modest shortfalls in capital.

Some of the recent weakness in European banking shares arises from wider worries about the world economy that have also driven down financial stocks elsewhere. A slowdown in global growth is one threat. Another is that the negative interest rates being pursued by central banks to try to prod more life into economies will further sap banks’ profits. A retreat in Japanese bank shares turned into a rout following such a decision in late January. Investors in European banks fret not just about lacklustre growth but also a possible move deeper into negative territory by the ECB in March. On February 11th Sweden’s central bank cut its benchmark rate from -0.35% to -0.5%, prompting shares in Swedish banks to tumble.

But the malaise of European banking stocks has deeper roots. The fundamental problem is both that there are too many banks in Europe and that many are not profitable enough because they have clung to flawed business models. European investment banks lack the deep domestic capital markets that give their American competitors an edge. Deutsche, for instance, has only just resolved to hack back its investment bank in the face of a less hospitable regulatory environment following the financial crisis.

And there are still too many poorly performing smaller banks within national markets. Although this year’s share-price declines have been steepest in Greece, these largely reflect renewed political tensions over implementing the country’s third bail-out. The banks arousing fresh concern are those in Italy, whose troubles go beyond an excess of them. One specific worry is the dire state of the country’s third-biggest (and the world’s oldest) bank, Monte dei Paschi di Siena, which has long been in intensive care and whose share price has fallen by 56% this year. Its woes reflect poor governance, a problem that plagues Italian banks, many of which are part-owned by local, politically connected foundations.

A more general worry is that Italy’s banking sector as a whole is weighed down with bad loans which have built up during recent years. Although Italian GDP has been expanding since the start of 2015, it is still around 9% lower than its pre-crisis peak in early 2008. This has hurt Italian firms—and their pain has been transferred to the banks that lent to them. Gross non-performing loans amount to €360 billion (18% of the total), of which €200 billion are especially troubled.

There is nothing new about Italy’s high level of non-performing loans; if the recovery can be sustained they should eventually start to come down. Moreover, over half of the sourest loans are covered by provisions, which means that the potential bill is more manageable, at around €90 billion rather than €200 billion. What has changed this year is a new European approach to tackling troubled banks, which shifts the burden for bail-outs from taxpayers to creditors who are “bailed in” when big losses arise. These rules, which have come fully into force this year (a few countries applied them in 2015), mean that senior bondholders and depositors with balances above €100,000 can be stung when banks are resolved.

Bank bonds are generally held by institutional investors who can look after themselves, but in Italy around €200 billion are in the hands of retail customers who were lured to invest in them until 2011 by favourable tax treatment. These retail bonds would be vulnerable if banks run short of capital after big write-downs.

This danger was highlighted late last year when four small banks were rescued in a rush to avoid this year’s more stringent bail-in provisions. That process ensnared retail bondholders holding junior debt, who could already be bailed in under the previous rules. One committed suicide. The furore has unnerved Italians. Ignazio Visco, governor of the central bank, has said that a less abrupt transition to the new bail-in regime would have been better.

The strict rules have also curtailed the ability of the Italian government, led by Matteo Renzi, to calm nerves by excising the bad loans from the banking system. Instead of setting up a state-backed “bad bank” to remove them, Mr Renzi has had to adopt a feebler approach in which the government will guarantee the senior tranches of securitised bundles of the bad loans. Investors plainly doubt this scheme will help much, to judge by the performance of Italian bank shares.

Frustration with European constraints on Italy’s attempt to sort out its banks is one reason why Mr Renzi has been making barbed attacks on the German way of running the euro area. Such political tension is adding to jitters about Italian banks. Portuguese banking shares have also tumbled, in part because a new left-of-centre coalition government alarmed international investors by its decision to impose heavy losses on some senior bank bonds late last year. In seeking to transfer the risk of failing banks away from taxpayers to creditors, European policymakers may have thought they were depoliticising the banks. In the euro-zone periphery, however, politics is never peripheral.

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.