A corrosive climate

Overcapacity has worsened the woes of an already unprofitable industry

Clouds over Scunthorpe’s future

Clouds over Scunthorpe’s future

FOR 151 years blast furnaces in Scunthorpe, a town in northern England, have been churning out pig iron and steel. In spite of rounds of consolidation, in which employment in the industry in Britain has fallen from more than 200,000 in the 1970s to around 24,000 now, Scunthorpe’s rust-streaked steelworks has survived, specialising in producing steel plates, wire rods and rails.

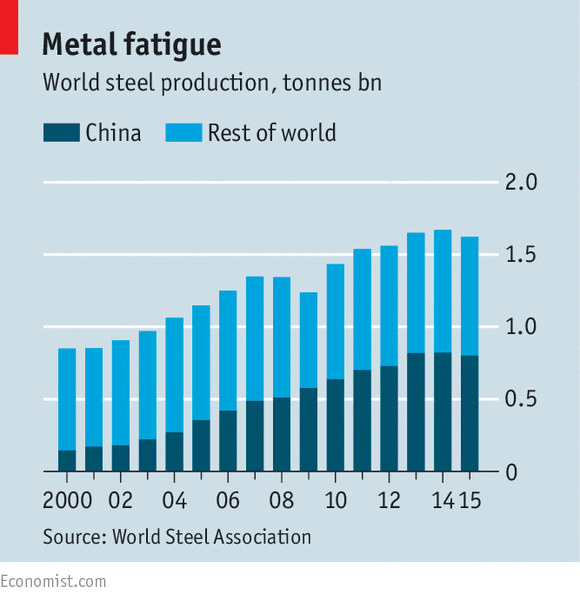

Now, though, a global crisis of overcapacity is putting the rich world’s remaining producers of low-value bulk steels, and even some specialist producers such as Scunthorpe’s, at risk. Over the past year bulk steel prices have fallen by more than half. This week the World Steel Association (WSA), an industry body, said that global production in 2015 had fallen by 2.8% (see chart). It declined in every large country except India—though even its steelmakers are suffering, and pressing the government for tariffs on Chinese imports. US Steel, America’s biggest producer, said this week that it lost $1.5 billion last year. This month it laid off 1,300 workers. British steelworkers have fared even worse: one in six lost their jobs last year, and Tata Steel announced a further 1,050 job cuts this month.

The collapse in the steel price is mainly the result of falling demand and, until recently, rising production in China, says Edwin Basson of the WSA. Between 2000 and 2014, global production doubled to around 1.6 billion tonnes a year, mainly driven by rising output in China. But as its construction boom came to an end, demand sagged, prompting the country’s state-owned steelmakers to sell their growing surpluses on foreign markets.

Chinese exports rose from 45m tonnes in 2014 to 97m tonnes last year—an increase significantly bigger than Germany’s entire output of 43m tonnes. This has triggered demands from rival firms for protection from what they see as dumping.

American producers have been helped by their government’s willingness to impose anti-dumping duties—of as much as 236% on some forms of corrosion-resistant steel. Although the strong dollar has hurt their competitiveness, cheap gas has kept their costs low. In the euro area, although the European Commission has been slower to increase anti-dumping levies, steel mills have benefited from the euro’s depreciation over the past year. But producers in Britain have faced a perfect storm, suffering from Europe’s high energy costs as well as from a strong pound. Hence the severity of their job cuts.

Some commentators have predicted that, without government assistance, low prices will soon wipe out almost the entire steel industry in high-cost countries such as Britain. Certainly, for simpler, commoditised steels, production in Europe and America is drawing to a close, says Vladimir Sergievskiy, an industry analyst. In Britain, SSI has closed its Redcar plant, which made cheap steel slabs. Tata Steel and ArcelorMittal, two Indian-owned giants which loaded up on debt to buy much of Europe’s slab capacity when steel prices were high, look vulnerable.

Not all production can be moved to developing countries, claims Gareth Stace at UK Steel, another industry association. Sophisticated steel products, such as the components that Sheffield Forgemasters makes for the nuclear, oil and gas industries, are harder to shift. And some customers who need costly precision-cut or cast steel want a close-by supplier in case they have to return a part for adjustments. Among high-end producers such as Novolipetsk Steel of Russia and Voestalpine of Austria, demand for what they make is rising. For its part, Tata is hoping that there will be sufficient demand for the specialist products made at its Scunthorpe mill to allow it to sell the plant as a going concern.

There are even signs that the prices of sophisticated steels are bottoming out in Europe. The price of high-grade steel sheeting in Germany may have already stabilised; French and Italian producers attempted to push through price rises this month. The global picture is also likely to improve later this year, says John Kovacs, a commodities economist at Capital Economics, a consulting firm. Some steel mills in China have started to close, including one, in November, that had previously produced 5m tonnes a year. On January 24th, the Chinese authorities announced plans to cut capacity by a further 150m tonnes, although they did not say when. Low prices are also starting to stimulate demand in some places, such as in India’s booming construction industry and in America, where steel stocks are now unusually low.

Yet even with a trough for prices in sight, a return to profitability in steelmaking will take time. In 2014 EY, another consultant, said that the global industry’s capacity utilisation would need to rise from below 80% to 85% for it to become sustainably profitable. Instead, that figure has now slid to just 65%. For many plants, survival is going to be hard enough; profitability still seems a distant dream

No comments:

Post a Comment

Note: Only a member of this blog may post a comment.